Unease about the Future – Currency Thoughts

Unease about the Future

February 25, 2025

Equities this Tuesday did poorly in the Pacific Rim, closing down 2.4% in Indonesia, 1.8% in New Zealand, 1.4% in Japan, 1.3% in Hong Kong, 1.2% in Taiwan, 0.8% in China and 0.6% in South Korea.

Digital money experienced a stellar 2024 but now two months into 2025 is fast approaching what constitutes as a bear market. The price of Bitcoin slumped 3.1% overnight, bringing its slump since mid-December to 18.8%.

America’s global political leadership, which provided the glue that prevented a super-power war for over 75 years, has undergone a huge makeover in this second presidential term of Donald Trump. His unorthodox style carried the MAGA movement to victory in November but hasn’t persuaded global or even domestic financial markets that better economic days lie ahead. Indicators of U.S. consumer and business confidence have faltered. The post-Covid spike of inflation, which drove Americans to pursue significant change — any change — is rising instead and creating concerns that growth is poised to slow at a time when scope for monetary relief is limited and equity values look over-valued by some measures.

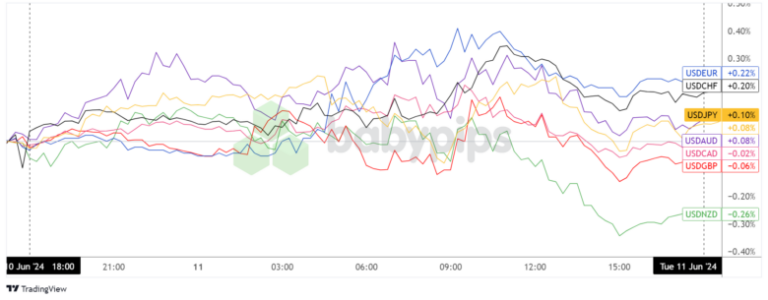

With the U.S. trade deficit taking a prominent role in the new U.S. government, the intuitive dollar bias would seemingly be toward depreciation, but the use of tariffs in addressing the problem persuaded forecasters to initially project a stronger dollar as Trump 2.0 launched. In choppy trading since the January inaugural, the greenback has in fact dropped 4.2% against the yen, 2.0% versus the Swiss franc and 1.5% against the euro.

Today’s light data menu featured revised German GDP figures, an assortment of price reports, and some central bank decisions. U.S. consumer confidence, house prices, and the Richmond and Dallas Fed manufacturing indices arrive later this morning.

German real GDP in the final quarter of 2024 contracted by 0.2% both compared to the prior quarter and versus the level a year earlier. This was the third decline in five quarters, and real growth in calendar 2024 was -0.2% as well and marked an extension to seven years of meager growth. Prior to Covid, GDP had risen only 1.1% in 2018 followed by 1.0% in 2019, and GDP in 2024 was on average only 0.3% above its level in 2019. Last quarter saw a substantial drag on economic growth from net foreign demand, with exports falling 2.2% and imports increasing 0.5%. Personal consumption edged just 0.1% higher, and business investment in machinery and equipment dropped 0.3%.

Corporate service price inflation in Japan was at 3.1% in January for the third time in four months.

Icelandic producer price inflation, which had swung from 29.7% in April 2022 to -7.0% a year later, jumped two percentage points to a 24-month high of 9.1% last month.

Producer price inflation in the Czech Republic, in contrast imploded from a 2.8% 19-month high in December to just 0.5% in January.

New car sales in the European Union went up just 0.8% in 2024, well down from the 13.9% advance in 2023.

Britain’s monthly distributive trades survey recovered only one point to -23 in February, remaining well weaker than last September’s reading of +4.

In its first change since May 2023, the Bank of Israel‘s policy interest rate had been cut by 25 basis points in January but was left unchanged at 4.5% at this month’s review. Israeli consumer price inflation of 3.8% is at a 16-month high and above the central bank target of 1-3%. The rate was hiked several times between April 2022 and May 2023 from 0.10% to a peak of 4.75%. A releases statement explains that “in view of the continuing war, the Monetary Committee’s policy is focusing on stabilizing the markets and reducing uncertainty.”

South Korea’s Base Rate peak of 3.5% had been maintained from January 2023 until an initial cut last October. That incremental reduction of 25 basis points was followed by another in November but not changed at this year’s first Bank of Korea policy review. But easing resumed today via a cut to 2.75% from 3.0%. In undertaking this third cut, which markets had been led to expect, officials wrote, “Although concerns about foreign exchange markets still remain, inflation stabilization has continued along with an ongoing slowdown in household debt, while the growth rate is forecast to decline significantly.” The latest South Korean inflation reading of 2.2% was close to the 2.0% target.

Three reductions in the National Bank of Kyrgyzstan policy interest rate totaling 500 basis points were undertaken between November 2022 and May 2024. At 9.0%, the rate after being kept steady today remains at its lowest level since February 2022. CPI inflation in its economy had dropped from a peak in February 2023 of 16.2% to a 55-month low of 3.8% in August 2024. The subsequent reacceleration of inflation to a 13-month high of 6.7% (still within the 5-7% target corridor) has kept policy easing on hold.

From a peak of 13.0% maintained for 13 months, Hungary’s central bank interest rate was lowered 225 basis points during the final quarter of 2023 and by a further 425 bps to 6.5% last year. As analysts expected, this level was maintained at today’s policy review. From low readings during 2024 of 3.0% overall and 4.0% core, consumer price inflation has reaccelerated sharply to 5.5% total and 5.8% core in January 2025. Forward guidance has accordingly turned more hawkish and is urging patience: “Geopolitical tensions, a volatile financial market environment, and risks to the outlook for inflation warrant the maintenance of tight monetary conditions.”

Copyright 2025, Larry Greenberg. All rights reserved. No secondary distribution without express permission.

Tags: Bank of Korea, German GDP, National Bank of Hungary, National Bank of Kyrgyzstan

ShareThis

ShareThisYou can leave a response, or trackback from your own site.