April DDD 2026

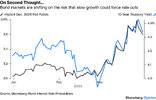

Further, the logic of bonds is that they act as a shelter in times of stress — which means investors buy them during extreme uncertainty and conflict, like the past month. Thus it’s always been strange that the bond market unambiguously reacted to the Iran war’s inflation risk, but not to the threat to growth, and sent yields higher. Until now. Both yields and rate expectations for the Federal Reserve suddenly dipped Monday:

It’s not obvious why this happened when it did. Traders entered the crisis with leveraged positions, meaning that some of the rise in yields since then has come through a classic trading squeeze. Also, comments by Fed Chair Jerome Powell in the US morning helped further dispel the notion that rate hikes were a certainty. The immediate effect was to spark a sudden recovery in equities despite another dispiriting weekend of news from the Gulf. To quote one macro strategist:

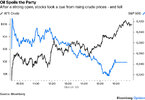

The classic measure of a growth scare is to track the performance of stocks relative to bonds. On that basis, although nothing like last year’s Liberation Day selloff, the fall in stocks has now brought them back to their level of inauguration week in January 2025. Since then, stocks and long bonds have exactly matched each other:Interesting. Equities trading much better because Fixed Income is trading much better. Fixed Income is trading much better because we suddenly chose to fear growth more than Warflation.

The bond market did allow a nice lift for stocks at the US opening, but it didn’t last. Even when handed an excuse for a rally, equities didn’t take it. That was mainly because of the oil price, with West Texas Intermediate, the main US benchmark, closing above $100 for the first time since the attacks on Iran began. (It fell later after the Wall Street Journal reportedthat Trump was considering ending the war without reopening the Strait).

As Points of Return has covered, the markets remain on alert for a relief rally, and this is deterring many from selling. Measures that normally gauge extremes of risk appetite suggest that people are now negative enough for a rally to start — but the problem is that this selloff isn’t a question of risk appetite. To quote Harry Colvin of Longview Economics:

Put differently, stocks are almost in the textbook world where they follow a “random walk” incorporating all news as soon as it is known. Usually, waves of sentiment ensure that moves aren’t truly random. But now, we need to keep watching the news and be prepared to react. It’s the uncomfortable reality of the moment.Equities are in an environment when you have all these technical and sentiment risk appetite models that really suggest you should get involved and buy again. But markets aren’t really driven by risk appetite so much as news flow. If it does rally it’s probably an opportunity to unload more risk, absent some sort of resolution of this conflict.

Market catharsis — the moment when fear finally overcomes greed and share prices stage a big fall to catch up with bad news — is surprisingly elusive. Because it depends on mass sentiment as well as the news, hope can delay it, but not indefinitely.

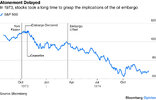

The relevant example for today is, yet again, the Yom Kippur War of 1973, the oil embargo that ensued, and the subsequent bear market in stocks. The conflict had a worse impact on the US equity market than either of the world wars, but it took a while for markets to grasp that.

A coalition of Arab nations led by Egypt and Syria attacked Israel on Yom Kippur, the Jewish Day of Atonement, which fell on Oct. 6. In response, US President Richard Nixon organized an airlift of arms to Israel, which prompted the world’s most important oil exporting countries to impose an embargo Oct. 19.

The UN-negotiated ceasefire followed on Oct. 25; the embargo remained in place. The S&P 500 peaked the next day, at which point it had gained 2.3% since the outbreak of hostilities. Only then did catharsis ensue:

Even after the embargo was lifted the following March, US stocks had almost 40% further to fall before reaching their 1974 low. The gas lines and trauma to public sentiment didn’t immediately dissipate.

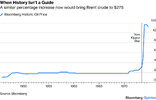

If this seems baffling in hindsight, bear in mind that history at that time gave no useful guidelines. For the first quarter-century after World War II, the oil price was stable and controlled. It began to pick up after the end of the dollar’s peg to gold in 1971, but nothing prepared traders (or the broader population) for what would happen once the embargo came into force:

If the oil price were to repeat its 277% rise in the six months following Yom Kippur, that would imply a price for Brent crude of $275 by the end of this year. That seems almost unimaginable today — just as nearly $12 oil was in 1973.

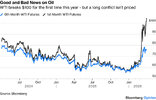

What is perhaps worrying is that crude futures show that traders are behaving as they did in the 50 years that followed the Yom Kippur War, and working on the assumption that any spike will be reasonably short-lived. WTI futures for nine months ahead are still below their level of two years ago, even as short-term prices move far ahead:

The futures market may well be right, but if it isn’t, the bad news will have to be incorporated into oil and stock prices.

Hard economic impacts of big geopolitical shocks take a while to have an effect, while market prices, refracted through human emotions, take even longer. For now, traders are guarding against the considerable upside risk that the Iran conflict is resolved without significant long-term effects on oil supply. If the major interruption to supply actually happens, then stock market catharsis still lies in the future.

The value of stocks, textbooks will tell you, ultimately depends on the discounted present value of the future cash flows they will generate. If the discount rate goes down — as it did when bond yields dipped Monday — that will help increase the value. More importantly, and harder to track, higher estimated earnings will tend to push up the price we should pay now.

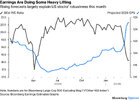

So far, the conflict has had minimal effect on earnings estimates. If we exclude the Magnificent Seven platform stocks, indeed, we find that 2026 earnings per share estimates for Bloomberg’s index of the “other 493” of the 500 biggest US stocks have risen sharply this month:

That gives greater reason to hope for the future, but also casts stocks’ resilience in a different light. The Iran war’s hit on forward earnings multiples has been almost as serious as last year’s selloff around the Liberation Day tariffs drama. The loss of confidence in stocks looks less severe because of the earnings momentum, but the hit has been serious.

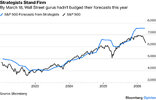

That momentum might also help to explain why Wall Street strategists have reacted with calm to the conflict. Last polled by Bloomberg News colleagues led by Lu Wang on March 18, they haven’t budget their end-year estimates at all. That mirrors how they behaved during the Liberation Day selloff last year, and it worked then:

The first quarter is about to end. If companies have bad news to get off their chests about the effect the war is having on the bottom line, they’ll probably start pre-announcing once the long Easter weekend is over. Until such a time as that happens, what remains a positive earnings outlook remains a good reason for delaying catharsis. If profits are really growing like this, it’s invidious to get out of stocks now and let someone else buy them cheap.

What is driving the attack and war on Iran?

Recently, energy analyst Anas Alhajji posited the following:

“The closure of the Strait of Hormuz dramatically heightens the perceived risks and costs of relying on Gulf oil and LNG. This shift makes American oil and gas exports far more competitive on the global market.

Fertilizers represent another key vulnerability. Gulf countries are major exporters of fertilizers, and roughly one-third of global fertilizer exports typically passes through the Strait of Hormuz—primarily destined for Asian markets, especially India.”

See: https://anasalhajjieoa.substack.com/p/public-no-paywall-the-hormuz-crisis and x.com/anasalhajji

In recent interviews, Alhajji also observed that in recent years liquid natural gas (LNG) carriers have not been able to secure insurance to sail from the Persian Gulf to Europe through the Red Sea/Suez Canal necessitating sailing an extra 4,000 mi. (7,000 km) around Africa to Europe while tankers containing crude or other fuels could easily secure insurance to transit the Red Sea route.

With the added circumnavigation of Africa, the distance from the Persian Gulf to Europe is now greater than from the US Gulf Coast. This has contributed to the US, in a few short years, now having become the dominant supplier of LNG to Europe providing fully 60% of Europe’s imported supply before the conflict started on February 28.

Is The Persian Gulf Intentionally Being Burned Down?

With the we see daily flip-flopping the marketing of the war effort has become a farce. Apparently.However, as mentioned previously, the vast scale of the Iranian military’s missile and drone programs were well known before the attack began as was Iran’s resulting attacks on countries supporting the US/Israeli effort. Nobody was shocked.

It is thus no surprise that today oil and LNG production and shipping facilities are on fire throughout the Gulf and that production, refining, and shipping capacity will likely be impaired for years to come if things go well.

This evening’s headline in the Wall Street Journal fits in with the strategy of just burn it all down and leave:The question then arises if simply triggering destruction of the vital Persian Gulf energy infrastructure was the primary goal of the entire conflict? Iran is not keen to stop, given the existential threat that it appears to face, until the threat it faces is terminated.

If this is the case and the war continues, there may not be much left when the conflict does stop.

| |

Petrodollar 2.0.

The Food Problem

Asia / Oceania (Australia + South Pacific) are especially dependent on fuel and fertilizer exports originating in the Persian Gulf.Already, much of this area is warning of, or has already started, fuel rationing, work from home, shortened work weeks, etc.

In addition, northern hemisphere planting season is currently underway and some impacts of continued disruption of fertilizer shipments from the Persian Gulf simply can’t be mitigated.

Famine, sudden price inflation, and extreme economic upset are cards in the deck.

If they are pulled, they will not be well received.

President Trump’s threat to bomb Iran’s water supply would constitute his most dramatic breach of the laws and norms designed to protect civilians in wartime, Axios’ Zachary Basu and Dave Lawler write.

- Why it matters: The Iran war is the biggest test of what Trump’s contempt for “politically correct” war-fighting looks like in practice.

- But the U.S. has been almost exclusively targeting Iran’s military and nuclear program up to now.

- The threat to hit civilian infrastructure shows how intent Trump is on finding ways to increase the pressure on Tehran, even if that means flouting the generally accepted principles of warfare.

- Defense Secretary Pete Hegseth, then a Fox News host, spent Trump’s first term lobbying privately and on air to secure pardons for soldiers convicted of war crimes.

- Like other countries in the severely water-stressed region, Iran relies heavily on desalinated water.

- A senior U.S. official told Axios the idea was to use strikes to pressure Iran to negotiate: “The Iranians want this to stop, too. Don’t be mistaken. Their economy is broken. A couple of sorties, they will have no power. A couple of Israeli sorties, they will have no water. There is a lot to lose if there’s no accommodation. Everyone will have to give, but we can get there.”

- The official cautioned that Trump has made no decision, and “he wants to make sure that things are proportionate in this war.”

- Trump stated his intent plainly, writing that the strikes would be “in retribution for our many soldiers” Iran has killed over the last 47 years.

- Reprisals against civilians — also known as collective punishment — are explicitly prohibited under the Geneva Conventions.

HOUSTON — As nuclear energy deals pile up, executives face a huge challenge: How to build multiple plants quickly, Axios’ Chuck McCutcheon writes.

- Why it matters: Nuclear is seen as critical to powering AI data centers, but the supply chains, workers and permits needed to build plants haven’t kept pace.

- Nvidia and Microsoft are joining forces to use AI tools to streamline nuclear construction, using virtual replicas that let engineers test changes.

- Aalo Atomics says it cut permitting time by 92% using Microsoft’s Generative AI for Permitting solution, saving about $80 million a year.

- Getting a qualified workforce fully up to speed to build many plants will take time, said Ross Ridenoure, Hadron Energy’s chief nuclear officer.

- “There will be, I think, a shortage initially, until the training programs catch up with the demand,” he told Axios.

Jeffrey Sonnenfeld, a professor at the Yale School of Management who is one of the nation’s premier CEO whisperers, is out today with “Trump’s Ten Commandments: Strategic Lessons from the Trump Leadership Toolbox,” including “Reducing Complexity to Simplicity” and “The Role of Grandeur, Image, and Heroic Aura.”

- Why it matters: “Like him, loathe him, or try in vain to look past him, Trump is the most consequential leader on the planet right now,” Sonnenfeld told me. The professor calls his book an “objective leadership analysis by [someone] who has known him for a quarter century.”

- Based on all those years of studying Trump, Sonnenfeld says the tactics include “divide and conquer, the sleeper effect of constantly repeating false information with unshakable confidence, starting negotiations by giving the other side a bloody nose rather than a handshake of trust, centralizing all power [in your own hands], personal grandiose branding on everything.”

Walking through a liquefied natural gas terminal is a good way to get a sense of how challenging it will be for the US to extract much benefit from energy supply disruption in the Middle East.

On Friday, as CERAWeek in Houston wound down, I joined a group of reporters on a visit to the Cameron LNG plant in Louisiana, a joint venture of TotalEnergies, Sempra, and a few other heavy industry companies. With annual exports of about 13.5 million tons, it’s actually relatively small by Gulf Coast standards. But it doesn’t feel that way. In this dense, sparkling web of pipes, tanks, and cooling towers spread over 500 acres, natural gas drawn from around the US is chilled to roughly the surface temperature of the dark side of the moon, liquefied, and pumped into tankers that carry it to the global market. On the day of our visit, the South Korean tanker SK Audace was loading cargo, hooked up to pipes so cold they were covered in a thick layer of frost despite the balmy bayou weather. As of Tuesday morning, the Audace was steaming past the Bahamas while Total’s gas trading desk fields bids from potential buyers in Europe and Asia.

Cameron was already cranking at maximum capacity before the war in Iran sent prices spiraling — especially attacks on the Ras Laffan terminal in Qatar, which knocked out 20% of the world’s LNG capacity. But while workers at the Cameron plant are now redoubling efforts to eke out a few thousand more tons with the existing system, there’s been no decision to expand the plant, my Total tour guides told me. One hour at Cameron is enough to understand the scale of design work and capital spending that would be required for that undertaking.

LNG might be selling at a premium these days, but so is much of the liquefaction and power-generating equipment an expansion would require. Construction firms are also overbooked, and labor in short supply. Those issues might be surmountable if energy company shareholders were confident about having a strong price signal for the foreseeable future. But they’re not, as Jack Fusco, CEO of rival exporter Cheniere Energy, observed during CERAWeek: “What you’re seeing with this type of volatility that seems to happen every four or five years, it’s just not good.”

A Kuwaiti oil tanker carrying two million barrels of oil caught fire after it was hit by an Iranian drone off Dubai, an attack that underscored the war’s deepening risks to the energy sector.

Oil prices remained volatile, rising early Tuesday before falling back to just above $110 a barrel on a Wall Street Journal report that US President Donald Trump told aides that he was willing to end the month-long conflict even if the Strait of Hormuz remained largely closed. Hours earlier, Trump hailed “great progress” in talks to end the war but also threatened that the US would “obliterate” Iran’s Kharg Island oil export hub if Tehran did not reopen the strait.

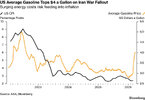

Meanwhile, the cost of the conflict is rippling through the US economy as average petrol prices rose above $4 a gallon for the first time since August 2022, though Federal Reserve Chair Jerome Powell said longer-term inflation expectations were “well anchored.” The global impacts have been more severe: Inflation is accelerating in Europe, with the EU’s energy chief urging Europeans to consider traveling less; South Korea is weighing imposing driving restrictions; and fuel shortages are hitting petrol stations across Africa.

A longtime oil and gas executive with links to the Trump family plans to use equipment from a sanctioned Russian gas project to open a major new export terminal in Alaska, he told Semafor. The project, dubbed Polar LNG, will eventually require $8-9 billion in investment and aims to have a capacity of 21 million tons per year, which would rank it among the largest LNG terminals in the country, with the first exports shipping out before US President Donald Trump’s term ends, CEO Joel Riddle said.

The spike in natural gas prices caused by the war in Iran, Riddle said, was generating “hurricane-force winds behind us to accelerate this project,” which would create a path for US gas to more readily reach markets in Asia. A separate project called Alaska LNG is racing ahead in parallel, but Polar LNG is angling to leapfrog it by buying LNG hardware and service ships that were originally destined for Russia’s Arctic 2 LNG terminal, which was sanctioned by the Biden administration, including equipment that is already located inside Russia. Acquiring pre-built equipment is critical for the project’s “speed to market,” Riddle said: “From a cold start, this would be impossible.”

That will require permission from the Treasury Department, which Riddle said he will be “laser-focused” on obtaining in the coming months. A Treasury Department spokesperson declined to comment. One investor in the project, Riddle said, is Gentry Beach, a college friend of Trump’s son Donald Jr. who has been pursuing a wide range of global energy and mineral deals through his firm America First Global.

Fears of global aluminium shortages that could affect the production of clean energy technologies intensified after Iran struck two major Gulf aluminium producers, sending prices to a four-year high. The Middle East accounts for 9% of the world’s production of aluminum, which is essential to a wide range of industries from transportation, construction, and packaging, as well as the manufacture of solar panels, electrical transmission systems, wind turbines, and EVs.

Export shipments to the US and Europe had already come to a halt because of the effective closure of the Strait of Hormuz, and Morgan Stanley economists singled out aluminium as carrying a high level of risk across the value chain. Andy Farida, an aluminium analyst at Fastmarkets, told Semafor that high prices would be passed on to end-users, ultimately causing demand destruction. “A prolonged shutdown (with little to no alternative supplies other than Russia and China) could cripple the supply of aluminium to support the production of clean and green technology,” he said, adding that relief could come “if governments allow some sanctioned Russian and Chinese aluminium to be imported.”

he estimated global loss in output from EV factories if battery supply exports from China were halted for a month — with facilities in the European Union accounting for over half the decline — according to analysis by the International Energy Agency. The Paris-based organization found “weak links” within battery, solar PV, wind, and heat-pump supply chains, each of which contain at least one step heavily reliant on Chinese supplies.

The analysis highlighted continued vulnerability caused by the concentration of cleantech supply chains in China, despite progress in diversifying downstream capacity. On Friday, Beijing initiated two counter-probes into US measures against such concentration, which it said “hinder trade in green products” by restricting exports to the US and slowing down the deployment of new energy projects after Washington launched investigations into its trading partners, including China.

China’s e-truck boom, like its electric car industry, is having a profound domestic and global impact. Almost 30% of new heavy trucks sold in China last year were new-energy models, compared to Europe’s 4%, while sales in California — the leading US e-truck market — remains in the hundreds, according to Rystad Energy. China’s rapid adoption “leaves the rest of the world in the dust,” one expert told Semafor. Truck makers, benefiting from a huge domestic market and tight-knit supply chains, are expanding as far afield as South Africa and Europe. This shift has far-reaching consequences for China, the world’s biggest fossil fuel importer: By 2030, the rollout of e-trucks is projected to lead to a 20% drop in Chinese diesel demand.

The sector’s success comes on the heels of the dominance of the Chinese EV sector, the prospects for which have been buoyed further by the Iran war driving up fuel prices. Industry behemoth BYD, for example, forecasts an uptick in its business, with its chairman telling analysts that the surging cost of energy would push the company’s sales to “another level.” It now projects annual overseas sales to hit 1.5 million this year, 15% higher than its earlier forecast. In one advert in Europe, the firm notes: “Fuel prices change, your plans don’t. Save money with a BYD.”

Five weeks into the Iran war — with the Strait of Hormuz still effectively shut, sending fossil fuel prices soaring, and the conflict threatening to expand rather than contract — there’s at least one clear winner: Renewables technologies such as solar, wind, and batteries. All are dominated by China, writes Semafor’s Andy Browne.

Even before the war broke out, experts had characterized the global struggle for the future of energy as one between a group of “Petrostates” led by the US — the world’s largest oil and gas producer — against “Electrostates” anchored by China, which supplies more than 70% of all the world’s green hardware.

The war has sharpened that contest, by showing once again how vulnerable the global economy is to shocks emanating from the Middle East. Crude prices are at multi-year highs, and threaten to surge further, raising the spectre of a global recession; natural gas supplies are also at risk, with attacks on LNG infrastructure in Qatar, a major producer. And around the industrialized economies of Asia, desperate governments are turning back to coal to fill the gaps.

Gasoline Goes Galactic: Prices Jump, Diesel Spikes, and the White House Feels the Burn

– Nationwide US gasoline prices topped $4 per gallon for the first time since August 2022, jumping to $4.018/USG as of March 31, raising domestic political risks for the Trump administration.

– With gasoline now up by more than $1 per barrel since the US attack on Iran, prices keep on rising despite the White House’s temporary waiver on the Jones Act to allow foreign-flagged vessels to move US fuel.

– California posts the highest gasoline prices across the country, with the cost of a gallon now at $5.887, up 27% from a month ago.

– The average national diesel price rose to $5.454 per gallon by the end of March, logging an even more impressive 45% month-over-month spike and creating a huge inflationary risk for consumer goods ahead.

– Arguably, the Trump administration’s last-resort lever to lower gasoline prices in the short term would be to introduce export restrictions – in the meantime, US gasoline outflows continue to average around 800,000 b/d, with Mexico taking in a third of those volumes.

Market Movers

– Kuwait Petroleum Corporation’s very large crude carrier Al Salmi was targeted by a swarm of drones believed to be Iranian on Tuesday morning, causing damage to the vessel and sparking a fire onboard the tanker that is fully laden with 280,000 tonnes of crude.

– Brazil’s state oil firm Petrobras (NYSE BR) has reported another discovery in the offshore Campos basin, next to the already producing Marlim field, finding crude of ‘excellent quality’ at a water depth of 1,178 metres.

BR) has reported another discovery in the offshore Campos basin, next to the already producing Marlim field, finding crude of ‘excellent quality’ at a water depth of 1,178 metres.

– Portugal’s oil major Galp (ELI:GALP) reported a ‘significant’ upgrade to its resource estimate for the giant Mopane discovery offshore Namibia, from 0.875 billion boe to 1.38 billion boe.

– US oil major Chevron (NYSE:CVX) said that its Wheatstone gas liquefaction facility will likely need a ‘number of weeks’ to return to full production rates after Tropical Cyclone Narelle damaged equipment both onshore and offshore.

Tuesday, March 31, 2026

Oil prices are set to log the highest monthly gain ever after the global economy experienced its worst-ever oil and gas supply disruption globally. With the Strait of Hormuz now officially closed and Tehran adding insult to injury by striking a Kuwaiti tanker in UAE waters, ICE Brent will roll over into April at almost $120 per barrel. In doing so, prices brushed aside US President Trump’s comments that the US might walk away from its so-called military operation without even opening the Hormuz.

Trump Floats Impending Kharg Island Attack. US President Donald Trump announced that he wanted to ‘take the oil in Iran’ and is mulling a potential seizure of the strategic Kharg Island, home to 90% of Iran’s oil exports, claiming that it would be ‘very easy’ as Tehran has no defense there.

G7 Expresses Readiness to Draw Down Oil. Finance ministers from G7 nations announced that they stand ready to take ‘all necessary measures’ to ensure energy market stability, implying there could be further SPR releases, and called on countries ‘to refrain from unjustified export restrictions’.

Israel’s Key Refinery Catches Fire. Israel’s 197,000 b/d Haifa refinery, the largest of the country’s two operational refineries covering some 60% of its needs, was hit by an Iranian missile attack that triggered a fire in the plant’s refined product storage tanks farm, delaying its restart.

Golden Pass Produces Its First LNG. Golden Pass LNG, a joint venture of QatarEnergy (70%) and ExxonMobil (30%), has produced its first liquefied natural gas this week, bringing the 18 mtpa capacity plant in Sabine Pass one step closer to full commissioning, expected later in April.

Russia Delivers Oil Cargo to Embattled Cuba. Russian authorities announced that the Anatoly Kolodkin tanker delivered 100,000 metric tonnes of crude to Cuba’s Matanzas fuel terminal, only the second ship to discharge in the Caribbean island in 2026 to date due to Trump’s political pressure.

Saudi Aramco Re-Routes Everything It Can. Saudi Arabia’s exports from the Red Sea port of Yanbu surged to a new record of 4.6 million b/d last week after the country’s state oil firm Saudi Aramco announced that the 7 million b/d East-West pipeline was finally pumping at full capacity.

South Korea Mulls Nationwide Driving Curbs. South Korea is considering extendingdriving curbs to the general public if global oil prices climb to $120-130 per barrel, the first nationwide restrictions since the 1991 Gulf War, having already launched a plate rotation system for the public sector.

Nigeria’s Key Refinery Turns to Domestic Oil. Nigeria’s national oil company NNPC will be allocating seven crude cargoes from the country’s domestic production to the 650,000 b/d Dangote refinery, up from the 5 it was receiving in earlier months, as soaring freight costs make imports costlier.

Drone Strikes Strangle Russian Exports. Ukraine’s drone strikes drastically curbedRussia’s oil exports after both Baltic Sea ports of Ust-Luga and Primorsk were hit past week, with weekly crude flows slumping to 2.32 million b/d, down 1 million b/d compared to the March average.

Chile’s Mining Woes to Lift Copper. Lingering copper prices could see some pricing upside after Chile posted its lowest monthly copper production in almost 9 years in February, with output totaling 378,554 tonnes and down 5% from a year ago as key mines continue to underperform.

California’s Offshore Riches Flow Again. US independent producer Sable Offshore (NYSE:SOC) has started selling some 50,000 b/d of crude from its restarted Santa Ynez pipeline system offshore California, filling up the pipe after an 11-year hiatus triggered by a major 2015 oil spill.

Key US Player Returns to Libya. US oil major Chevron (NYSE:CVX) has signed a deal with Libya’s National Oil Corporation to appraise and drill a ‘promising’ offshore oil block, a month after Tripoli announced the results of its first licensing round in 18 years, locking in block NC146 via direct talks.

Canada Fights to Keep Key Smelter. The governments of Canada and Quebec are close to an agreement with global mining giant Glencore (LON:GLEN) to keep the country’s only operational copper smelter online, suggesting a closure could be avoided for the 0.8 mtpa Horne Smelter.

US Exempts Offshore Drillers. A federal panel that included Interior Secretary Doug Burgum and EPA administrator Lee Zeldin voted unanimously to exempt oil and gas drillers operating in the Gulf of Mexico from a decades-old law to protect endangered species, citing potential environmental lawsuits.

- A lack of sellers changes everything.

- The data says stocks are not falling apart.

- The math says the next move is more buying.

Because if you’re just following the headlines, they’ll tell you things are breaking down everywhere. Bear market. Risk off. Get defensive.

But when you actually look under the hood, it’s a different story.

New lows on the New York Stock Exchange (NYSE) aren’t expanding. They’re shrinking.

Each week, fewer stocks are participating in the downside, even as the indexes themselves flirt with fresh lows.

That’s not what real deterioration looks

If stocks are “breaking down,” where are the sellers?

One possible answer is that they’re already gone.

Investors have spent weeks, maybe months, preparing for chaos. They’ve hedged, de-risked, raised cash, and in many cases already sold what they wanted to sell.

If that’s true, then what we’re left with is a market where the pressure isn’t coming from new sellers.

It’s coming from a lack of them.

And that changes everything.

Who’s Left To Sell?

Charlie McElligott of Nomura said it best this week: “Stocks refuse to crash because we’re too hedged for chaos.”

That’s not a throwaway line. That’s positioning.

Commodity trading advisor (CTA) trend followers have been dumping risk aggressively.

Goldman Sachs estimates they sold about $190 billion in equities this month and are now net short roughly $50 billion globally:

This isn’t discretionary selling. These are systematic players doing exactly what they’re programmed to do as trends weaken.

But here’s the part that matters.

When this group gets this short, historically it hasn’t marked the start of sustained downside. It’s been much closer to the end of it.

Because once they’re short, the next move is buying.

Goldman’s Brian Garrett is already pointing in that direction. His team expects CTAs to be buyers over the next month in basically any scenario.

Think about what that means.

If the marginal seller has already sold, and is now mechanically turning into a buyer, the pressure flips.

If that shift is already starting, it would help explain what we’re seeing beneath the surface.

Stocks that refuse to go down.

The Tape Isn’t Confirming It

The indexes made new lows yesterday. The S&P 500 did it. The Nasdaq-100 did it. Even some of the recent leaders finally saw a little pressure.

That’s what the headlines focused on.

But underneath the surface, the data told a completely different story.

Fewer stocks on the NYSE hit new 52-week lows than last week. And last week had fewer than the week before.

That’s the opposite of what you see in real breakdowns. You want expansion in new lows. We’re getting contraction.

Now look at participation.

The percentage of stocks above their 200-day moving average rose. Same thing for the 50-day. Even shorter term, the percentage above the 20-day surged and is nowhere near the washed-out levels from just two weeks ago.

So while indexes are probing lower, more stocks are actually holding up or improving.

That’s not distribution. That’s absorption.

Then there’s breadth.

The cumulative advance-decline lines for both the NYSE and the S&P 500 actually moved higher. Not by much. But they didn’t fall. On a day when indexes made new lows.

Think about that for a second.

If you want a group to watch, look at financials.

We don’t get sustained bull markets without them, and they were up over 1% yesterday.

Right off support at that 61.8% retracement from last year’s rally:

When financials are rising while the indexes are making new lows, I pay attention.

When everyone is telling you stocks are falling apart, and the data says otherwise, I pay even closer attention.

Because if everyone is positioned for chaos, and the market still can’t go down, that’s not weakness.

That’s something else.

So is the market actually too hedged for chaos?

The math checks out.

jog on

duc

Source link