Is It A Good Idea To Buy An Option Straddle Across Earnings?

Since stocks have the potential to make a big move on earnings announcements, one might think that it is a good idea to buy an option straddle and hold it through earnings to profit from the large move.

Is that really a good idea?

Unless one has extra money to lose, one really needs to analyze this idea carefully and backtest and/or paper-trade it before throwing hard-earned money into an earnings straddle (pun intended).

An option straddle consists of an at-the-money put option plus an at-the-money call option at the same strike and expiration.

Since we are buying a straddle, we are buying both the call and put options before the earnings announcement.

When we buy an option, we say that we are “long” the option (as opposed to “short” the option).

So, this option combination is known as a long straddle.

Contents

Let’s test out one example of buying a long straddle on Verizon (VZ) on January 29, 2026 – the day before the earnings announcement scheduled for the next morning.

Date: Jan 29, 2026

Price: VZ at $39.93

Buy to open ten contracts Jan 30 VZ $40 call @ $0.73

Buy to open ten contracts Jan 30 VZ $40 put @ $0.80

Net Debit: -$1525

Since VZ is at $39.93, the at-the-money strike is the one closest to the current price – the $40 strike price.

We have chosen the closest expiration date that is after the earnings event.

A straddle consists of one call and one put option.

We are buying 10 straddles – or 10 contracts.

The call option costs $0.73 per share, or $73 per contract.

The put option costs $80 per contract.

So 10 of these cost a total of $ 1,525, which is the maximum risk in the trade.

10 x ($80 + $73) = $1530

For the backtest, we use the mid-price provided by OptionNet Explorer, which may be subject to some rounding.

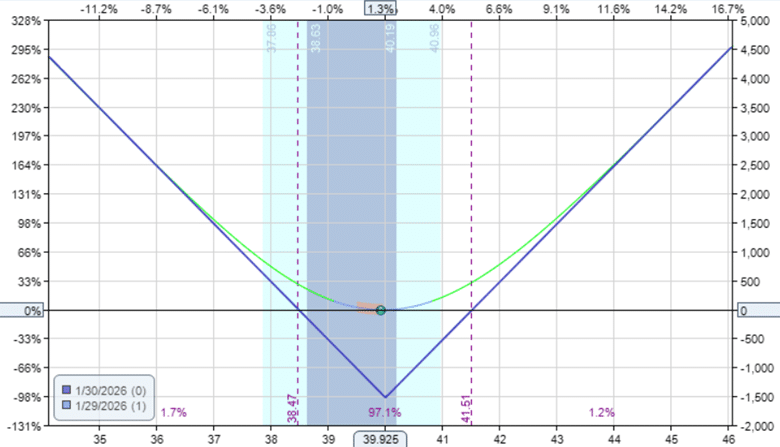

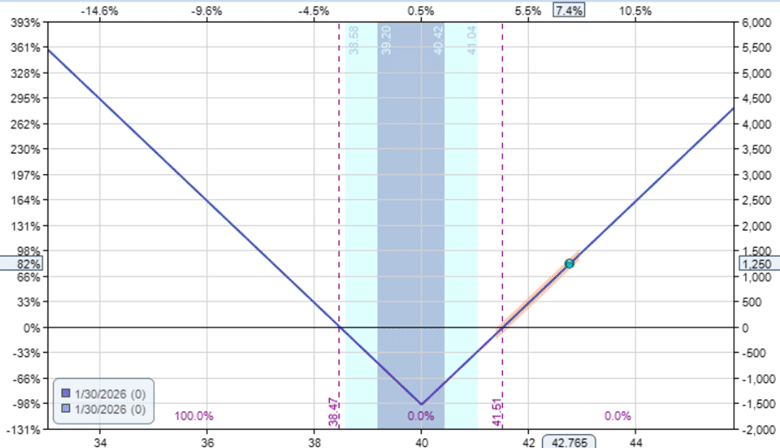

This is the payoff graph for the long straddle at the start of the trade…

Advancing the clock one day in OptionNet Explorer so that we are now past the earnings event and the option is expiring, we have the following…

Verizon went from $40 to $42.76.

Because of the big move, the straddle profits $ 1,250, or an 82% return on the capital invested.

This is due primarily to VZ making a greater-than-expected move.

An expected move would be about one standard deviation, as shown by the gray shading…

Here, Verizon’s move exceeded two standard deviations.

One example does not make a good backtest.

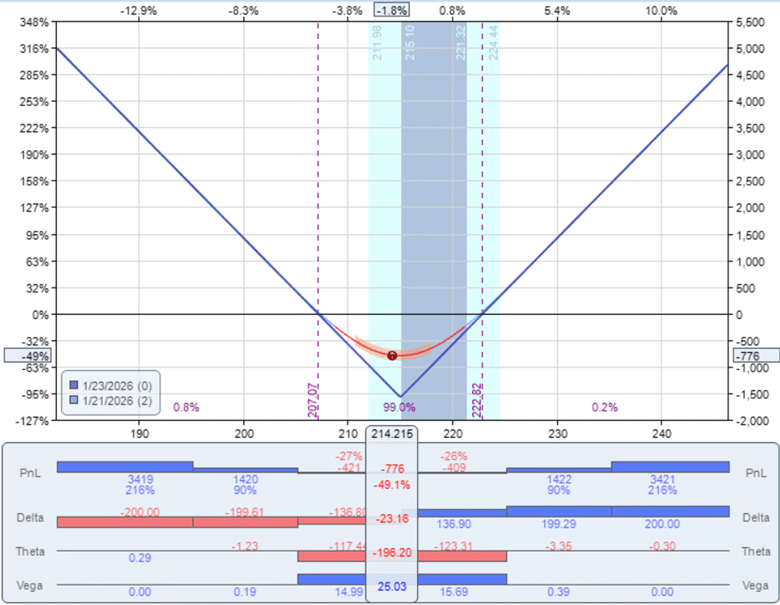

Let’s look at another example—this time on Johnson and Johnson (JNJ).

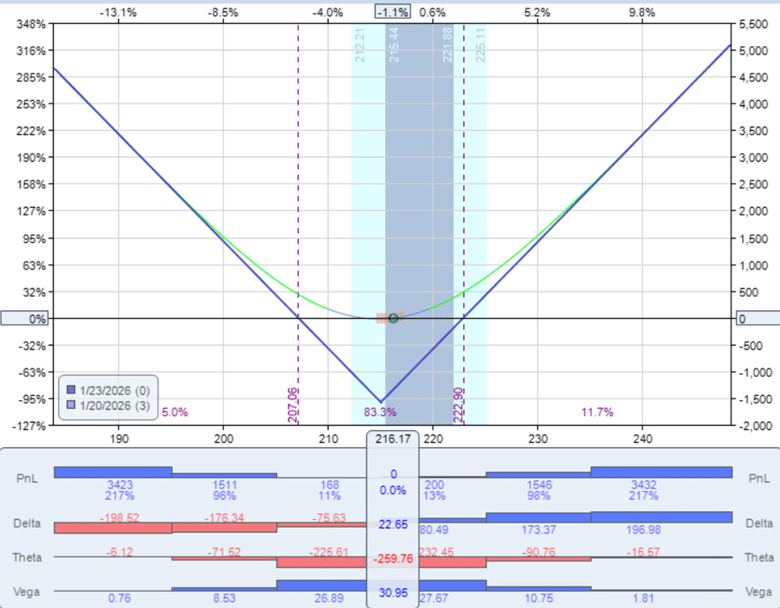

Date: Jan 20, 2026

Price: JNJ @ $216.17

Buy to open two contracts Jan 23 JNJ $215 call @ $4.40

Buy to open two contracts Jan 23 JNJ $215 call @ $3.50

Net Debit: $1580

We see that the trade starts with a near-zero delta, meaning it is non-directional.

We make money whether the stock moves up or down in price.

As is true of long options, they have negative theta.

It means that the trade loses value as it gets closer to expiration, or as time passes.

This is one factor going against the profitability of the trade.

Another Greek that will become important to watch is Vega, which measures how an option’s value changes with changes in implied volatility.

As with long options, they have positive vega, meaning the option rises in value as implied volatility (IV) increases.

The options lose value as IV drops.

The next day after the earnings event, the straddle lost $776, or nearly half of the capital invested…

This is because JNJ made only a modest move from $216.17 to $214.21, representing a 0.9% decline.

Everyone knows when the earnings event occurs.

They even know the expected price move of the event.

This information is priced into the options’ cost.

The greater the expected move in the stock, the higher the options will cost.

This is also why the cost of the options in the straddle is relatively high when buying them right before earnings.

We say that the market is efficient in pricing information.

All knowledge of the event is priced into the option.

Therefore, we can say that the options are fairly priced based on all available known information.

If something is fairly priced, we cannot expect to profit by buying and then selling it unless there is a one-off event that was not expected (as in the case of Verizon).

Looking at the vega before and after the earnings event.

It was 30.95 before and dropped to 25.03 after.

This drop is known as a volatility crush, which occurs once the uncertainty surrounding earnings is gone.

Recall that a drop in IV hurts the value of the long options.

This played a big role in the trade’s loss.

A good backtest needs a large enough sample size.

Anything less than twenty trades is not enough to tell us anything with any kind of confidence.

While no fixed number guarantees statistical significance, the more the better.

Fifty would give us better confidence.

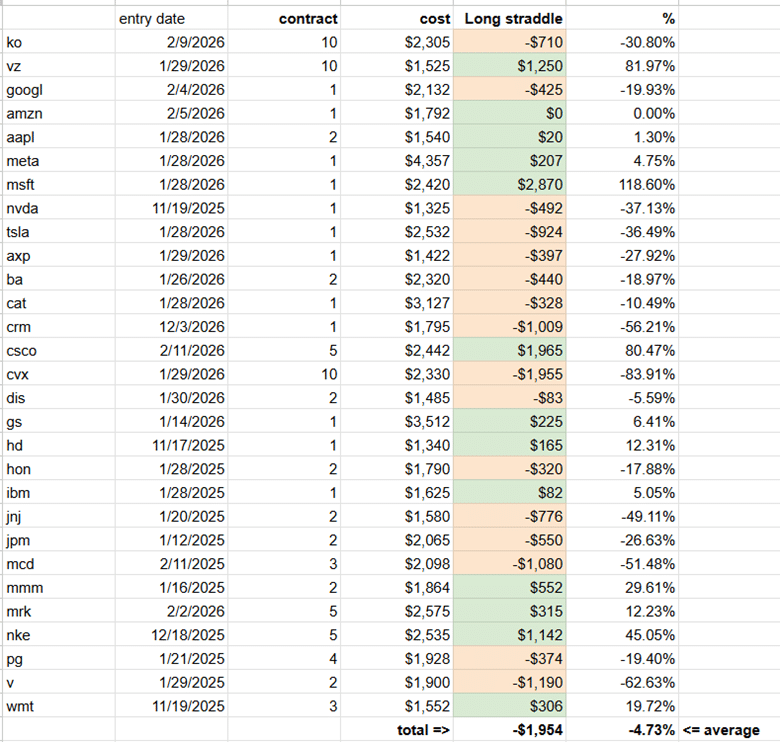

For our purposes, we’re going to review 29 backtested earnings-straddle trades across several popular stocks.

This aligns with the roughly 20 to 30 earnings trades a typical retail trader might realistically place during a single earnings quarter.

Of the 29, there were 16 losing trades and 13 winning trades.

The total P&L (profit and loss) accumulated from the 29 trades was -$1,954, nearly a $2,000 loss.

Each trade carried roughly $2,000 in risk, and we sized the number of contracts to keep trade risk as consistent as possible.

Even so, not every setup will have identical risk, which naturally leads to some variation in individual trade P&L.

A more comparable metric is the percentage return on risk shown in the last column, since it isn’t dependent on trade size.

Averaging the percent return across all the trades yields -4.7%.

A negative average return indicates negative expectancy, meaning the strategy is expected to lose money over the long run.

The long earnings straddle has several things going against it:

- Option prices have already priced in the move

- Volatility crush hurts the value of the straddle

- Time decay of negative theta causes the straddle to lose value

The combination of these factors generally makes buying long straddles through earnings events a poor strategy, as demonstrated by the backtest above.

If you don’t have analytical tools with historical option data to test a strategy, you can always paper-trade it first to see how it performs before committing real capital.

We hope you enjoyed this article on buying options straddles across earnings

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link