The Most Misunderstood Option Strategy Is The In-The-Money Covered Call

There is a distinction between an out-of-the-money covered call and an in-the-money covered call.

The traditional covered call is an out-of-the-money covered call, in which an investor buys 100 shares of a stock and sells a call option with a strike price above the purchase price.

This makes sense.

This is the covered call that is taught and is the covered call that you should learn first.

When people talk about covered calls, they mean this one.

On occasion, you might see someone selling an in-the-money-covered call, where the strike price of the call option is below the purchase price of the stock.

This is known as an in-the-money covered call.

At first glance, this does not make sense because there is a good chance the investor is obligated to sell the stock at a price lower than the purchase price.

Today, we are going to see if we can make sense of this most misunderstood options strategy.

But first, let’s review the traditional covered call so you get a solid understanding of the terminology.

Contents

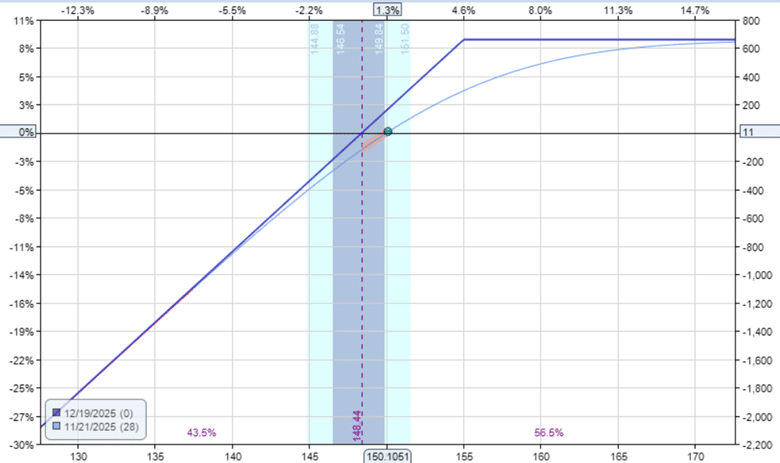

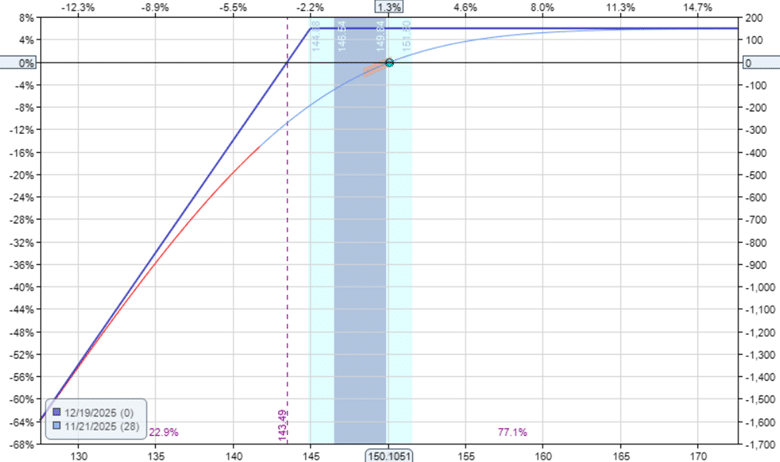

In the traditional covered call, the investor buys 100 shares of Procter & Gamble (PG) stock at $150 per share.

And then sell one contract of a call option with a strike price of $155 expiring in 28 days.

Date: Nov 21, 2025

Price: PG @ $150

Buy 100 shares @ $150 per share

Sell one contract Dec 19 PG $155 call @ $1.60

The investor paid $15,000 to acquire the shares and received a $160 credit from selling the contract, a net debit of $14,840.

But we’ll just make it easy and say this is about a $15,000 investment.

The payoff graph will look like this with the stock price on the bottom horizontal axis and the P&L (profit and loss) on the vertical axis:

A call option is out-of-the-money if its strike price is higher than the stock price.

The call option with a strike price of $155 is considered an out-of-the-money option because it has no “intrinsic value” right now.

The owner of this call option has the right to buy 100 shares of PG at $155 per share.

But there is no point in doing that right now, since the market price is $150 per share.

While this option has no intrinsic value, it does have “extrinsic value”.

Extrinsic value represents the value assigned to the possibility that the option might later have intrinsic value at expiration.

Extrinsic value is what some people call “time value”.

As shown in the payoff graph, the covered call is a bullish strategy.

The out-of-the-money covered call is more bullish than the in-the-money covered call.

In both cases, the investor wants the stock to go up.

In this example, the maximum profit is $660 if the stock finishes above $155 at expiration.

At that point, the short call is assigned, requiring the investor to sell the 100 shares at the $155 strike.

Since the shares were purchased at $150 and sold at $155, the investor earns $500 from the $5 increase in stock price, plus the $160 option premium received.

This results in a total potential profit of $660, or a 4.4% return on invested capital.

The covered call – whether it is an out-of-the-money or in-the-money covered call – is also an unlimited-loss trade with the potential to lose the entire investment if the stock goes to zero.

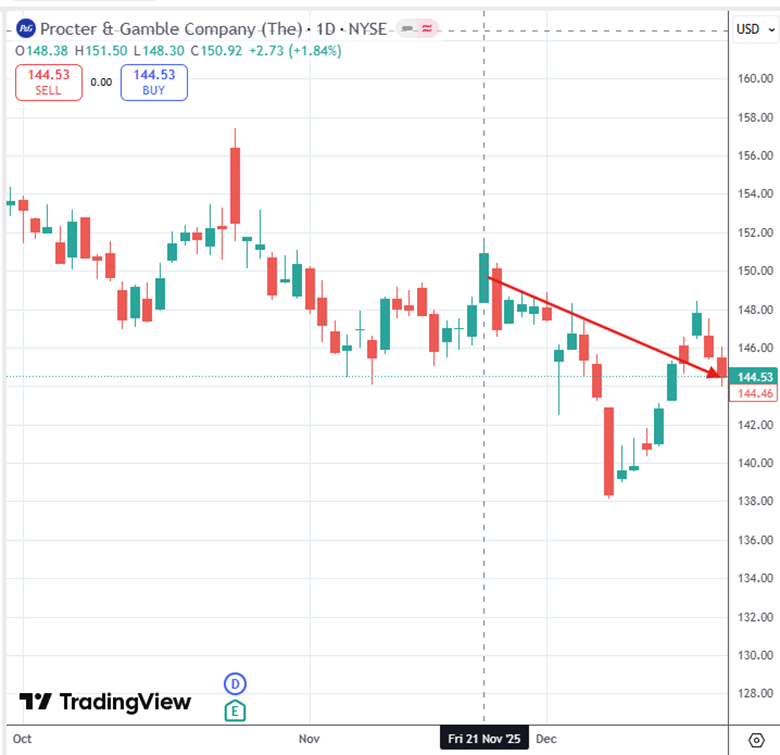

Unfortunately, the stock did go down.

But fortunately, not to zero.

On expiration day on December 19th, the PG stock closed at $144.46.

The investor lost $5.54 per share of the PG stock:

$150 – $144.46 = $5.54

With 100 shares, the loss is $554.

Taking into account the $160 of the initial credit received for the call option, the net loss is $394.

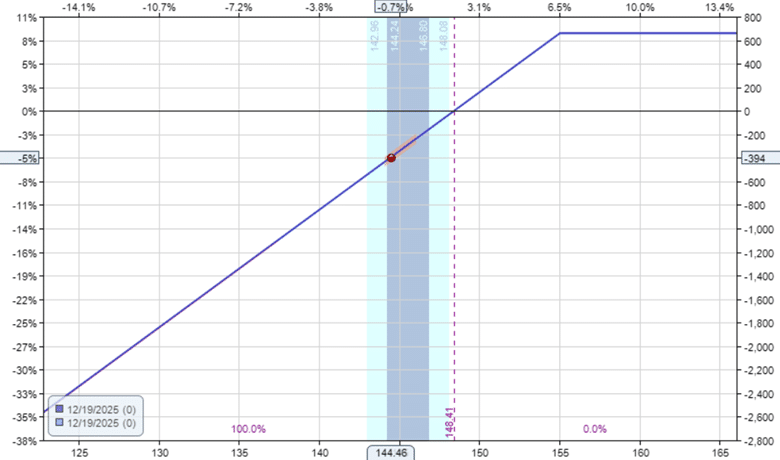

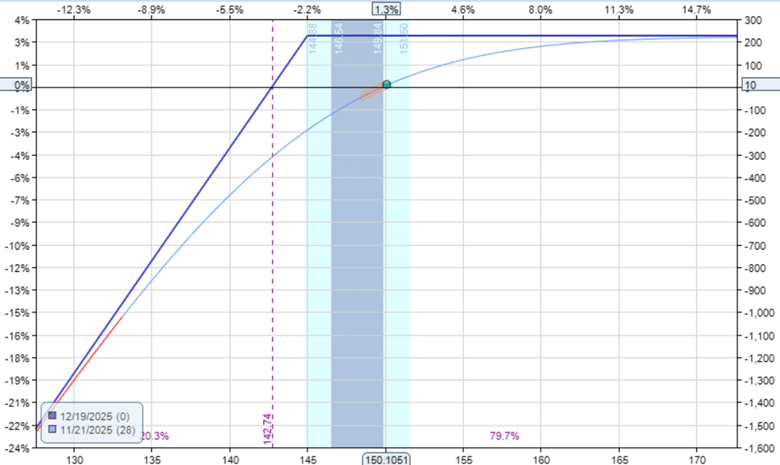

Now consider a different investor who also buys 100 shares of PG at $150 per share.

But this investor sells a call option with a strike price of $145.

The options expire on December 19th, as in the previous example.

Date: Nov 21, 2025

Price: PG @ $150

Buy 100 shares @ $150 per share

Sell one contract Dec 19 PG $145 call @ $7.27

By selling this call option, the investor is obligated to sell his 100 shares at $145 per share if PG is above $145 at expiration.

PG is already above $145, so there is a good chance that this could happen.

On the surface, it doesn’t make sense that the investor bought stock at $150 per share and then sold a call option that could result in his shares being sold out at $145, taking a $ 5-per-share loss on the stock.

If someone were to ask him whether he was afraid that his stock would be called away at a loss, he would reply that he would love it if that happened.

This is why the in-the-money covered call is so misunderstood.

This call option is in-the-money because it already has an intrinsic value of $5 per share, or $500 per contract.

This is because if the owner of the call option were to exercise it right now, he would be able to buy 100 shares of PG at $145 per share when PG is trading at $150 – an automatic $5 per share gain.

In fact, this call option is worth $727 right now – $500 of intrinsic value plus $227 of extrinsic value.

This is why when the investor sold the call option, the investor received a $727 initial credit.

The payoff graph of this in-the-money covered call looks similar except that its potential profit is capped at $227…

This max potential profit is achieved if PG is above $145 at expiration, in which case the investor’s stock will be called away (sold at $145 per share).

Of the $727 credit he initially received, he would lose $500 to depreciation of the stock, and he would pocket the remaining $227 as his profit.

So he is correct that he would love it if the stock price is above $145 so that his stock is called away.

That would be the best-case scenario, with a maximum potential profit of $227.

But let’s see what actually happens.

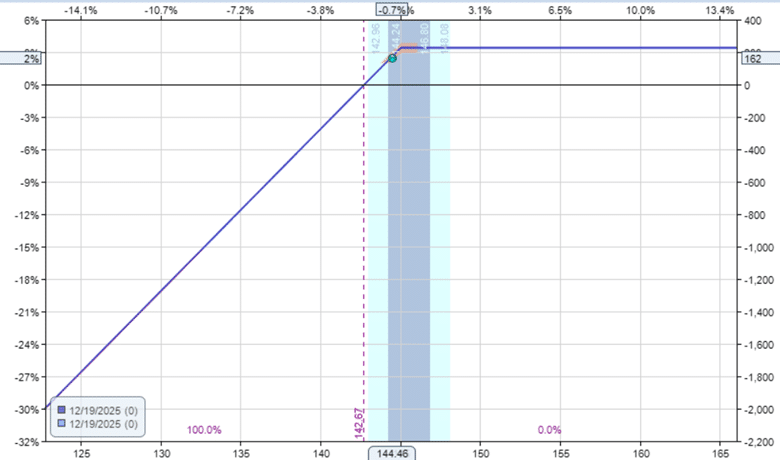

On expiration day, the PG stock closed at $144.46 – just short of $145.

So the stock was not called away because the call option strike price of $145 is higher than the stock price.

The owner of that call option would not want to exercise his right to buy at $145 when the market price is at $144.46.

The call option expired worthless.

The investor in the covered call took a loss of -$554 due to the stock’s depreciation.

($150 – $144.46) x 100 = $554

With an initial credit of $727, taking a $554 loss on expiration day means a net profit of $173.

In this example, the in-the-money covered call made money while the traditional out-of-the-money covered call lost money.

This is because the in-the-money covered call offers much better downside protection in the event the stock goes down, which it did in this case.

The breakeven point for the traditional covered call example was $148.44 (see the payoff graph above).

The breakeven point on the in-the-money covered call was at $142.74.

This means that the trade would be profitable as long as PG is above $142.74 at expiration.

The traditional covered call makes money from stock price appreciation, plus from the sale of the extrinsic value of the call option.

The in-the-money covered call is more concerned with making money from the sale of the call option’s extrinsic value.

At expiration, it would make the same amount of money regardless of whether the stock went up or down (as long as it didn’t drop too much).

In our example, the investor of the in-the-money covered call collected the $272 in extrinsic value even as the stock price dropped.

This $272 in potential profit on a $15,000 investment is about a 1.8% return in one month.

Consider a third investor who doesn’t bother with stock or call options.

Instead, she sells an out-of-the-money short put option on PG with the same expiration.

Date: Nov 21, 2025

Price: PG @ $150

Sell one contract Dec 19 PG $145 put @ $1.50

Credit: $150

A put option is considered out-of-the-money if its strike price is below the price of the stock.

After collecting her $150 credit, she says she doesn’t care whether the stock goes up or down, as long as it doesn’t drop too far.

At expiration, she will keep the “extrinsic value” of the put option she sold.

Sounds just like what the in-the-money covered call investor would say.

Looking at the payoff graph of the short put…

The payoff graph of the out-of-the-money short put looks just like the in-the-money covered call.

In both cases, the bend in the expiration graph is below the current stock price.

(The exact profit numbers may differ due to the difference in the extrinsic value of the puts versus calls from put-call skew.)

The out-of-the-money short put does not look like the traditional covered call, where the bend is above the stock price.

In fact, the traditional covered call is like selling a short put above the stock’s price, which is like selling an in-the-money short put.

Selling a put option above the stock price feels uncomfortable to many investors.

But selling a covered call does not.

Why?

They are the same.

Investors sell out-of-the-money puts all the time.

But they rarely sell in-the-money covered calls.

Why?

They are the same.

Perhaps it is because the in-the-money covered call is the most misunderstood and most under-appreciated of all options strategies (in my opinion).

We hope you enjoyed this article on selling in-the-money call options.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link

![Ultimate Guide To Footprint Charts [Best Volume Footprint Strategy]](https://dcgreferral.com/wp-content/uploads/2025/07/1753204233_Ultimate-Guide-To-Footprint-Charts-Best-Volume-Footprint-Strategy-768x512.png)