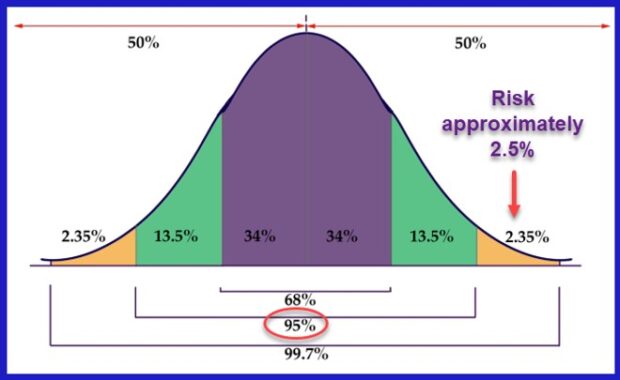

Using 2 Standard Deviations to Determine the Risk of Exercise of a High Implied Volatility Stock When Covered Call Writing

Portfolio overwriting (PO) is a form of covered call writing where, in addition to generating cash flow, we also want to retain the underlying shares. Achieving both goals may become more challenging when employing high implied volatility (IV) securities. In this article, a real-life example with Intel Corp. (Nasdaq: INTC) will be used to analyze such a scenario.

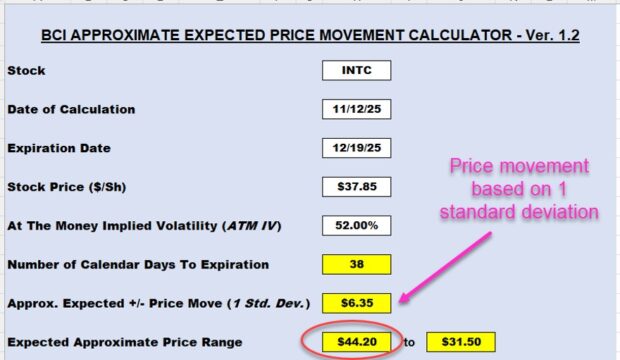

Real-life example with INTC on 11/12/2025

- INTC trading at $37.85

- The near-the-money $38.00 strike shows an IV of 52%

- IV stats are based on 1-standard deviation (1-SD) and 1-year timeframes which need to be converted to the timeframe for the contract in question

- The BCI Expected Price Movement Calculator will do just that

- The BCI Expected Price Movement Calculator will be used to determine an out-of-the-money strike which has a16% risk of being breached (subject to expiring in-the-money and at risk of being exercised or sold)

- We will double the expected price movement to then calculate the 2-SD amount which will provide a strike with only an approximate 2.5% probability of being breached

INTC option chain on 11/12/2025 showing an ATM IV of 52%

BCI Expected Price Movement Calculator to Select PO Strikes Based on 1 Standard Deviation/ 16% risk factor

- If a 16% risk factor is acceptable, share price is expected to move up or down by $6.35, resulting in a strike selection of $44.00.

- A 2 SD strike is calculated by doubling $6.35 to $12.70, leading to a strike of $50.00 ($37.85 + $12.70)

Standard Deviation Bell Curve showing risk factors of 16% (1 SD) and 2.5% (2 SDs)

- 1 SD risk: Green + brown fields on the high end

- 2 SD risk: Brown field only on the high end

Cash flow using this 2 SD approach with this high IV stock

- The $50.00 strike had a premium of $0.46 for the 12/19/2025, 38-day trade.

- This resulted in an initial time-value return of 1.22%, 11.67% annualized.

- Since the $50.00 strike was so deep OTM, an additional 32.10% of upside potential was also available.

Discussion

When using portfolio overwriting with high IV stocks, generating strikes using 2 SDs can result in lower-risk trades which can still generate significant cash flow. Strike selection is always based on both initial time-value return goal range as well as personal risk-tolerance.

Using stocks and stock options to develop a low-risk, wealth-building strategy for retail investors. Selling puts is a strategy similar to, but not precisely the same as, covered call writing. Mastering either strategy is a huge opportunity for retail investors to secure our financial futures. Mastering both will allow us focus on the best investment choices depending on market conditions and personal risk tolerance.

Free training resources

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to publish several of these testimonials in our blog articles. We will never use a last name unless given permission:

Thanks Alan (and Barry) for last night’s session.

I thought it was clear, for what it’s worth.

I have been using the CEO approach since early last year and it’s doing great (except for the 3 weeks I spent in Morocco – should have not set up trades – I know better).

Take care.

Frank

_____________________________________________________________________

_____________________________________________________________________

Upcoming events

1. Hollywood Florida Money Show

April 8: Trading Panel

April 9: 2-hour Master Class

3:30 – 5:30

The Put-Call-Put (PCP) or Wheel Strategy

Using Both Covered Call Writing and Put-Selling to Generate Monthly Cash Flow

Selling stock options is a proven way to lower our cost-basis and beat the market on a consistent basis. Two such low-risk strategies are covered call writing and selling cash-secured puts. This presentation will detail how to incorporate both strategies into one multi-tiered option-selling strategy where we either generate cash-flow or buy shares of stock at a discount. I refer to this as the Put-Call-Put (PCP) Strategy, also referred to as the wheel strategy.

The basics and pros and cons of low-risk option-selling strategies will be discussed as well as an analysis of a real-life example and introduction into the BCI Trade Management Calculator (TMC). This seminar is appropriate for those who look to generate modest, but consistent, returns which will enable us to potentially beat the market on a consistent basis while focusing on capital preservation.

April 10: Portfolio Overwriting

11:40 – 12:25

2. Sarasota Investment Group

Portfolio Overwriting: A Form of Covered Call Writing

Wednesday April 22, 2026

Details to follow.

3. BCI Educational Webinar #10: The Put-Call-Put (PCP) or “Wheel Strategy”

Thursday May 14, 2026, at 8 PM ET

Using both covered call writing & cash-secured puts in a multi-tiered option selling strategy. A 68-day real-life example taken from one of Alan’s portfolios will be analyzed.

BONUS: Barry will share a real-life credit spread trade using our BCI Conservative Credit Spread Management System.

Discount coupons and a live Q&A session will follow the presentation.

4. American Association of Individual Investors: NYC Chapter

June 10, 2026, at 6 PM – 8 PM ET

More information to come.

5. MoneyShow Masters Symposium Las Vegas

July 20 – 22, 2026

Caesars Palace Hotel

Las Vegas

Details to follow.

6. Toronto Money Show

September 24 – 25, 2026

MaRS Center, Toronto Canada

7. Orlando Money Show

October 5 – 7, 2026

Hilton Orlando Lake Buena Vista

Details to follow.

Source link