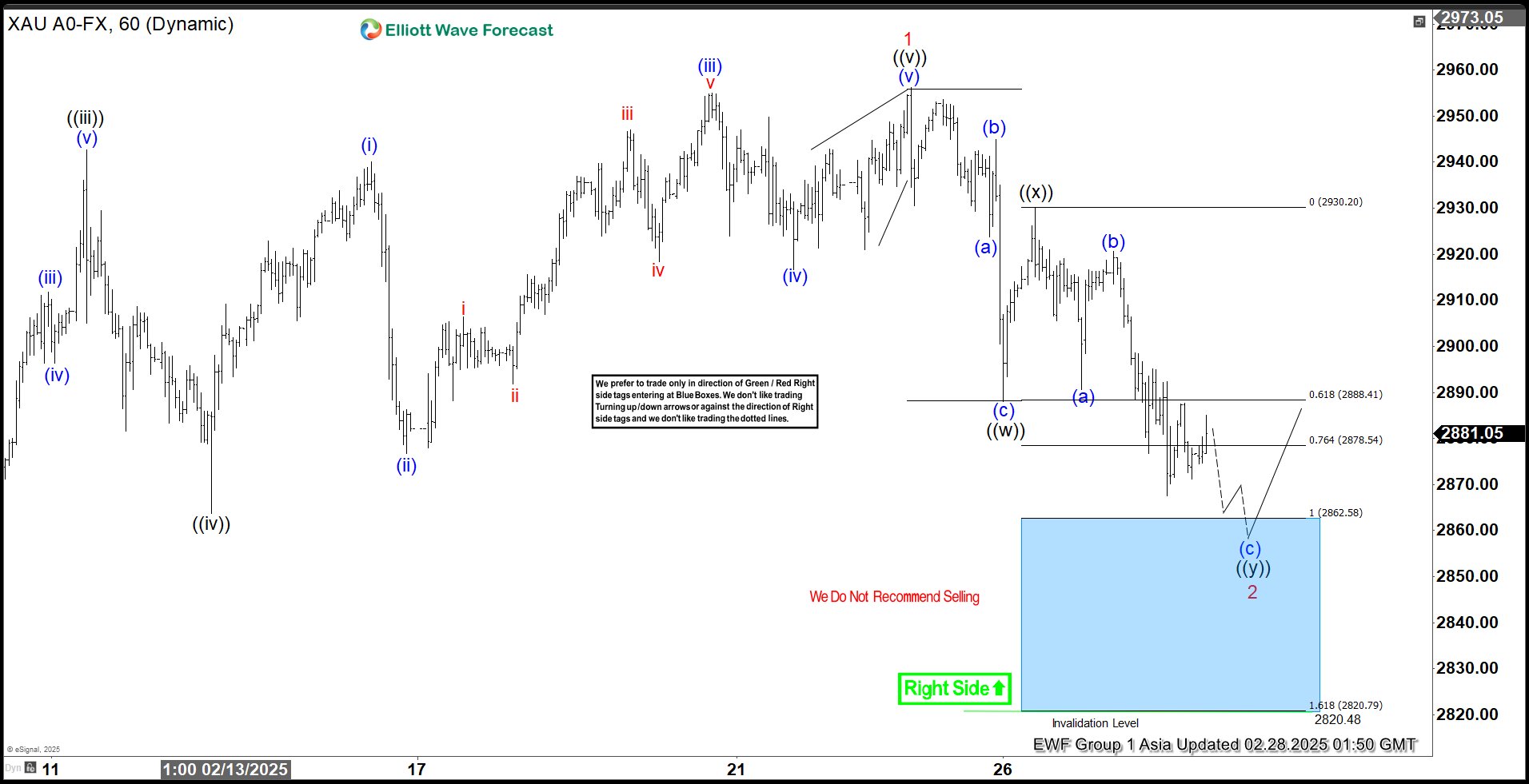

Oil prices have once again approached 100 dollars per barrel

By the end of the day, the Dow Jones (US30) rose by 0.52%. The S&P 500 (US500) gained 0.62%. The tech‑heavy NASDAQ (US100) closed up 0.72%. The main driver of optimism was news that Israel is willing to consider negotiations with Lebanon. This eased investor fears of the entire region being dragged into a full‑scale war and allowed markets to enter a phase of confident consolidation near recent highs. Despite the positive sentiment on Wall Street, the overall atmosphere remains tense. Oil prices, once again surging toward 100 dollars per barrel, serve as a constant reminder that the Strait of Hormuz is still at risk of a complete blockade.

On Thursday, European stock Indices closed in the red, giving back part of Wednesday’s record rally. By the end of the day, Germany’s DAX (DE40) fell by 1.14%, France’s CAC 40 (FR40) declined by 0.22%, Spain’s IBEX 35 (ES35) slipped by 0.15%, and the UK’s FTSE 100 (UK100) closed down 0.05%. The shift in sentiment came after reports that the two‑week ceasefire between the US and Iran had already begun to crack. Tehran accused Washington of violating the terms of the truce, reigniting fears of renewed attacks on tankers in the Persian Gulf and a prolonged energy shortage.

Silver prices posted a strong rally, reaching 74.5 dollars per ounce. This rise reflected investor reaction to the critical instability of the 14‑day ceasefire between the US and Iran. Amid the renewed disruption in the Strait of Hormuz and a sharp spike in oil prices to 99 dollars, silver regained its appeal as a safe‑haven asset. An additional driver was the weakening US dollar, which made precious metals more attractive for holders of other currencies.

The oil market was hit by a new wave of volatility: WTI prices jumped nearly 5%, reaching 99 dollars per barrel. This sharp rise almost erased the previous day’s optimism and followed reports that the two‑week ceasefire announced by Donald Trump was on the verge of collapse. Traders reacted instantly to news of increased military activity near the Strait of Hormuz and delays in tanker traffic, which brought the risk premium back into the market. Prices also received fundamental support from OPEC+, which reaffirmed its commitment to production cuts, and from fresh US data showing an unexpected decline in commercial crude inventories.

On Friday, US natural‑gas prices held at 2.67 dollars per MMBtu, the lowest level in a year and a half. While the oil market is shaken by uncertainty in the Middle East, the US gas sector shows remarkable resilience. The main pressure on prices comes from domestic fundamentals: oversupply and unseasonably warm weather, which meteorologists expect to persist across most of the US at least until April 24. The latest EIA report confirmed bearish concerns: gas inventories rose by 50 billion cubic feet for the week, exceeding market expectations.

In Asia, Japan’s Nikkei 225 (JP225) fell by 0.73%, China’s FTSE China A50 (CHA50) declined by 0.61%, Hong Kong’s Hang Seng (HK50) dropped by 0.54%, while Australia’s ASX 200 (AU200) gained 0.24%.

The Australian dollar confidently held above 0.707 USD, reaching a three‑week high. The currency is on track for its strongest weekly gain since mid‑January, supported by a temporary improvement in global risk appetite following the announcement of the two‑week ceasefire. Since the aussie is traditionally viewed as a barometer of global market sentiment, the decline in demand for the safe‑haven US dollar and hopes for de‑escalation in the Middle East provided strong support. Despite the optimism, the backdrop remains extremely tense due to the situation in the Strait of Hormuz. If direct negotiations with the Iranian delegation fail and the blockade persists, global supply chains could be hit hard – instantly cooling demand for risk assets such as the Australian dollar.

S&P 500 (US500) 6,824.66 +41.85 (+0.62%)

Dow Jones (US30) 48,185.80 +275.88 (+0.58%)

DAX (DE40) 23,806.99 −273.64 (−1.14%)

FTSE 100 (UK100) 10,603.48 −5.40 (−0.05%)

USD Index 98.83 −0.31 (−0.31%)

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.