Four Options Portfolio Management Principles

When managing an options portfolio, there are four principles to consider:

- Directional Exposure

- Position Sizing

- Theta Income Generation

- Hedging

Contents

At the portfolio level, I prefer using Beta-weighted Delta Dollars since it gives a more realistic picture of your directional exposure across different ticker symbols.

Beta-weight delta dollars answers the question…

“How many dollars of SPY exposure is my position equivalent to, once I adjust for my underlying’s beta relative to the market?”

You cannot simply add up the options’ Greek deltas, because those deltas are relative to the underlying’s size.

An option Greek of 1 delta on an SPY (the S&P 500 ETF) trade is different from 1 delta on a Cisco (CSCO) trade because the asset sizes are completely different.

The Greek delta tells you how much the option price changes for a $1 change in the stock price.

You can think of delta as a “share equivalent”.

One delta on the SPY position is equivalent to one SPY share in directional exposure.

One delta on a CSCO position is like owning one share of CSCO.

Below, I have modeled a one-contract bull put credit spread in SPY…

OptionNet Explorer shows that this position has a delta of 5.

Less commonly, some platforms or modelling software may show this same delta as 0.05, which is 100 times lower.

It is because they are giving it on a per-share basis, whereas OptionNet Explorer is giving it as a per-contract basis.

One contract is equivalent to 100 shares.

Since we have one contract of a bull put spread, a delta of 5 is correct here.

In terms of directional exposure, it is like me owning 5 shares of SPY.

Since SPY is trading for $680 per share, I have $3400 of directional exposure.

This is calculated by 5 times $680.

The number $3400 is what we call the Delta Dollar for the position.

CSCO is trading at $80/share.

So a bull put spread on CSCO with 5 delta will give you only $400 of directional exposure, because 5 times $80.

Delta Dollar = delta x stock price

It gives a better picture of our directional exposure, but not exactly.

The SPY put spread has a Delta Dollars of 5 x $680 = $3400.

It is like owning $3400 worth of stock in SPY.

The CSCO put spread has a Delta Dollars of 5 x $80 = $400.

It is smaller.

It is like owning $400 worth of CSCO stock.

But not all stocks are the same.

A $1 ownership in SPY is not the same as a $1 ownership in CSCO, because CSCO is less volatile than SPY.

It has less price movement than SPY.

CSCO moves 13% less than SPY does.

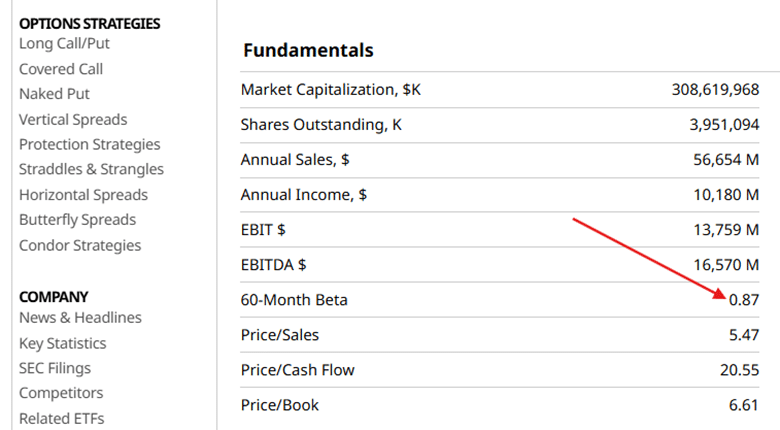

This is because CSCO has a Beta of 0.87…

SPY, by definition, has a Beta of 1.0 and is a proxy for the overall market.

When we standardize the Delta Dollars to this market proxy, we get the Beta-Weighted Delta Dollars.

Beta-Weighted Delta Dollars = Beta x Delta x price per share

Beta-Weighted Delta Dollars of CSCO put spread = 0.87 x 5 x $80 = $348

This number represents the number of dollars of SPY exposure the CSCO put spread represents.

Beta-Weighted Delta Dollars of the SPY put spread = 1.0 x 5 x $680 = $3400.

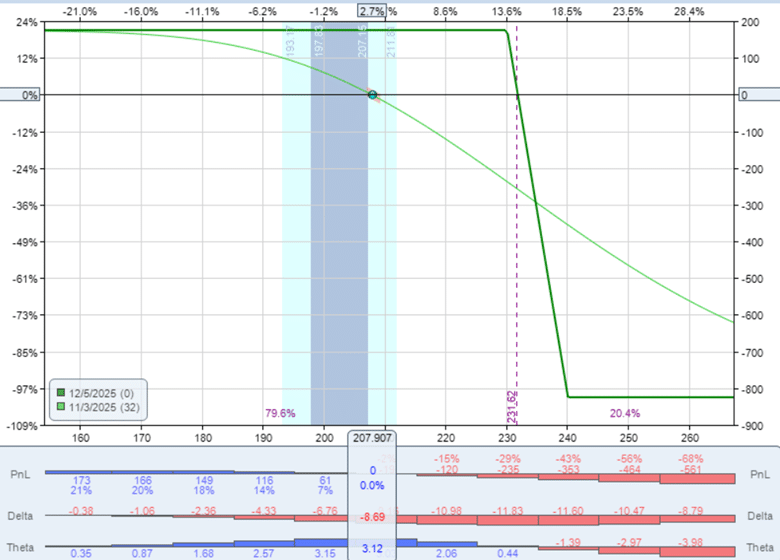

As another example, NVDA has a Beta of 2.3.

If SPY moves up on an up day, NVDA moves twice as much up.

If SPY moves down, NVDA moves twice as much down, on average, generally speaking.

It doesn’t happen like that every day, of course.

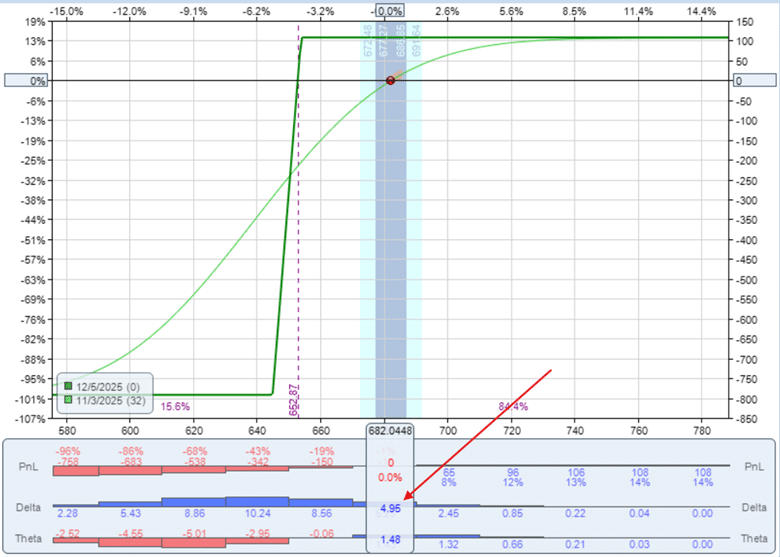

This bear call spread on NVDA has a delta of -8.7 (which means that it profits when the price of NVDA goes down).

This negative delta causes the Beta Weighted Delta Dollars of the position to be negative as well.

Beta Weighted Delta Dollars = 2.3 x -8.7 x $207.9 = -4,160

If you have other positions in the portfolio, you would sum up all the Beta-Weighted Delta Dollars to come up with the portfolio Beta-Weighted Delta Dollars.

If you get a positive number, you have a bullish portfolio.

If you get a negative number, you have a bearish portfolio.

But you don’t want the portfolio to be too bullish or too bearish.

You generally don’t want the magnitude of this number to be more than half or one times your account size.

So if you have a $50k account, you want your portfolio Beta-Weighted Delta Dollars to be $25k or less (if you are conservative or a non-directional trader).

If you are a directional trader, you can set this limit to $50k (or whatever your account size is).

If your portfolio Beta-Weighted Delta Dollars is greater than your account size, you’re starting to take on outsized directional risk.

Unlike a pure stock investor, an options investor can get into positions with directional exposure that exceeds their account size.

This is why people say that options are leveraged.

So now that we have set some risk guidelines at the portfolio level, we also need to establish some risk parameters at the trade level.

Keeping each trade to 3-5% of account risk is a solid guideline, and it’s what I do as well.

If you are still learning and don’t want to lose too much money, you can set it to 1% to 2% of your account size.

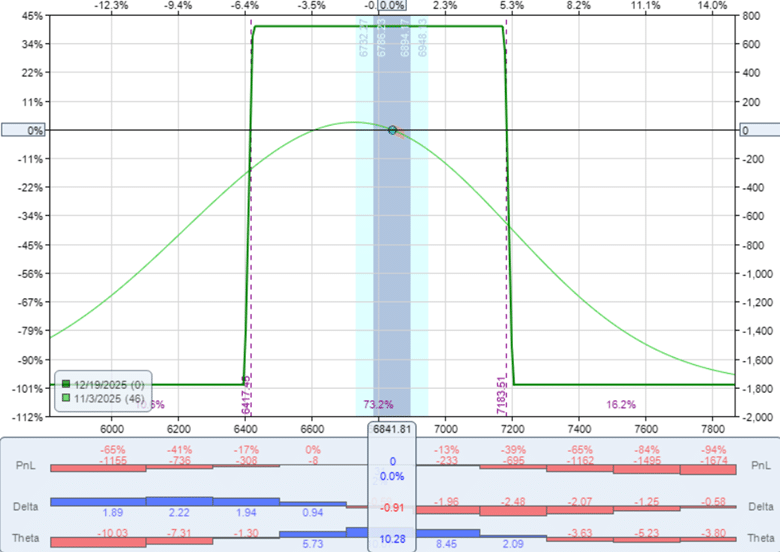

Reading the payoff graph of this one-contract iron condor on SPX (S&P 500 index).

We see that it has a max risk of $1800.

If you have a $50k account, this one trade represents 3.6% of your account…

$1800 / $50000 = 3.6%

This is within the risk parameters.

However, you could not trade two contracts of this iron condor because if the trade reached max loss, you would lose $ 3,600, which would be 7.2% of your account.

This would exceed the risk guidelines, which state that no single trade should lose more than 3% to 5% of your account.

I am a net seller of options.

I like to sell options, collect the premium, and let time decay do its work.

Most of my trades are theta positive.

That means the position makes money over time (assuming all other factors remain the same).

Theta is another option Greek that determines how much an option’s position decays each day due to the passage of time.

Unlike delta, theta does not depend on asset size.

One unit of theta in CSCO is the same as one unit of theta in NVDA.

The Greeks are additive across contracts.

If a one-contract bull put spread in CSCO has a delta of 5 and a theta of 0.43, then a 10-contract position would have a delta of 50 and a theta of 4.3.

Ideally, I want my theta per day across all positions to be between 0.06% and 0.10% of account size.

For a $50k account, that is daily Theta around $30-$50.

You can aim higher if you want to be more aggressive, but it becomes riskier as well.

The more theta, the more gamma.

Gamma is the second-order option Greek that measures how quickly delta changes as the underlying stock price moves.

If delta changes too much or too fast, your Delta Dollars can exceed your risk parameters while you are not watching.

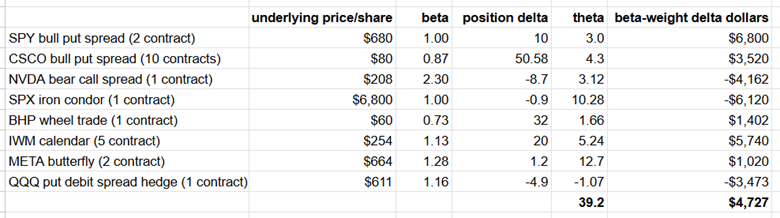

Here is a hypothetical portfolio of a $50k account.

Each position’s size and the overall portfolio’s beta-weighted delta dollars are within risk parameters.

If we added up all the theta, we get 39.2, which is 0.08% of the account value.

39.2 / 50,000 = 0.08%

This is within our target range.

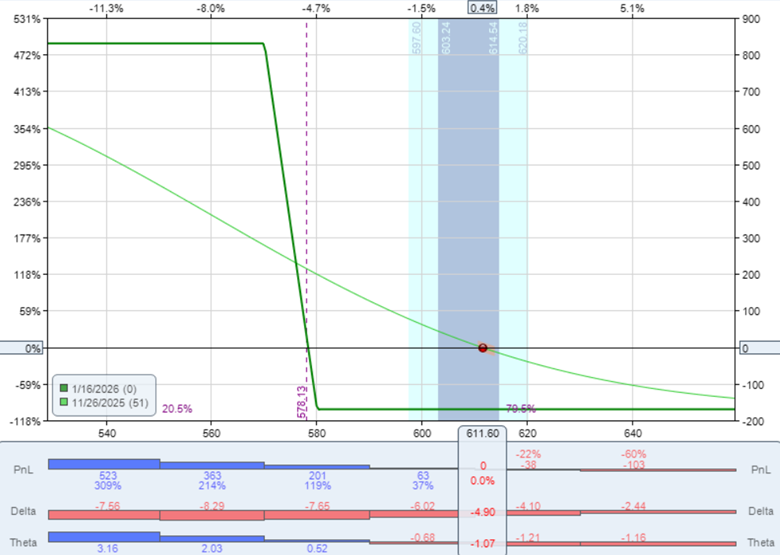

The only position with a negative theta is the QQQ bear put spread, which looks like this for one contract.

This is intentional.

A small put debit position can help reduce overall Delta Dollars when your portfolio is tilted too bullish, or you think the market will pull back.

The long put option is around the 25-delta on the option chain, with an expiration about 60 days out.

The hedge should not risk more than 1% – 2% of account size and should exit, and optionally re-hedge, once the hedge’s value decreases by half.

In this example, the one-contract hedge is risking $200, which is only 0.4% of the account value.

It had reduced the portfolio’s beta-weighted delta dollars by $3,473.

The portfolio’s overall beta-weighted delta dollars are now $4727.

This means the portfolio has a directional exposure equivalent to owning $4727 worth of SPY shares.

Since one SPY share is $680, it is like having 7 shares of SPY.

If you came from the world of stock investing, then you have an intuitive idea of what 7 shares of SPY exposure feels like.

It may feel small to some traders and big to others.

As you enter into the world of options and delta, you now know how to translate the options positions to SPY share equivalents.

By understanding directional exposure and position size, options give traders a flexible toolkit to harness theta income and to manage risk by balancing delta dollars and hedging.

We hope you enjoyed this article on options portfolio management.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link