7 Bad Things That Can Happen Investing in SPVs – Churning and Burning

We’re living in exciting times right now. SpaceX is about to IPO on Friday and there’s a lot of chatter. I’d say about half the chatter is about the company being overvalued at 100x revenue, 25% of it is about having unlimited $10T type of upside, and the other 25% of the chatter is about the unraveling of the many, many SPVs–like the tweet below.

I’ve been reading a lot of fear mongering lately on VC/Tech Twitter about SPV investing. Here’s a small sample I have collected:

Yikes. If you’re looking at all of this from the outside, SPV investing probably sounds like an absolute minefield. Why not just stick with public markets, where disclosures are plentiful and you can hit the sell button whenever you want? Totally get it. Let’s break down all the bad shit that can happen when you invest in SPVs.

7 Bad Things That Can Happen Investing in SPVs

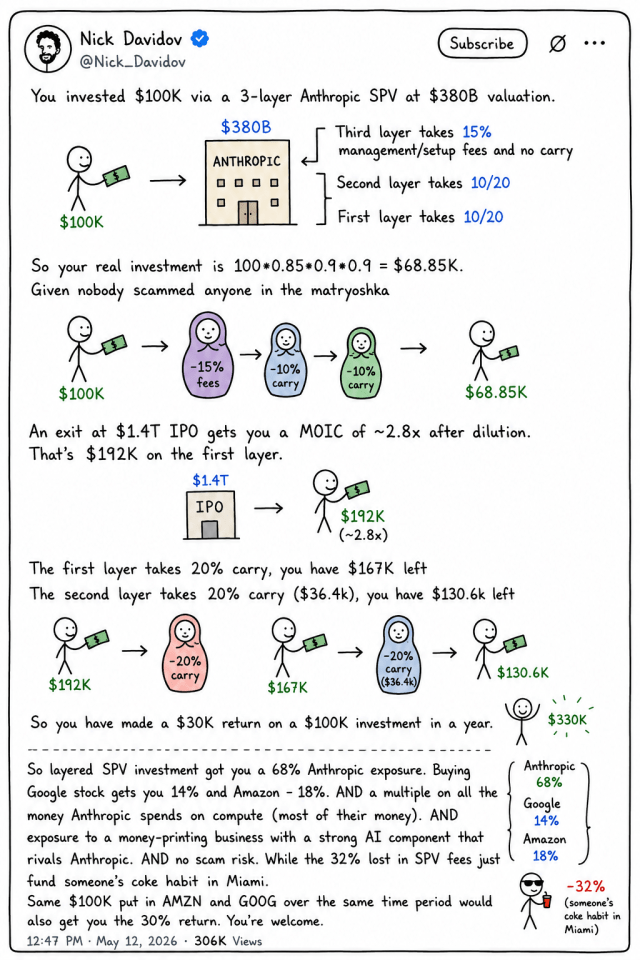

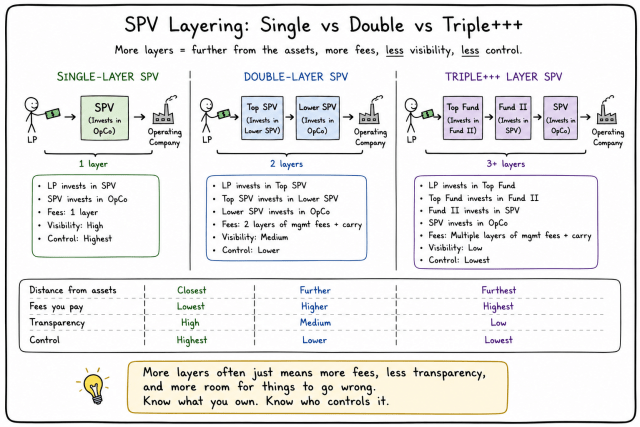

1. Multi-layered SPVs creating too many middlemen and massive fee drag

Notice there’s a lot of warnings about sitting in triple layer or quadruple layer SPVs.

Given how publicly I’ve written about private investing, how many platforms I’m on, and how many random deal pitches end up in my inbox, you’d think I’d be the perfect target for some absurd quadruple-layer structure where the fees compound into oblivion and nobody can explain who actually controls the shares. Yet I’ve never seen any of them.

Meanwhile, my Twitter and LinkedIn feeds are full of well-meaning VCs warning about these labyrinthine SPV structures lurking around every corner. It supposedly could be someone’s cousin in Miami funding his coke addiction. If these things are really everywhere, I’m apparently on the wrong mailing lists. Maybe they’re just in private SF group chats and I’m too far away from the action. Lucky me.

Maybe I’m just lucky to have the right relationships. Or lucky to have common sense and not get into triple layer SPVs where I’m paying triple carry because I know it is an obvious horrible deal.

But yeah, don’t as a rule, do not get into a triple layered SPV. Double is OK. Single is ideal.

2. Good ol’ fashioned FRAUD

Johnny B. Broker cold calls you and says he can you sell a block of Anthropic. Just my luck! But he doesn’t have the shares and he doesn’t even plan on trying to acquire them later–he simply pockets the money. Sorry, it’s just fraud.

It’s happening a lot now. Some of them have been charged and sentence to prison: Here. Here. Here. Be careful out there.

You have to know how do your own counterparty due diligence. The simplest thing to do is use FINRA’s brokercheck–see if your guy and his firm are registered investment advisors. If you want to be even more diligent, do a background check or hire a securities lawyer. Then verify that the underlying shares exist–ask for a live video or at least a screenshot. If you can’t rely on yourself to do proper diligence, then it will ultimately come down to trust–do you trust your broker to have your interests at heart and to do good work themselves?

One of my best brokers, Aurelius Investments, sent us a memo on a shady negiotiation they had with a party called Sesante Capital, who were selling interests in an Anduril SPV. Here’s a summary of the memo:

The diligence team was unable to independently verify that Sestante Capital actually owned the Anduril shares it claimed to hold. Concerns escalated when the manager refused to provide basic verification through Carta, offering explanations that appeared inconsistent with how Carta’s authentication system works. Additional checks with industry contacts suggested neither Sestante nor its affiliated vehicle appeared on Anduril’s cap table, raising questions about the true ownership structure. The team also became uncomfortable with the lack of transparency, including the late disclosure that the shares were allegedly held through another underlying SPV rather than directly. Operationally, the firm appeared understaffed, lacked dedicated accounting and fund administration support, and had no independent auditor or administrator overseeing the vehicle. Combined with sparse documentation, weak governance processes, and concerning background-check findings, the diligence team concluded the risks could not be adequately mitigated.

Last December, Sesante Capital was charged with fraud. Always good to have competent people you can trust. Good job fellas!

3. The company you so badly want to invest in simply VOIDS YOUR SHARES

About a month ago, Anthropic posted a negative memo about SPVs. They stated this:

Any sale or transfer of Anthropic stock, or any interest in Anthropic stock, that is not approved by its Board is void and will not be recognized on its books. It also specifically said it does not permit SPVs to acquire Anthropic stock.

Pretty harsh language there. The memo is much more aggressive than the usual private-company transfer restrictions. They’re practically trying to kill the entire gray market of retail and HNWI access to Anthropic shares through unauthorized SPVs. It sent some shockwaves in VC/tech circles, with many people thinking their SPV interest was now a donut.

How valid is it? Can companies simply declare SPVs null and void?

My personal view is that Anthropic is doing more signaling than litigating. The company is clearly trying to discourage the explosion of unauthorized SPVs, synthetic exposure products, and increasingly convoluted secondary-market structures. Whether it actually intends to spend years and millions of dollars pursuing every SPV investor, sponsor, and intermediary is a separate question. Don’t they have better things to do with their time and money? I think all existing (real) SPVs will simply settle post IPO and there will be nothing that Anthropic can do about it.

That being said… I would probably just avoid buying any further interests in Anthropic unless you can actually be on cap table and verify that the company is going to approve the transfer.

4. SPV manager goes rogue

This is an off-shot of the whole “layered SPV” problem from point number one. You don’t have total control over your investment, the SPV manager does. And sometimes he decides to be a jerk because he has the contractual right to do so. It’s not fraud but it’s annoying.

Here’s my experience: Aurelius Investments bought an interest into a Stripe SPV with for another firm investment, let’s called them Pirate Investments, about a year ago. They didn’t have a pre-existing relationship across other deals so it was purely transactional relationship. The manager of Pirate Investments had the right to liquidate all interests at a fair market value. There was no reason to think he would exercise this clause but it turns out he wanted to start a new fund–buy land or boats or something, I don’t know, it doesn’t matter. So he sold the entire fund’s interest in Stripe and returned all funds. We did end up getting an 18% net return on our investment. My broker called me to apologize and said it was a lesson learned on their part to not getting involved without 100% control on the shares.

I’d rather not have sold Stripe. I viewed it as a long-term portfolio holding. We got in at $90 billion, exited in the high 100s, and it’s now worth $166 billion according to PM Insights.

5. The company doesn’t approve your transfer

This happened to me when I tried to buy an interest in Groq. From my Groq/Cerebras post:

I attempted to secure some shares of Groq in the $7-8 billion range in November 2025. My SPV manager, who believed that Groq had 10x upside, had secured a spot to co-invest with an investor on the cap table through an option to add more as a follow-up. SPV manager and counterparty agreed on a deal but approval for the follow-on shares sat on the board for a couple weeks. Then boom–on Christmas Eve–Nvidia announced that they had acquired Groq. $20 billion price–3x the valuation of their last fundraising round. Our deal evaporated into the ether and the SPV manager promptly returned all of our money. Too bad–it could’ve been a nice quick win for yours truly.

If SPVs aren’t your thing, you can sometimes buy shares directly from existing shareholders through marketplaces like Hiive or EquityZen. The advantage is that you own the shares directly instead of sitting behind an SPV manager. The catch is that private companies usually control who can appear on their cap table, so the transfer often requires company approval and may be subject to right of first refusal (ROFR).

6. The Best IPO Window Closes

Sometimes the company is ready to go public, but management decides to wait for a better market. Sometimes they’re right. Sometimes they miss the best opportunity they’ll ever get. Either way, your capital stays locked up while the exit timeline keeps moving further into the future. I thought this would happen to me on my very first investment on ABNB when they kept delaying for years until travel collapsed during an unforseeable pandemic… but I got lucky.

The idea schematic behind pre-IPO investing is that follow the VC financing model of infinity upround into IPO. But it doesn’t always work that way. Some examples of recent unicorns that missed their best shot and stayed below water from their highest private round:

Instacart and Klarna are two cautionary tales of having bad timing and not being able to sustain enough momentum into an IPO.

If you were trading these companies on the NASDAQ, you could get out when the chart says to get out or when fundamental inflections tell you to get out. In an SPV? You’re at the mercy of management’s timing and decision making.

7. You’re in a shit market and you don’t know it

If I had gotten obsessed with SPV investing back in 2020-2022 instead of in 2024, things probably would have gone very differently. I would have plowed money into a bunch of ZIRP’d up garbage at peak valuations only for my money to get stuck forever or in a few cases, marked to absolute 0. There’s a decent chance I would have sworn off private investing entirely. I’d probably be telling everyone it was a scam, nursing my wounds, and definitely not writing about it with the same enthusiasm I do today.

Here’s some of the stuff offered by Meridian Investments from the ZIRP era: Flexport, Dataminr, Convoy, Cyberreason, Instacart, ThoughtSpot, Bowery Farming–followed by where they are now.

Imagine investing in all of that junk and then just 2 years later, the marketplace is flooded with generational names like OpenAI, Anthropic, and SpaceX? And you don’t have either the capital or the risk tolerance to participate? Ouch. Timing matters.

I guess in the end, this is less a risk idiosyncratic to SPV investing and more of a risk that can be generalized to all markets. Some market periods just suck and there’s nothing you can do about it.

In the end, SPV investing isn’t magic. It’s the same old formula: diligence, timing, patience, and a healthy dose of luck. I’m super grateful I just flat out did not care to be in this space during the wrong time. Now I’m concentrating my bets amid what I believe are the tailwinds of the greatest technological breakthrough since the invention of the internet. I just need to get lucky on this cycle and I’m good. And pray I don’t hit any counter party landmines.

Related

Source link