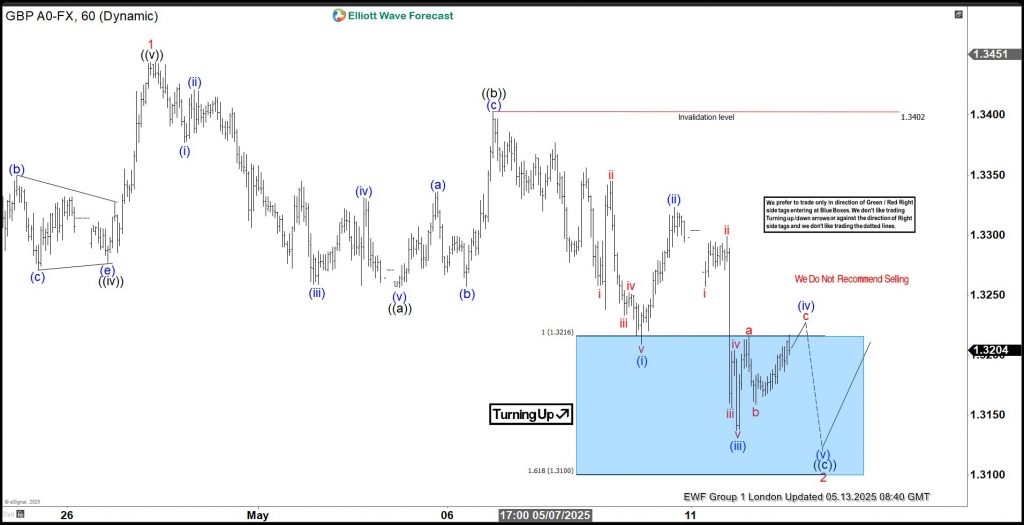

Market Snapshot March 9th 2026 – The Concept Trading

Crude and Brent are both above $100/ barrel. Red ALERT! 🚨🚨🚨

Note: Please get yourself updated with the current status of this war as it will update per seconds, any volatility from the next morning is getting the charts among the highest levels. Stay in the highest cautious.

Data:

[🟦 Global Rates | Core sovereign yields] Safe-haven demand from the weak U.S. payrolls report partly offset the inflation shock from surging oil, leaving benchmark yields elevated but off intraday extremes. U.S. Treasuries: 2Y ~3.56% | 5Y ~3.72% | 10Y ~4.13% | 30Y ~4.76%. UK 10Y Gilt ~4.63%, Germany 10Y Bund ~2.86%, France 10Y OAT ~3.51%, Japan 10Y JGB ~2.28%, Australia 10Y ACGB ~4.85%, Canada 10Y GoC ~3.41%.

[🟥 U.S. Equities | Friday close] Wall Street ended sharply lower as investors absorbed a 92,000 drop in February payrolls, a rise in the unemployment rate to 4.4%, and a surge in oil above $90/bbl, reviving stagflation concerns. Dow Jones 47,501.55 (-0.95%) | S&P 500 (US500) 6,740.02 (-1.33%) | Nasdaq Composite 22,387.68 (-1.59%).

[🟥 Europe Equities | Friday close] European equities posted their biggest weekly drop in almost a year, with the regional selloff driven by the Middle East conflict, higher oil, and weaker U.S. labor data. Euro Stoxx 50 5,795.97 (-3.19%) | DAX (GER40) 23,591.03 (-0.94%) | CAC 40 7,993.49 (-0.65%). Reuters also reported the STOXX 600 fell 1.0% on Friday and 5.5% for the week.

[🟨 Japan Equities | Friday close] Japan outperformed relative to U.S. and Europe on Friday, with bargain-hunting and a softer intraday tone in the yen helping local equities stabilize after a volatile week. Nikkei 225 55,620.84 (+0.62%).

[🟥 Macro “Red News” | Prior-day data] The key macro shock was the U.S. labor-market miss: nonfarm payrolls -92,000 in February versus expectations for gains, while the unemployment rate rose to 4.4% and wage growth stayed firm at 3.8% y/y, complicating the Fed’s reaction function. The market takeaway shifted toward a more fragile growth outlook, even as oil-driven inflation risks intensified.

[🟧 Commodities | Oil shock dominates] Cross-asset pricing remained driven by the Middle East supply shock. WTI settled near $90.90/bbl (+12.21%) and Brent near $92.69/bbl (+8.52%), both at their highest levels since 2023 as the Strait of Hormuz disruption tightened global supply expectations.

[🟨 Precious Metals | Safe-haven bid returns] Gold rebounded after payrolls, with spot gold at $5,149.14/oz and U.S. gold futures at $5,158.70/oz, although Reuters noted bullion was still headed for its first weekly loss in five weeks because of the earlier dollar strength and algorithmic selling.

[🟥 FX | Dollar weakens against havens] The payroll shock and surge in geopolitical risk pushed investors toward traditional havens, with the dollar softer against safe-haven currencies even as rate volatility stayed high. Reuters highlighted that the dollar weakened against safe-haven currencies as global volatility surged.

[🟥 High-impact headline | Stagflation risk re-enters] The combination of falling payrolls and surging oil revived a clear stagflation narrative across markets, with equities selling off even as bond markets hesitated between growth fears and inflation risk. Reuters described the shock as a “one-two punch” for risk assets.

[🟧 High-impact headline | Volatility spikes] Market stress accelerated sharply: Reuters noted that the Cboe VIX jumped to its highest level since April 2022, while U.S. banks, travel stocks, and other growth-sensitive segments underperformed.

[🟧 High-impact headline | Energy and defense leadership] In Europe, energy and defense were among the few outperforming sectors as investors repriced the conflict’s duration and the potential for sustained supply disruption. Reuters specifically cited gains in names such as Rheinmetall and Leonardo even as the broader STOXX complex slumped.

Companies.

+) Broadcom surged after reporting stronger-than-expected quarterly results, driven by robust demand for AI networking chips and custom silicon used in hyperscale data-center infrastructure.

+) Marvell Technology traded volatile following its earnings release as investors weighed strong AI-related revenue growth against cautious near-term guidance.

+) Costco declined after posting mixed earnings results, with investors focusing on slower comparable-sales growth and margin pressures despite stable consumer demand.

+) Gap Inc. fell after reporting disappointing quarterly results and issuing cautious forward guidance amid uncertain consumer spending trends.

+) Nvidia remained a central focus for investors as AI infrastructure demand continued to drive semiconductor sector sentiment, although the stock traded mixed following recent gains.

+) The Trade Desk continued to attract strong institutional inflows as investors remained bullish on digital advertising growth tied to AI-driven marketing tools.

+) Palantir Technologies gained amid ongoing demand for AI-driven defense and government analytics platforms.

+) Lockheed Martin advanced as geopolitical tensions and rising military spending expectations supported the defense sector.

+) RTX Corporation traded higher due to strong order backlogs in missile defense systems and aerospace components.

+) Boeing remained volatile as investors monitored aircraft delivery timelines and progress on regulatory approvals for its key commercial jet programs.

General

PART 1 — Market & Macro Morning Summary (09.03.2026)

Global markets begin the week under heightened geopolitical stress and a deepening energy shock as the U.S.–Iran war continues to disrupt oil supply routes across the Persian Gulf. The conflict has increasingly shifted from a localized military confrontation to a global macro‑economic event, with energy markets acting as the primary transmission channel.

Equities:

Global equity markets remain volatile after last week’s selloff driven by energy prices and geopolitical escalation. Energy producers, commodity exporters, and defense companies continue to outperform, while airlines, transportation firms, and industrial exporters remain under pressure due to rising fuel costs and logistics disruptions.

Rates & Inflation Expectations:

Bond markets reflect a conflict between safe‑haven demand and renewed inflation risk. Analysts warn that sustained oil prices above $100 per barrel could significantly complicate global disinflation trends and delay expected monetary‑policy easing across major economies.

FX & Safe Havens:

The U.S. dollar remains supported by safe‑haven flows amid geopolitical uncertainty and rising energy prices. Gold continues to attract strong hedging demand as investors position for potential escalation and prolonged market volatility.

Macro Theme:

Markets remain dominated by a geopolitical supply‑shock regime, where developments in the Persian Gulf and disruptions to maritime oil flows continue to dictate cross‑asset price action.

PART 2 — Commodities, FX & Sector Flows

Oil & Energy Markets:

Crude oil markets remain the central driver of global macro sentiment. Brent crude and WTI have surged sharply, with prices moving above $100 per barrel for the first time in nearly four years amid escalating supply disruptions.

Energy markets are reacting to severe disruptions across the Persian Gulf, particularly the near shutdown of tanker traffic through the Strait of Hormuz, a chokepoint responsible for roughly 20% of global oil and LNG flows.

Major producers across the Gulf have begun reducing output as storage fills and exports stall. Iraqi oil production has reportedly collapsed by roughly 70%, highlighting the scale of logistical disruption caused by the conflict.

Shipping & Freight Markets:

Commercial shipping through the Gulf has effectively ground to a halt as tanker operators withdraw vessels due to security risks and insurance restrictions. Hundreds of ships remain stranded or rerouting around the region.

Natural Gas:

Gas markets remain volatile after disruptions to LNG infrastructure and shipping routes across the Gulf. The shutdown of key export facilities and attacks on energy infrastructure have increased supply risks for both Europe and Asia.

Sector Rotation:

- Energy: Supported by supply disruptions and higher oil prices

- Defense: Benefiting from geopolitical tensions

- Airlines & Logistics: Under pressure due to fuel costs and rerouted flights

- Global Industrials: Impacted by shipping delays and trade disruptions

Upcoming News

Markets open the week in a post-payroll reassessment mode, as investors digest Friday’s U.S. Non-Farm Payrolls outcome and recalibrate expectations for the Fed’s policy trajectory into Q2. Overall market sense is cautiously constructive but selective, with FX and rates trading off the interpretation of wage dynamics and labour-market resilience rather than the headline payroll number alone. Liquidity is stable at the start of the week, but conviction remains moderate ahead of fresh inflation and activity data later in the week.

In the United States, today’s calendar is relatively light, positioning the session as a positioning and confirmation phase rather than a headline-driven one. Markets will closely monitor Treasury yield behavior and cross-asset flows to determine whether the payroll report reinforced the narrative of gradual labour cooling or revived concerns over persistent wage pressures. The USD is likely to trade directionally early in the session based on yield spreads before settling into ranges without fresh macro catalysts.

Across Europe, the focus shifts toward investor confidence and sentiment indicators, which help gauge whether early-Q1 growth expectations are stabilizing following recent PMI readings. EUR price action remains primarily driven by U.S. rate differentials and global risk sentiment. In the Asia–Pacific region, Japan’s current account data and China’s inflation readings offer regional context on external balances and price dynamics, influencing JPY and CNH through trade and policy expectations. Corporate catalysts remain limited, leaving macro interpretation and positioning adjustments as the dominant drivers.

| Time (GMT+7) | Category | Country / Region | Event | Market Relevance |

| 06:50 | 🔴 Red News | Japan | Current Account | External balance and flow dynamics; JPY sensitivity |

| 09:30 | 🔴 Red News | China | CPI (y/y) | Consumer inflation; CNH & regional risk sentiment |

| 09:30 | 🔴 Red News | China | PPI (y/y) | Producer price dynamics; commodities outlook |

| 17:00 | 🔴 Red News | Eurozone | Sentix Investor Confidence | Forward-looking sentiment; EUR sensitivity |

| All day | 🔶 Stress / Headlines | Global | Post-NFP positioning / policy headlines | May amplify FX and rates moves |

Snapshot (09.3.2026)

🟢 Dollar Surges | DXY 99.54 (+0.68%)

The U.S. Dollar Index climbed sharply to 99.54, approaching the 100 level as risk sentiment deteriorated. The move reflects strong safe-haven demand for the dollar amid rising geopolitical and commodity volatility.

🛢 Oil | Sharp Rally

- WTI Crude 107.40 (+17.69%)

- Brent Crude 108.06 (+16.02%)

Oil prices surged dramatically, with WTI jumping above $107 and Brent above $108. The rally reflects supply shock concerns and heightened geopolitical risk, triggering one of the strongest single-session moves in crude markets in recent months.

🔄 G7 FX | USD Dominance

- EUR/USD 1.1526 (-0.77%)

- GBP/USD 1.3309 (-0.71%)

- USD/JPY 158.38 (+0.40%)

- USD/CHF 0.7811 (+0.65%)

The stronger dollar pressured major currencies broadly, with EUR and GBP weakening significantly. USD/JPY advanced toward the 158 level as yield differentials continued to favor the greenback.

🪙 Crypto | Broad Selloff

- BTC 66,182 (-1.62%)

- ETH 1,942 (-1.38%)

- SOL 82.12 (-1.31%)

Crypto markets declined as investors rotated into defensive assets. Bitcoin slipped toward the 66k area while altcoins posted similar downside pressure.

🥇 Metals | Precious Metals Under Pressure

- Gold 5,073 (-1.91%)

- Silver 81.96 (-2.98%)

Precious metals fell sharply despite geopolitical stress, reflecting the strong USD rally and profit-taking after the previous rally phase.

📊 Equities | Risk-Off Shock

- S&P 500 6,623.35 (-1.64%)

- Dow Jones 46,650.15 (-1.72%)

- Euro Stoxx 50 5,619.95 (-1.77%)

- VIX 28.75 (+7.54%)

Global equities dropped sharply as oil’s surge triggered inflation concerns and risk aversion. The VIX spiked above 28, signaling a significant jump in market volatility.

This report is provided to The Concept Trading from Van Hung Nguyen