MHJ – Michael Hill International

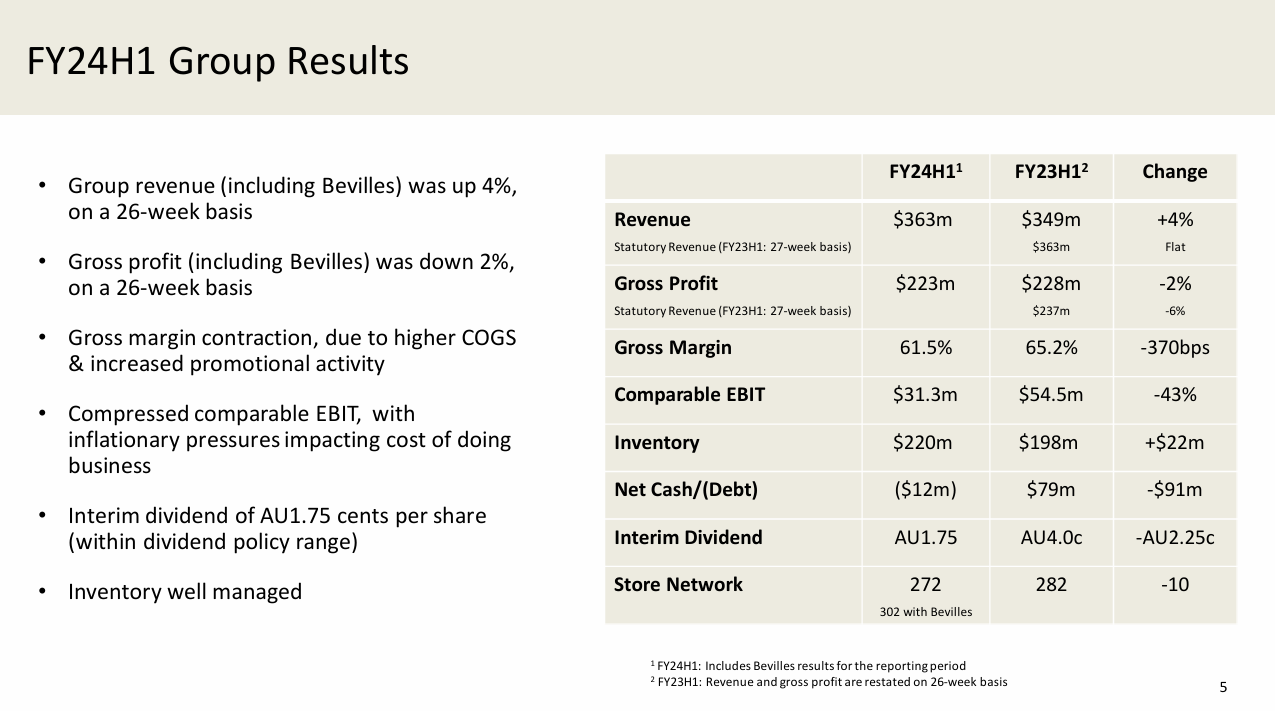

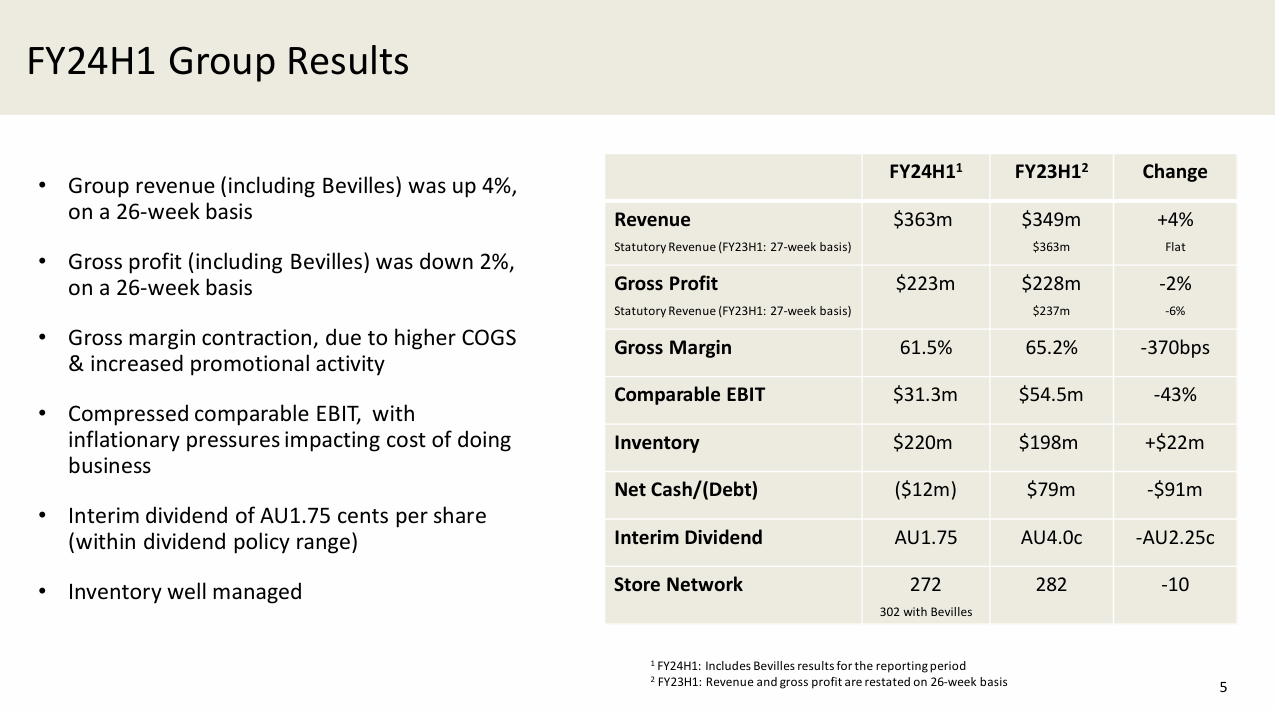

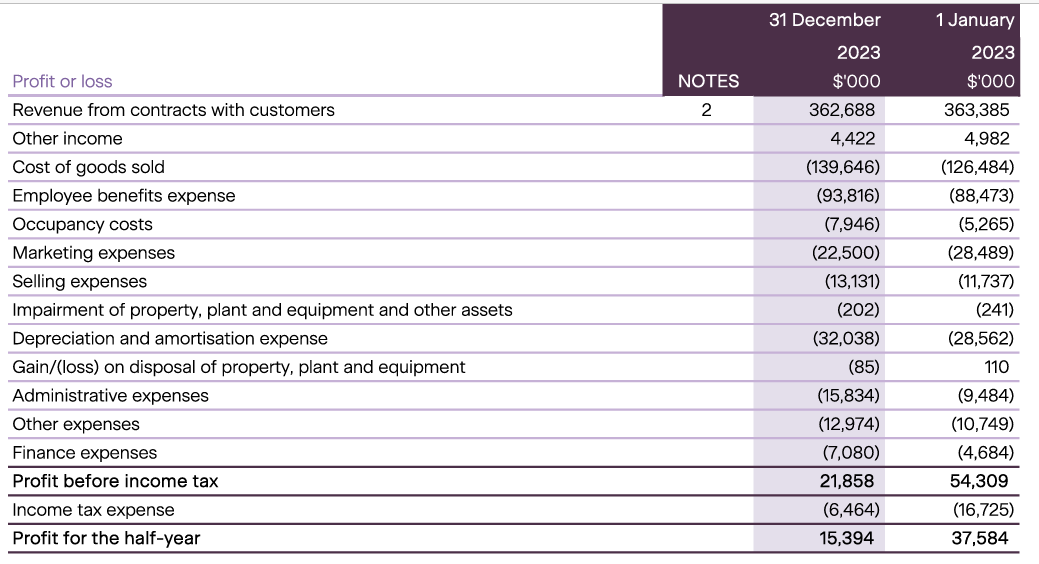

“Comparable EBIT” is another junk term made up to avoid showing a more significant fall in profits. The cashflow statement does not look very healthy. Operating cashflow for the half ($22m) didn’t even cover leases ($24m), which leaves them dependent on borrowing to pay for capex (13m) all the while paying a dividend which they also cannot afford. IN FY23, operating cashflow was 80m – capex was 25m, leases were 45m, buybacks were 10m – and they still paid a dividend.

They bought Bevilles (another Jewler) last year and traded cash for intangibles… I anticipate the usual ASX takeover post 1 year write-off in several months. I personally can’t see where bevilles or michael hill have genuine name/brand recognition either. They’re not Tiffany – your wife doesn’t say I want a Michael Hill necklace.

Anyways, back on the watch list but I’m not holding out much short-term hope for a price increase.

Source link