What is Quantifying Risk: Part I- Using Delta

When analyzing the risk of our covered call writing or cash-secured put trades, we typically are referring to the exposure of losing capital. However, there is also the risk of exercise, which we may want to avoid. In the case of calls, it is the potential sales of our shares; and in the case of puts, it’s the possibility of having to purchase shares. In this article, Delta will be highlighted as one of the ways to measure or quantify these liabilities.

What is Delta?

Delta has multiple definitions. The one that applies to estimating the risk of our trades is as follows: The approximate probability of the option expiring in-the-money or with intrinsic-value.

Covered call risk example

We may not want our shares sold. We would then select an out-of-the-money strike based on the amount of risk we are willing to incur. This will vary from investor-to-investor. We also want to be sure that the premium returns align with our pre-stated initial time-value return goal range. Since mitigating risk comes at a cost, we would anticipate lower returns than traditional option selling.

Cash-secured put risk example

We may not want to purchase the underlying shares. We would then select an out-of-the-money strike based on the amount of risk we are willing to incur. This will also vary from investor-to-investor. We also want to be sure that the premium returns align with our pre-stated initial time-value return goal range. Since mitigating risk comes at a cost, we would anticipate lower returns than traditional option selling.

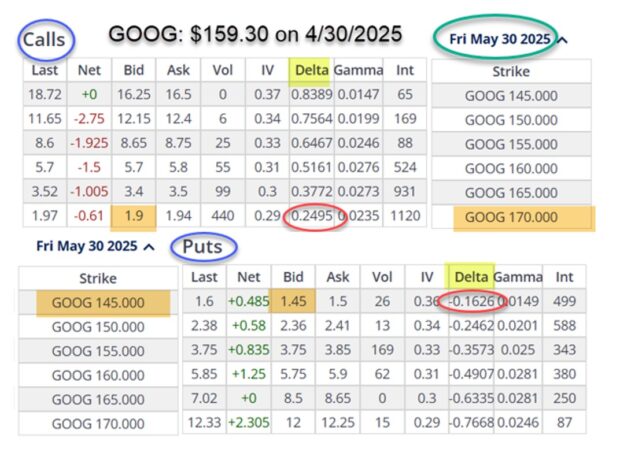

Real-life example with Alphabet, Inc. (Nasdaq: GOOG): Option-Chain on 4/30/2025

- The $170.00 OTM covered call strike shows a Delta of 0.2495 or 25%. This is the risk of expiring ITM and subject to exercise

- If we wanted to expose ourselves to more or less risk, we would select strikes accordingly

- The bid price of this $170.00 call is $1.90/share

- The $145.00 cash-secured put strike displays a Delta of -0.1626 or 16%. This is the risk of expiring ITM and subject to exercise

- If we wanted to expose ourselves to more or less risk, we would select strikes accordingly

- The bid price of this $145.00 put is $1.45

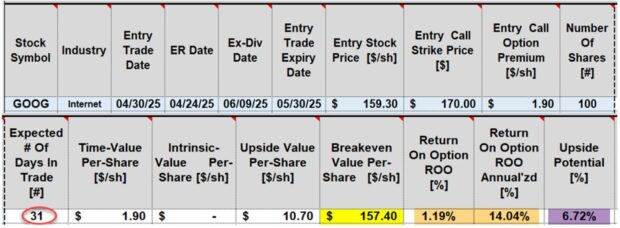

GOOG: Covered call calculations: The BCI Trade Management Calculator (TMC)

- Red circle: This is a 31-day trade, if taken through contract expiration

- Yellow cell: The breakeven price is $157.40

- Brown cells: The 31-day return is 1.19%, 14.04% annualized

- The upside potential is 6.72%, for a max 31-day potential return of 7.91%

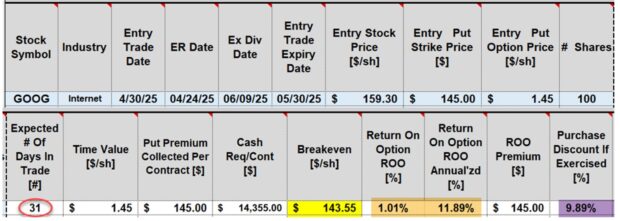

GOOG: Cash-secured put calculations: The BCI Trade Management Calculator (TMC)

- Red circle: This is a 31-day trade, if taken through contract expiration

- Yellow cell: The breakeven price is $143.55

- Brown cells: The 31-day return is 1.01%, 11.89% annualized

- The purchase discount if exercised is 9.89%

Discussion

The approximate amount of risk we are subject to in our option-selling trades can be quantified using Delta. The greater the risk that aligns with our personal risk tolerance, the higher will be our initial time-value returns and vice-versa. Despite taking defensive postures to our trades, the returns can still be significant.

***In an upcoming article, another methodology of quantifying risk will be analyzed.

Selling Cash-Secured Puts Basic and Advanced Principles: Online Video Course

Selling Cash-Secured Puts is a 6-part Video Series + downloadable workbook. All aspects of Put-Selling including stock selection, option selection and position management. A huge section on exit strategies and a deeper dive into ultra-low risk approaches to selling cash-secured puts have been added to previous versions of this course. The Companion Workbook contains 111 all-color pages of all charts, graphs and slides. Download Table of Contents (PDF)

This course contains 6- parts in the video course:

Section I: Option basics (definitions and foundational information)

Section II: Traditional put-selling (stock & option selection + position management)

Section III: PCP (wheel) strategy (adding covered calls to selling cash-secured puts)

Section IV: Buy a stock at a discount instead of a limit order (buy a stock at our target price or get paid not to buy the stock)

Section V: Ultra-low-risk put/Delta strategy (High probability, low-risk trades)

Section VI: Ultra-low-risk put/implied volatility strategy (High probability, low-risk trades)

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to publish several of these testimonials in our blog articles. We will never use a last name unless given permission:

Alan,

Thank you for this insight on explaining the TMC!

Its hard not to be excited with the BCI system even after learning from you for many years now.

The initial value of our retirement packages has more than doubled by using BCI methods.

I appreciate what you have done and always look forward to new learning experiences with BCI.

Jim

Upcoming events

1.Mad Hedge Investor Summit

Tuesday September 9, 2025

11 AM ET

Details to follow.

2. BCI Educational Series Webinar # 8: New Credit Spread Calculator

Thursday September 18,2025

8 PM ET – 9:30 PM ET

Over the past 2 years, BCI has been developing and beta-testing a 1-of-a-kind spreadsheet for entering and adjusting our credit spread trades. Like our Trade Management Calculator (TMC), our goal was to make it the industry standard. Only you can decide if we accomplished our mission.

Alan & Barry will introduce this product, review all the tabs inherent in the spreadsheet and demonstrate how to use it. A 1-time early order discount will also be offered.

For those who trade, or are interested in learning how to trade, credit spreads, this is a must-see webinar.

Click here to register for free.

3. Orlando Money Show

Orlando Resort @ ChampionsGate

October 16 – 18, 2025

- Opening ceremony keynote address

- 45-minute workshop class: Traditional & Low-Risk Covered Call & Cash-Secured Put Trades

Details and registration link to follow.

4. Money Masters Symposium Sarasota Florida

December 1 – 3,2025

Setting Up Option Portfolios Using Stock Selection, Diversification, Cash Allocation and Calculations

Analysis of 6 covered call writing trades

Minimize risk and maximize returns. These are our 2 main goals when crafting our option portfolios. There are several factors we can utilize which will put ourselves in an outstanding position to achieve these objectives. Here is a summary of those factors which will be addressed during this presentation:

- Select elite-performing stocks and ETFs

- Diversity stock positions as well as their industries

- Allocate a similar amount of cash per-position

- Ensure that initial calculations align with strategy goals and personal risk-tolerance

- Once trades are entered, go into position management mode- be prepared for exit strategy opportunities

Registration link to follow.

Source link