Stagflationary Concerns – Currency Thoughts

Stagflationary Concerns

February 27, 2025

The investment community remains concerned that President Trump’s revolutionary policy agenda, which is proceeding at Blitzkrieg speed, will introduce upside inflationary risks and downside growth risks. The concerns are limited to the U.S. economy. Europe is likely to fair even worse and possibly Asia, too. The disparate possibilities are reflected in today’s market action.

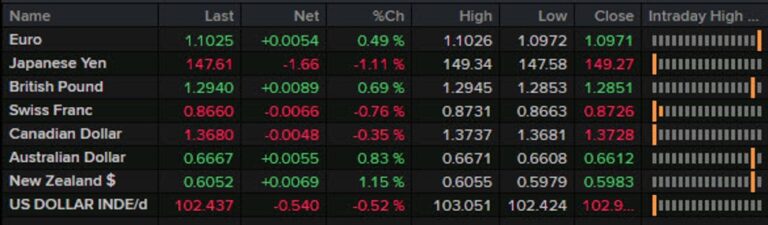

- The dollar rose overnight by 0.7% against the yen, Swissy, and kiwi, 0.6% versus the euro, loonie and Australian dollar, and 0.3% relative to the Mexican peso and sterling.

- U.S. equities opened today on a rising note even though equity markets had closed down 1.8% in Indonesia, 1.5% in Taiwan, 0.7% in South Korea and 0.3% in Hong Kong. European stock markets are down at least 0.7% in Germany, Italy, France, and Spain.

- The ten-year U.S. Treasury yield’s rise of four basis points was matched by the increase in the Japanese JGB yield but more than increases in British, French, Italian and Spanish yields.

- Prices rose for gold, oil and especially bitcoin.

The second estimate of U.S. GDP growth last quarter remained unrevised from the earlier 2.3% reading, but that didn’t prevent upward revisions in the measured inflation pace of the PCE deflator (to 2.4% from 2.3%) and the core PCE price deflator from 2.5% estimated earlier to 2.7%. A 4.2% annualized increase in personal consumption dominated last quarter’s growth. Government spending, residential construction, and even net exports also made positive contribution to GDP growth, while inventories and non-residential business investment exerted drags. Real GDP grew 2.8% on average during calendar 2024 and 3.16% per annum in the Biden years from 1Q 2021 to 4Q 2024. That was 1.3 percentage points faster than the net 1.86% per year growth achieved during Trump’s first term. Juxtapositioned against the changes of U.S. non-farm employment (down 2.75 million Trump 1.0, then +16.2 million Biden), the widespread impression by voters last year that the economy would perform better under Republican than Democrat stewardship highlights the dominance of inflation in shaping impressions of economic performance.

A 5.2% year-on-year decline in U.S. pending home sales during January was the biggest decline in six months, and the Kansas City Fed’s manufacturing survey index dropped to a five-month low in February.

It seems highly doubtful that the strength of U.S. consumer spending last quarter continued in the present one. Measures of consumer sentiment have hit an air pocket, and new jobless insurance claims leaped 24k last week to an 11-week high of 242k, lifting the 4-week average to a 9-week high. Durable goods orders, on the other hand, rebounded by a sharper-than-expected 3.1% in January after dropping 2% in November and a further 1.8% in December.

America’s persisting economic expansion compares favorably with Euroland’s sputtering one, and that is reflected the widening gap between the monetary policies of the Federal Reserve and the European Central Bank. Fed officials have signaled that any further reduction in its interest rate is unlikely until late this year. The ECB today published minutes from its policy review in late January. Officials had then cut the deposit rate by 25 basis points to 2.75%, and the minutes welcome the drop in inflation and project another year of weak growth.

There was a clear case for a further 25 basis point rate cut at the current meeting, and such a step was supported by the incoming data. Members concurred that the disinflationary process was well on track, while the growth outlook continued to be weak. Although the goal had not yet been achieved and inflation was still expected to remain above target in the near term, confidence in a timely and sustained convergence had increased, as both headline and core inflation had recently come in below the ECB projections. In particular, a return of inflation to the 2% target in the course of 2025 was in line with the December staff baseline projections, which were constructed on the basis of an interest rate path that stood significantly below the present level of the forward curve. At the same time, it was underlined that high levels of uncertainty, lingering upside risks to energy and food prices, a strong labor market and high negotiated wage increases, as well as sticky services inflation, called for caution.

The February reading for economic sentiment in the euro area rose to a 5-month high of 96.3 in February, still well below 119.5 reached in October 2021. The mood in the services sector weakened, however.

Consumer confidence in February eased in Ireland to a 2-month low from a 6-month high in January and also fell to 9-, 8- and 7-month lows in Finland,Sweden. and Portugal. In Italy, consumer sentiment and manufacturers’ business confidence printed at their best levels in seven and six months, respectively.

Producer price inflation of 0.8% in January in Malaysia reached a 6-month high, having previously declined from 13.2% at end-2021 to -48% in June 2023.

Spanish consumer confidence rose to an 8-month high of 3.0% this month from a 42-month low of 1.5% last September, and French PPI inflation, although still negative at -2.1%, was at a 13-month high.

A 0.2% quarterly rise of Swiss GDP in 4Q 2024 represented the second deceleration in a rose. Compared to a year early, Swiss GDP rose 1.5% in 4Q and 1.3% for all of 2024.

Icelandic consumer price inflation of 4.2% this month was its lowest reading in four year and down from the peak of 10.2% two years ago.

President Trump’s tariff policy in Canada paints that country as a predatory trader, but that economy experienced global deficits in 2024 of C$ 15.602 billion in the current account and C$ 7.371 billion in its goods and services trade balance.

Copyright 2025, Larry Greenberg. All rights reserved. No secondary distribution without express permission.

Tags: ECB minutes, euro area economic sentiment, U.S. GDP

ShareThis

ShareThisYou can leave a response, or trackback from your own site.