November 2025 DDD

| After a month marked by failed breakouts in the riskiest stocks, this morning on the Open Bar, I took a step back and reviewed some of the most bearish groups. Warning Signs from the “New 3 B’s” It has been a teflon run off the April lows, but the market has started to show some cracks of late. Key risk-on areas — Regional Banks, Homebuilders, and Bitcoin — are flashing warning signs, suggesting heightened downside risk. Here are the charts, showing dynamic support levels off the April lows. |

| |

| The bottom line is bad things happen below VWAP… and that’s where these guys are living for now… besides the banks. Regional Banks They keep holding on, but I doubt they will end up looking any different from homebuilders over time. If the other B’s roll, look for banks to follow. The big banks, though, are another story. They are built differently, and I think they can continue to act differently… staying strong despite weakness from the little guys. Homebuilders Homebuilders currently look like the worst of the worst. The weakness comes amid some sector-specific headwinds, and the short-term outlook suggests more downside could be ahead. If rates keep ticking higher, this group is likely to lead lower. Simple as that. Bitcoin: “guilty until proven innocent” Bitcoin continues to lose ground, despite its big-cap tech peers showing strength. Until it can reclaim and hold key levels, we want to treat this as a topping pattern. We’re seeing very similar bearish action and patterns playing out in Ethereum and Solana, which we are monitoring closely for supporting evidence. Potential Dollar Headwinds DXY might be the single most important chart right now. Major currencies –including the Canadian dollar, the pound, the euro, and the yen — are already breaking down relative to the USD. If those are all tops, then this is going to be a durable bottom in the US Dollar Index. If that plays out, the current market weakness is likely to expand beyond the 3 B’s, and dollar headwinds could throw a wrench in the broader risk asset rally. We went through all of these charts and key developments in The Open Bar this morning. Click here to watch the replay. The main takeaway is that evidence continues to build in favor of us shifting back to “keep money” mode… and we are. After all, we need to preserve what we have so we can take advantage of the good times… I have a feeling they’ll be back before we know it. |

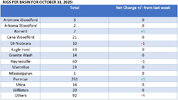

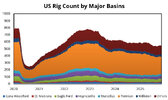

In this week’s newsletter, we will take a quick look at some of the critical figures and data in the energy markets this week.

We will then look at some of the key market movers early this week before providing you with the latest analysis of the top news events taking place in the global energy complex over the past few days. We hope you enjoy.

– OPEC+ surprised oil markets by announcing a pause in its scheduled return of voluntary cuts throughout Q1 2026, having agreed on a minor 137,000 b/d increase for December 2025.

– According to media reports, Russia was the largest proponent of the temporary supply hike pause, giving OPEC+ more time to assess the impact of sanctions on Russian crude production.

– Whilst Saudi Arabia was the main driver behind triple monthly increases earlier this year, it supported Russia’s motion for 2026, arguing that Q1 will see notable inventory builds across the globe and there would be little incentive to worsen the glut.

– OPEC+ countries have collectively boosted their quotas by 2.9 million b/d this year to date, half of the oil group’s total 5.85 million b/d voluntary cuts.

– In real terms, however, OPEC+ boosted production by only 70-75% of their respective targets as many analysts argue these volumes were already in the market, largely unaccounted for.

Market Movers

– UK oil major BP (NYSE:BP) has agreed to sell minority stakes in its US onshore pipeline assets in the Permian and Eagle Ford basins to investment firm Sixth Street for $1.5 billion, under pressure from activist investors to divest.

– US oil major Chevron (NYSE:CVX) has signed a deal with Guinea Bissau to explore two offshore blocks in the African country’s offshore sector, taking a 90% working interest in both with national oil company Petroguin holding the remaining 10%.

– Latin America-focused upstream firm Geopark (NYSE:GPRK) has rejected an unsolicited acquisition proposal from peer producer Parex Resources in a deal worth almost $1 billion, building up an 11.8% position in the company before.

– Italy’s energy major ENI (BIT:ENI) has signed a deal to assess five offshore oil and gas blocks in Sierra Leone, a West African country that is still yet to see a commercially viable discovery despite its proximity to Ivory Coast and Ghana.

– Libya’s National Oil Company announced a new oil discovery in the Ghadames Basin in the northwestern part of the country, with its H1-NC4 exploration well producing almost 5,000 b/d.

Tuesday, November 04, 2025

OPEC+ paying heed to 2026 oversupply concerns did relatively little to wake up crude oil prices from their week-long slumber, seeing ICE Brent flat around $65 per barrel. Top oil executives meeting in Abu Dhabi this week tried to boost market sentiment, repeating all over that next year’s oil glut will not be as bad as thought, however an upside rally is only likely to materialize if the US-Venezuela tensions escalate into military action.

OPEC+ to Halt Output Hikes in 2026. Eight members of OPEC+ agreed to increasecollective output targets in December by another 137,000 b/d, as well as to pause the monthly hikes in the first quarter of 2026, citing ‘seasonality’ in stock builds and a weak demand outlook in the short term.

ADNOC and SLB Roll Out AI System to Optimize Oil Production. ADNOC has partnered with SLB and Cognite to deploy AiPSO, an AI-powered platform designed to optimize oil production across all 25 of its fields by 2027. Already active at eight sites, the system integrates SLB’s Lumi platform and Cognite Data Fusion to analyze millions of real-time data points, enabling engineers to diagnose and optimize wells in minutes.

Argentina Boosts Its LNG Portfolio. Argentina’s state oil firm YPF (NYSE:YPF) signed a deal with Italy’s ENI and ADNOC’s investment arm XRG to build a 12 mtpa LNG export facility at a port in the Patagonian province of Rio Negro, with gas to be sourced from the Vaca Muerta shale play.

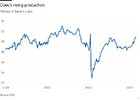

Brazil Production Hits a New Record. Brazil’s pre-salt crude production is booming, as confirmed by September output statistics from the country’s regulator ANP that show production at 3.91 million b/d last month, up 13% from a year prior, with the Tupi field producing a whopping 820,000 b/d.

Permian Consolidation Is Still Not Over. US shale producers SM Energy (NYSE:SM) and Civitas Resources (NYSE:CIVI) agreed to a $12.8 billion merger to create one of the largest Permian-focused independent upstream firms in the country, holding a total of 823,000 net acres across the US.

Qatar Flaunts 2026 Expansion Start. The chief executive of QatarEnergy Saad al-Kaabi announced that the company’s large-scale North Field expansion project will produce its first LNG in the second half of 2026, adding 49 mtpa of liquefaction capacity to the country’s currently operational 77 mtpa.

Ukraine Strikes Russia’s Black Sea Port. Ukraine drone strikes have damaged oil terminal infrastructure in Russia’s Black Sea port of Tuapse, loading on average 240-250,000 b/d of refined products, with an oil product tanker docked in the port also catching fire from falling debris.

Venezuelan Exports Shrink on Diluent Dearth. Venezuela’s oil exports dipped by 26% month-over-month to 808,000 b/d in October as shrinking inventories of much-needed diluents restricted heavy crude upgrading, with Chevron shipping 16% of total outflows (equivalent to 128,000 b/d).

Glencore Shuts Canada’s Key Smelter. Mining giant Glencore (LON:GLEN) is planningto shutter its Horne smelter, Canada’s largest copper-producing plant, due to a long-standing lawsuit over arsenic emissions in Quebec and more than $200 million required to modernize it to keep it operational.

Ørsted Divests Key Asset. Denmark’s embattled wind developer Ørsted (COP:ORSTED) sold a 50% stake in Britain’s Hornsea 3 offshore wind farm to US investment firm Apollo Global Management for $6.1 billion, a record sum for a wind project, seeking to avoid a crippling credit rating downgrade.

Pakistan Cuts Down on LNG Deals. Pakistan has agreed to cancel 21 LNG cargoes in 2026-2027 under its long-term deal with Italy’s ENI (BIT:ENI), also launching talks with QatarEnergy to defer term cargoes or potentially even resell them as gas demand continues to plunge in the country.

Iraq Bans Fuel Imports. Iraqi Prime Minister Mohammed al-Sudani has signed a decree suspending the country’s gasoline, diesel and kerosene imports as domestic refining production is now exceeding local consumption, having imported only 20,000 b/d of gasoline in October 2025.

LNG Freight Rates Soar Again. Tight availability of LNG carriers in the Atlantic Basin has pushed daily freight rates in the region to their highest since August 2024, trending around $61,500 per day, whilst ample supplies across the Asian markets kept freight there much lower, at $42,250 per day.

Stakeholders Urge Rio to Derail Teck-Anglo Merger. Activist fund Pallister Capital has urged Australia’s mining giant Rio Tinto (NYSE:RIO) to challenge Teck’s 53 billion merger with Anglo American, with one month left until the Anglo Teck shareholder vote planned for December 9.

|

|

|

|

|

|

|

|

|

|

|

|

")

|

- This is what evolution looks like in a bull market.

- Adapt. Rotate. Profit.

- Do more of what’s working, less of what’s not.

Sure, some people still act like Neanderthals, but it was our species’ ability to adapt together that kept us alive.

Today, as traders and investors, we face a similar test. The stakes aren’t life and death anymore – they’re financial survival. Adapt or go bankrupt.

Markets create similar evolutionary pressures our ancestors faced. Only now, instead of hunting for food or shelter, we’re hunting for the current market regime – and adjusting our strategies to thrive within it.

That’s where most investors fail. The inability to adapt is what separates the many losing portfolios from the few that survive and thrive.

Because let’s be honest – most investors out there still behave like Neanderthals. We see it every day.

But just like their namesake ancestors, they’ll eventually go extinct (go broke).

Our job, as rational and adaptive humans, is to profit from their mistakes.

It’s a massive advantage to not act like a Neanderthal.

Use it.

Rotation Rotation Rotation

In bull markets, everybody gets a turn. That’s why understanding rotation – and adapting to it – is so critical.

If you can’t recognize where the money’s moving, you’ll get stuck holding the wrong stocks, looking like one of those hard-headed Neanderthals we just talked about.

Remember how bad Healthcare looked for so long? It felt like the sector underperformed forever. And within it, Biotech was left for dead.

Now? Healthcare is one of the strongest groups in the market – and Biotech stocks are leading the charge.

Take a look at this three-month performance chart of U.S. indexes and sectors. I’ve included both the Equal-Weighted Biotech ETF (XBI) and the Market-Cap-Weighted Biotech ETF (IBB) so you can see just how strong this group has been – no matter how you slice it:

This is what sector rotation looks like.

This is what bull markets look like.

When Small-Cap Healthcare – especially Biotech – started working for us, we leaned in. We bought more. Then when it kept working, we bought even more.

That’s how we operate at TrendLabs: more of what’s working, less of what isn’t.

Notice how we only bought one bank stock? It didn’t work, we got stopped out, and now we don’t own any regional banks. Simple.

Meanwhile, my portfolio’s packed with Biotech winners – you’d think I had a lab coat hanging in my office. Those of you who know me well know that I’m the furthest thing from a scientist.

So the only question now is:

Who’s next?

Where’s the next rotation coming from – and how do we get there first?

Oil Refiners Hit New All-Time Highs

If everyone gets a turn, then eventually Energy’s turn will come too.

Here’s the Oil Refiners ETF (CRAK), which just finished October with its highest monthly close in history.

Below it, you’ll see the broader Energy Sector ETF (XLE) – similar setup, but still stuck at the same levels it was back in the summer of 2008.

If you’re not a Neanderthal, you can do the math – that’s more than 17 years ago.

That’s a long time to be stuck in the cave.

But I think their time is coming…

We started with one Oil & Gas name a few weeks back. Then we added two more last week. And by the looks of it, we’ll probably be adding again soon if they keep working.

That’s what adaptation looks like.

Do more of what’s working. Do less of what’s not.

It’s not complicated – it’s evolution.

The investors who survive are the ones who evolve with the market. The rest?

They go extinct.

Be a Homo sapien. Not a Neanderthal.

A US recession was at one point taken as the base case for last year. Somehow, it still hasn’t happened. The Bloomberg News count of stories citing “recession” has dropped to its lowest since the data starts in 2015. This crude measure isn’t scientific, but comes at a time when the economy appears to be humming along, amid all the anger over global trade policies.

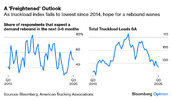

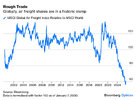

The S&P 500 is up 16.5% for the year, and that is doing a good job of masking visible signs of weakness creeping up elsewhere. Just take a look at the freight and logistics industry. Its belated recovery from the pandemic-era supply chain crisis has been scuttled by 2025’s unraveling trade policy.

Heading into this year, Lindsay Bur of the American Trucking Associations points out that many carriers were optimistic for a turnaround. But tariffs dealt a blow, sending the industry further into uncertainty. Renewed pessimism shows up in the latest Bloomberg Truckstop Truckload Survey, where respondents expecting a rebound have fallen to the lowest level since last fall. That negativity isn’t surprising as the pernicious slide in seasonally adjusted total truckloads continues unabated. Loads are no greater now than they were 10 years ago:

Evidently, fewer goods are being moved. Craig Fuller of FreightWaves describes this as a goods recession. His analysis of high-frequency data from their proprietary platform shows that there’s been a problem with overcapacity. Driver employment remained steady, but freight has declined. A similar oversupply of drivers pre-Covid led to plummeting rates that wiped out many smaller carriers:

It’s therefore not surprising that logistics stocks are near multi-year lows after their post-pandemic highs. The sector’s own troubles have only compounded its underperformance against the broader market:

The problem isn’t restricted to the US. Mercantilism, countries’ attempt to be self-reliant and do without trade, has had a terrible impact on global air freight:

Is there a way out of this quagmire? It could conceivably come from the immigration crackdown. Bloomberg Intelligence’s senior logistics analyst Lee Klaskow argues that a revival needs to balance freight demand and the supply of drivers. Enforcement of English-language proficiencyrequirements could constrain driver capacity, helping rates recover. Fuller notes that the crackdown could potentially impact as many as 600,000 drivers over the next two years.

jog on

duc

Source link