April micro-cap flashback – Fat Tail Daily

About two months ago, micro-caps were having a torrid time.

The recent budget may perversely help them this month despite its clear hostility to risk capital.

In times like these, it can be hard to navigate the waters in this end of the market if you don’t fully understand risks.

So given today is a public holiday in Victoria, below is an example of some of the content that was published in Fat Tail Micro-Caps in April.

The dichotomy between larger ASX stocks and micro-caps is often stark, and I shared with readers how I would be looking at recommendations for commodities stocks in light of changing capital conditions in the market.

But as the saying goes – the worm must turn.

Here’s hoping the second half of the year improves for this end of the market, and the quality companies in the micro-cap space can get some more big wins on the board.

You’ll hear from me tomorrow, when I’m back at the desk – enjoy the break!

The risks weighing on markets right now

(Fat Tail Micro-Caps, Excerpt 15 April, 2026)

Let’s be direct.

The war with Iran is hurting micro-caps.

And it has introduced a layer of geopolitical risk that the market is still struggling to price.

High oil prices feed directly into transport and logistics costs, and anything diesel-adjacent.

Everything we buy, in effect.

Compounding this is the private credit complex.

Years of cheap money pushed enormous capital into illiquid, leveraged structures that are now being stress-tested at the worst possible moment.

Any disorderly unwind of private credit that doesn’t stay contained could be seismic.

Put those two forces together and you get a genuine inflation scenario: energy-driven cost push, tighter credit conditions, and a market that is already jittery.

Now, here’s the part I want to dwell on for a moment, because it’s important.

If that inflation scenario plays out, the economic system has a mechanism for dealing with it.

Higher commodity prices act as a price signal that forces capital, the institutional funds, infrastructure investors, sovereign wealth…to deploy into quality projects that increase supply.

That capex cycle is not optional.

It’s how the world keeps the lights on, the machines running, and the data centres humming.

That means quality companies with genuine projects, strong capital structures, and credible management teams SHOULD attract funding.

Not all micro-caps, but the right ones.

Yes, there may be short-term suffering.

This is why we have stop-losses.

But if we position wisely in companies that sit directly in the path of that forced capital allocation, we can ride out the volatility and benefit enormously when the tide turns.

That’s the plan in place.

The micro-cap malaise —

even the pros are feeling it

Micro-caps as an asset class have been suffering.

It’s not your imagination, and it’s not just our portfolio.

Across the market, we’re seeing a pronounced rotation away from the small and micro end of the spectrum as investors look to de-risk and park capital in large-cap defensives.

The BHPs, the Woodsides, even the banks.

In a world of uncertainty, big and liquid stocks are the market’s preference.

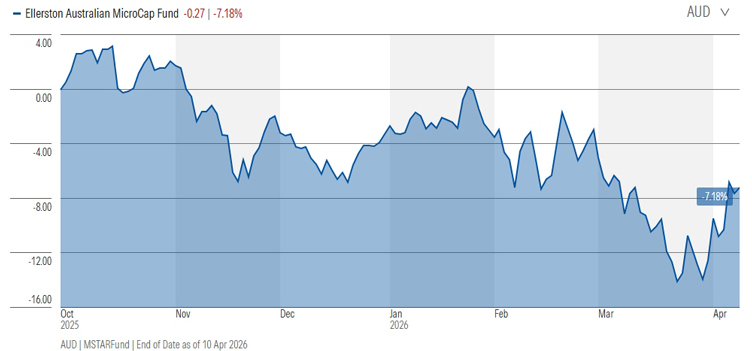

So, I want to show you something.

Below is the performance chart of the Ellerston Australian MicroCap Fund which is one of the most respected dedicated micro-cap funds in the country, run by a team of professionals with significant resources and experience:

Source: Morningstar

[Click to open in a new window]

Down approximately ~7% from October 2025 through to April 2026.

Ellerston ain’t amateurs.

Ellerston Capital runs a ~60 stock portfolio of Australian micro-caps with a big team behind it.

And they’ve been through the wringer the last 6 months right alongside the rest of us.

When even the best-resourced specialist funds in this space are posting losses across a six-month stretch, it tells you that this a micro-cap wide phenomenon.

The entire asset class is getting hurt as capital flees to safety.

This is the mood I’m getting from conversations across the industry: face to face at conferences, on the phone with brokers and fund managers.

We’re not at the bottom of the sentiment cycle yet.

But also, bottoms form when nobody is looking.