Part III: Deglobalisation – Your Investment Framework – Fat Tail Daily

From Kyiv to Gaza.

The Taiwan Strait to the Strait of Hormuz.

Our third and most prosperous globalisation event is deteriorating rapidly.

That’s what I explained in your last edition here.

So, how did we get here?

Well, weak global leadership and ineffective diplomacy are certainly fast-tracking the end of our third and most prolific globalisation wave over the last 150 years.

And while this promises to be an incredibly challenging investment phase, it’s not all bad, especially for commodity-focused investors!

Let me explain…

No doubt, you’ve seen the AI-capex buildout and green energy transition.

This has been hyped as the key catalyst to drive commodities higher over the years ahead.

Sure, it will be an important factor. But as I’ve maintained many times before, I don’t believe this will be the PRIMARY catalyst.

Instead, it could be this:

The retreat of globalisation

I believe that this could emerge as the single most important driver of higher commodity prices in the years to come.

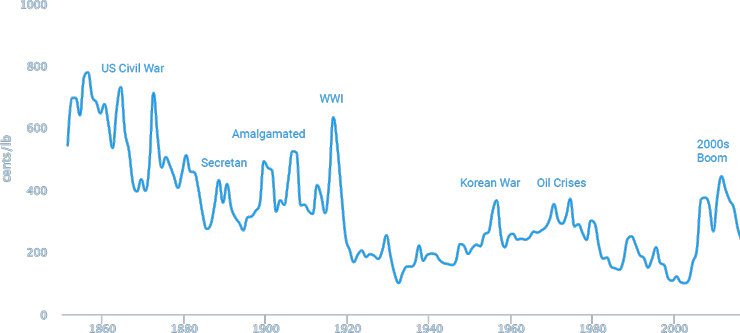

Recall the 1970s, a period of deglobalisation that witnessed record prices for copper, nickel, coal, oil, and uranium, among others.

But it was 1914, and the capitulation of the first major globalisation event that delivered one of history’s greatest-ever commodity surges.

According to data published by the United States Department of Labour, copper traded for almost $14,000/tonne (in real terms) way back in 1914.

That’s amongst the highest levels ever recorded for this market.

But it’s not so much de-globalisation as the cause of higher commodity prices… it’s the events leading to the demise of global trade that help foster the surge.

One aspect: demand driven by hostility

Whether the conflict is active (or cold), the outcome is the same.

As the drums of war beat louder, nations spend more on metal-intensive rearmament.

History shows that this is the biggest driver for higher commodity prices, especially critical metals like copper:

Source: USGS

[Click to open in a new window]

It’s why I have long held that ‘Dr Copper’ is a misused barometer of global growth.

History shows that its primary connection lies in global rearmament and its allocation to defence spending and all that it entails.

In my mind, it’s a more valid explanation for today’s surging copper price…

De-globalisation, the reshoring of manufacturing, and a return to self-sufficiency are already underway…

And that’s moving in lock step with a copper price that’s now HIGHER than the early 2000s ‘once-in-a-generation’ commodity boom.

Right now, we’re witnessing the most important historical demand driver for metals and energy.

The historical link that virtually no one is paying attention to.

But here’s the important part…

As demonstrated by past cycles, when the point of no return is reached, commodities pivot AWAY from rational pricing mechanisms.

Where supply chain security matters MORE than economic efficiencies.

Again, that’s starting to unfold, but we haven’t seen the consequences yet.

In my mind, the events taking place today mirror much of what has taken place in the past… Re-inflation, deglobalisation and rising conflict.

These are the things that explain today’s surging commodity prices.

From now on, the solution is clear:

Unhinge yourself from the geopolitical risk that could soon hit most asset classes and build your exposure to commodities.

Next time, we’ll outline specific strategies.

Until then.