Upslope Capital’s Q3 2024 Investor Letter

Pornpimone Audkamkong/iStock via Getty Images

Dear Fellow Investor,

Upslope’s objective is to deliver attractive, equity-like returns with significantly reduced market risk and low correlation versus traditional equity strategies. Last quarter, I noted headwinds for Upslope’s regular style biases (overweight defensives, midcaps, Europe, and value). Q3 was the opposite: a near ideal environment for Upslope’s style, and performance reflected this.

Upslope Exposure & Returns[1] | Benchmark Returns | |||

Average Net Long[2] | Net Return | S&P Midcap 400 ETF (MDY) | HFRX Equity Hedge Index | |

Q3 2024 | 34% | +14.8% | +6.8% | +2.3% |

YTD 2024 | 39% | +18.1% | +13.2% | +7.5% |

Last 12 Months | 43% | +36.7% | +26.3% | +11.4% |

Since Inception | 34% | +11.5% | +10.3% | +4.9% |

Downside Deviation | 5.0% | 13.0% | 4.8% | |

Sortino Ratio[3] | 1.91 | 0.64 | 0.60 | |

| Note: LPs/clients should always check individual statements for returns, which may vary due to timing, fee schedules and other factors. Since inception returns, downside standard deviation, and Sortino are all annualized figures. |

MARKET CONDITIONS – WALL STREET CYNIC4

Market participants are as cynical as I have seen in my career. Likely frauds are popular trading vehicles – even among respected, big name fund managers. All potential risks are buying opportunities (actual drawdowns optional). This has been the correct mindset for a while, but the windows and buyable drawdowns are getting smaller and shallower, even as some risks look increasingly serious. Today, markets are very expensive, geopolitical issues are bubbling, and macro uncertainty is high. Despite this, investors seem to widely anticipate post-election relief in the form of falling volatility (usually associated with rising equity indexes). While I am open-minded, as always, markets feel unusually imbalanced and I’m not sure it’s that easy.

The Fund added several new longs – CME Group (CME), CompoSecure (CMPO), and Mitsubishi Heavy Industries (OTCPK:MHVYF) – most significantly during the early August swoon. The Fund exited Finning (OTCPK:FINGF) and cut back Garmin (GRMN) and Kongsberg (OTCPK:NSKFF). Despite markets sitting near all-time highs, I still see pockets of value on the long side. Naturally, there appear to be ample opportunities for shorts.

PORTFOLIO POSITIONING

At quarter-end, gross and beta-adjusted net exposures were 151% and 44%, respectively. Positioning continues to reflect a high number of perceived opportunities on both sides of the portfolio.

Exhibit 1: Portfolio Snapshot

NAME | TICKER | INDUSTRY | HQ | MCAP ($B) |

Core Longs (26% of Total Gross Exposure) | ||||

CME Group Inc. | Investment Banks/Brokers | United States | $79.3 | |

Hershey Company | Food: Specialty/Candy | United States | 38.8 | |

DSM-Firmenich AG | OTC:KDSKF | Chemicals: Specialty | Switzerland | 36.6 |

Japan Exchange Group, Inc. | Investment Banks/Brokers | Japan | 13.5 | |

AptarGroup, Inc. | Containers/Packaging | United States | 10.6 | |

Diploma PLC | Wholesale Distributors | United Kingdom | 8.0 | |

Tactical Longs (34%) | ||||

Mitsubishi Heavy Industries, Ltd. | Aerospace & Defense | Japan | $49.8 | |

Teledyne Technologies Inc. | Aerospace & Defense | United States | 20.5 | |

nVent Electric plc | Electronic Components | United States | 11.7 | |

Barry Callebaut AG | Food: Specialty/Candy | Switzerland | 10.2 | |

Winpak Ltd. | Containers/Packaging | Canada | 2.2 | |

CompoSecure, Inc. | Commercial Printing/Forms | United States | 2.2 | |

North West Company Inc. | Specialty Stores | Canada | 1.8 | |

Chemring Group PLC | Aerospace & Defense | United Kingdom | 1.3 | |

Starter Longs (19%) | ||||

Garmin Ltd. | Telecommunications Equipment | United States | $33.8 | |

Undisclosed | — | Major Banks | Norway | 30.6 |

Undisclosed | — | Aerospace & Defense | United States | 30.2 |

Kongsberg Gruppen ASA | Aerospace & Defense | Norway | 17.2 | |

Undisclosed | — | Miscellaneous Commercial Services | United States | 10.2 |

Undisclosed | — | Apparel/Footwear | United States | 7.8 |

Undisclosed | — | Beverages: Non-Alcoholic | United States | 7.3 |

Undisclosed | — | Air Freight/Couriers | Netherlands | 3.1 |

Shorts (21%) |

| Note: as of 9/30/24 and may change without notice. Positions disclosed/categorized at Upslope’s discretion. Source: Upslope, FactSet |

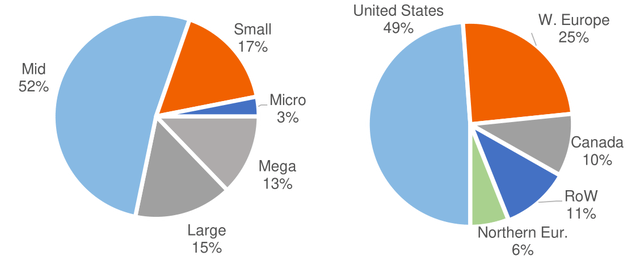

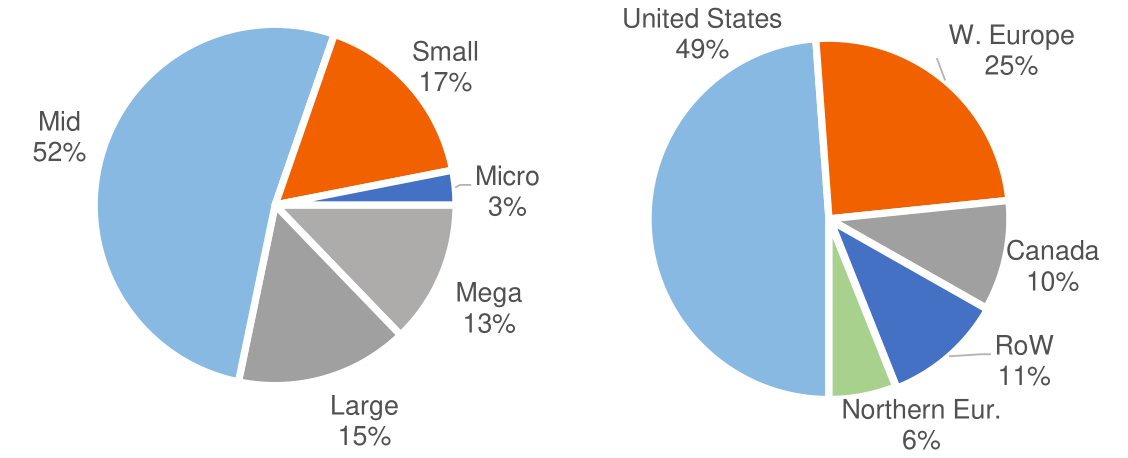

Exhibit 2: Gross Exposure by Market Cap & Geography (Total Portfolio)

| Note: as of 9/30/24. Market cap ranges: Micro ($50bn). Source: Upslope, Interactive Brokers, FactSet |

PORTFOLIO UPDATES

The largest contributors to and detractors from quarterly performance are noted below. Gross contribution to overall portfolio return is noted in parentheses.

Exhibit 3: Top Contributors to Quarterly Performance (Gross)

Top Contributors | Top Detractors |

Long/Short: VIX Hedge (+275 bps) | Short: Global Exchange (-105 bps) |

Long: Mitsubishi Heavy (+200 bps) | Short: China Hedges (-125 bps) |

Long: Undisclosed (+190 bps)5 | Long: Undisclosed (-85 bps)6 |

Longs – Total Contribution | Shorts – Total Contribution |

+2,070 bps | -260 bps |

| Source: Upslope, Opus Fund Services, Interactive Brokers Note: Amounts may not tie with aggregate performance figures due to rounding. |

Exited & Reduced Longs – Finning, Garmin, Kongsberg

The Fund exited Finning (FTT-TSE, world’s largest Caterpillar equipment dealer and distributor), largely on peak cycle concerns. While I believe margin peaks/troughs should continue to move higher over time, it’s hard to identify specific reasons for further improvement in the medium term.

The Fund also significantly reduced its positions in Garmin (GRMN, technology business known for smartwatches and navigation systems, among other products) and Kongsberg (KOG-OSL, Norway-based aero/defense and maritime business), due to full valuations. Both are very well-managed leaders in their respective niches. However, a significant amount of good news is clearly baked into shares today.

CME Group (CME) – New Long

CME Group is a leading operator of global derivatives exchanges. Key end markets include interest rates (34% of transaction/clearing fees in 2023), energy + other commodities (31% combined), equities (23%), and FX (4%). Upslope’s thesis is simple: CME is an attractive business that has been relatively out of favor vs. peers due to exaggerated worries about new competition and the end of the interest rate hiking cycle.

The financial exchange sector is comprised of durable, monopoly-like businesses, and has a history of predictable mean-reversion. Exchange stocks come in and out of favor, as investors extrapolate short-term issues and opportunities (not unlike other sectors, but I see this space as more predictable than most). CME is the “out of favor” exchange today: shares have materially lagged peers over the past 1/3/5 years and are reasonably valued today. Over the past 10 years shares have rarely been cheaper on a forward earnings basis. This, despite CME being in a strong position to benefit from continued interest rate volatility and ever-expanding U.S. government debt issuance, as well as general commodity volatility.

What makes CME a high-quality business? Due to the unique nature of derivatives market structure, the company holds a monopoly-like position in many key products. This is reflected in CME’s ~70% EBITDA margins. Additionally, unlike most global exchanges, which have shifted significantly away from being trading volume-driven and towards data/other services, CME still derives most of its revenue (82% in 2023) from trading. While most investors prefer the new exchange model, I hold the opposite view: I prefer to own shares of a company that benefits when volatility surges – even if that makes it harder to predict/model in the short-term.

On the competitive front, investors have worried that CME’s core rates products could be pressured by new competition from BGC Group, who launched the FMX Futures Exchange in late September. With the benefit of very significant network effects (liquidity begets liquidity), legacy exchanges have historically been able to easily fend off competition from new entrants. This situation appears no different. And while it’s early days, FMX volumes and open interest have not impressed to date. BGC’s CEO also appears to have other priorities: he is co-chair of the Republican presidential candidate’s transition team.

Key risks include: heightened volatility and trading volumes may not be sustained, potential for FMX volumes to improve significantly, large scale M&A, and potential trade matching/execution errors.

CompoSecure (CMPO) – New Long

CompoSecure is the leading producer of premium metal credit cards, with almost 85% market share7 in the U.S. and a growing international presence. The company dominates this growing, niche market, and does so via defensible, long-term contracts. Fundamentally, CMPO has performed well despite being a de-SPAC (that also navigated a COVID era demand surge). FCFE has historically been strong – growing HSD% and typically converting at ~100% of adjusted EPS.

In early August, the company announced a financially and strategically transformative transaction (now closed): David Cote, a legendary capital allocator (ex-Honeywell, Vertiv) would invest $372mm via his family office entity. Financially, the transaction cleans up the capital/share structure and immediately boosts free cash flow by eliminating the old dual class share structure and associated tax payments. Strategically, Cote will assume the role of Executive Chairman and seems poised to streamline operations and leverage CMPO for acquisitions in complementary verticals (a playbook Cote has deep experience deploying).

Prior to the transaction, CMPO shares traded in the 7x EPS range due to the SPAC stigma, customer concentration risk (serious, but pushed out many years following recent renewals), and uncertainty regarding the terminal value of the physical card business. Upslope effectively purchased shares for 9x EPS shortly after the transaction was announced, with a simple thesis that the deal was very clearly transformative – eliminating or mitigating most of the prior perceived issues and creating significant optionality via Cote’s involvement. Shares have continued to re-rate, but at 12x EPS remain reasonable considering the tangible and intangible benefits of the transaction.

Key risks include: cyclical end markets (partially tied to credit card issuance volumes), uncertain strategic changes, M&A execution, “key man” risk (Cote), customer concentration, and potential for accelerated shift to digital/phone-based cards.

Mitsubishi Heavy Industries (7011-JP) – New Long

Mitsubishi Heavy is a Japanese industrial conglomerate with four broad segments: Energy Systems (38% of F2023 sales), Logistics & Thermal Drive Systems (28%), Aircraft, Defense and Space (17%), and Plants and Infrastructure Systems (17%). The company is a global leader in the design and production of gas turbines and nuclear power systems. It is also the largest domestic defense contractor in Japan – a nation committed to nearly doubling defense spending as a percent of GDP in short order. 8

This is an unusual situation and position. I had been tracking Mitsubishi Heavy for some time, and while the business and outlook looked attractive, shares were expensive. Then, in early August the Japanese market had its own “flash crash.” Mitsubishi Heavy shares dropped ~40% in short order and were suddenly cheap. Because of Upslope’s nimble structure (“investment committee of one”) and size, the Fund was able to move fast and purchase shares at a steep discount. The stock has rebounded surprisingly fast.

Upslope’s thesis is that Mitsubishi Heavy holds leading market positions in unique end markets – Japanese defense, nuclear power, and gas turbines – that should continue to see very strong (and in some cases accelerating) demand over the medium- and long-term. At 14x EBITDA shares are no longer “cheap,” as they were just a few weeks ago. But given the tailwinds noted above, I believe they shouldn’t be.

Key risks include: FX, cyclical end markets, political and geopolitical uncertainty (re: defense unit), potential for operational accidents/liability.

STRATEGY COMMENTARY

Two topics I’d like to discuss: (1) update on expansion of gross exposure implemented two years ago, and (2) comment on market cap movement of late.

- Gross exposure. Two years ago, I increased the strategy’s self-imposed limit on gross exposure from 125% to 150%. You can read the commentary here(under “Fine-tuning the Strategy”). To date, I believe the change has had a clear positive impact. As anticipated, volatility has increased moderately – but so too have absolute returns. Given downside volatility of the strategy had been extremely low (roughly 1/3 of long-only indexes), I believe the tradeoff was well worth it. Related: with higher gross exposure, you may have noticed a steady increase in the number of positions in the portfolio (mostly, but not entirely due to the addition of “Starters”). This has been a deliberate shift. While I wanted higher gross exposure, I did not want greater single position concentration risk. The success of this adjustment is harder to measure, but I also believe it has been for the better. In addition to enabling higher gross, having more positions also helps me be more patient. Sheepishly, I hadn’t anticipated this benefit. An example: in a portfolio with just 10 longs, just one laggard can be detrimental to medium-term performance. With a greater number of positions, a portfolio manager is afforded the ability to be more patient – not every single position must “work” at all times. Perfect timing becomes less important than getting the thesis right. Of course, there is no free lunch and this adjustment spreads me a little more thin. Overall, I think this is another tradeoff that is well worth it; however, I do anticipate pulling back from the current number of positions, which feels slightly too high (partly driven by tax management).

- Market cap changes. You may have noticed the Fund currently holds a higher than typical number of larger cap (> $25bn) stocks. Has there been a big change in strategy? In short, “no.” The long answer is more nuanced. First, the strategy remains centered on midcaps – Upslope holds positions in some companies larger than typical midcaps and some quite a bit smaller. At Q3-end, three of the Fund’s top four longs were below $10 billion market cap – two were sub-$2 billion. The median portfolio company was still very clearly midcap at $8 billion. That said, I do think some flexibility is prudent. It seems irrational to ignore opportunities that arise well within my circle of competence – CME being the obvious example – that happen to be outside of the technical “midcap” definition. Rest assured, I see that the portfolio looks a bit different than in the past and note every new position outside of the midcap strike zone. And while market caps of the Fund’s holdings may rise or fall over time, I assure you that I remain as committed as ever to constructing and maintaining an uncorrelated portfolio that looks like no one else’s.

CLOSING THOUGHTS

As always, thank you for the trust you’ve placed in me and Upslope to manage a portion of your hardearned money. If you have any questions at all, would like to add to your investment, or know a qualified investor who may be a good fit for Upslope’s unique approach, please call or email anytime.

Sincerely,

George K. Livadas

Source link