Revisiting the SpaceX Valuation: A Post-Prospectus Update!

The prospectus also lays bare the governance questions that will overhang the firm, with information that there will be two classes of shares- 6,932 million class A shares with one vote per share and 5,602 million class B shares with ten votes per share. The public offering will be class A shares, and with Elon Musk holding all of the class B shares, he will control more than 85% of the voting rights in the company. In summary, the prospectus is long and filled with distractions, but there is almost nothing in it that surprises me. SpaceX is a growing company that is money-losing and cash-burning, that will be a Elon Musk vehicle (with all the pluses and minuses that entails).

The Prospectus: Story update

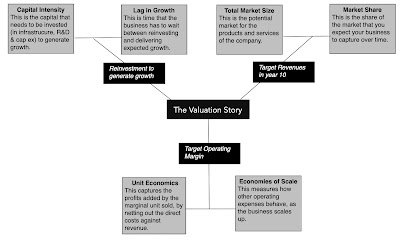

In my original post, I noted that SpaceX is a company, where it is the story about how its businesses will evolve over time that drives value, rather than the base year numbers (on revenues, earnings and cash flows). That story, broadly speaking, has three key spokes to it and they are summarized below:

The first of these spokes, target revenues, frame how big each business can grow over time, and is a function of the total market and market share. The second, the target operating margin, will capture how profitable each business can become, and is determined by unit economics and economies of scale. The third, reinvestment, measures how much each business has to invest to get to target revenues, and will vary with the capital intensity of the business. To frame how my valuation will change, as a result of what I learned from looking at the prospectus, I will start by presenting by pre-prospectus estimates on these key inputs, and then look at the impact of the prospectus on each input.

Pre-prospectus inputs and value

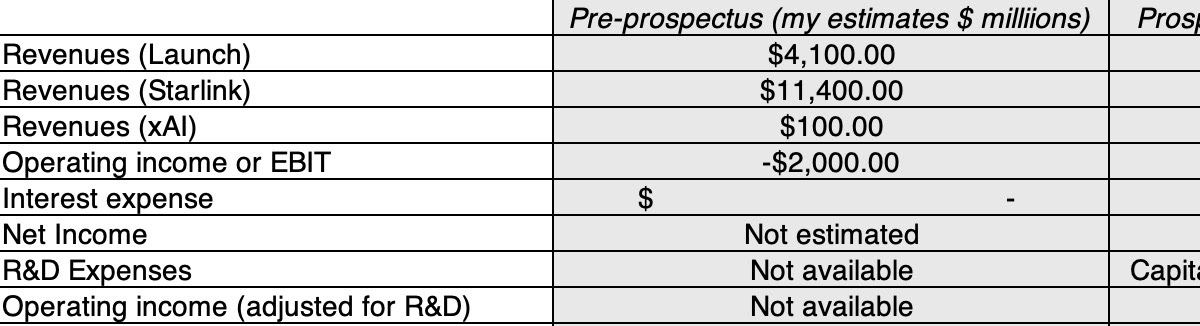

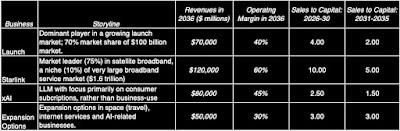

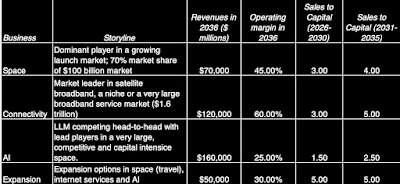

My pre-prospectus valuation of SpaceX contains my storyline for the three businesses that the company is in, with an add-on for the expansion options embedded in each business:

With these inputs in place, I estimated a value of $1.2 trillion the SpaceX enterprise, and since I ignored cash and debt, this yielded an equivalent market value. Driving these numbers are upbeat stories about each of the three businesses that SpaceX is in, with large revenues and high margins in stable growth.

The Prospectus Effect

To the extent that the prospectus contains information that alters the storylines on any or all of these businesses, it will affect my estimate of value for SpaceX.

1. Revenue Growth (Target Revenues)

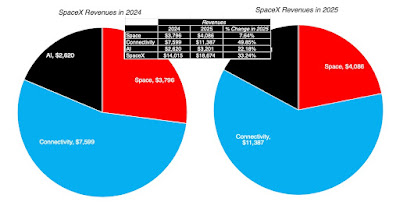

I will start with the growth (target revenues) input and use two parts of the prospectus to reexamine my story. The first is the historical growth reported by the company for each of its three business lines – launch, connectivity and AI.

As you can see, the company saw its revenues grow by a third in 2025, relative to 2024, with divergence across businesses; the connectivity business led with revenues growing by almost 50%, the AI business saw an increase in revenues of about 22% but the space business reported only modest growth in the year (7.64%). In short, notwithstanding the star role played by AI and the appeal of the rockets in the space launch business, it is Starlink that carried the company in 2025. The prospectus mentions Colossus, xAI’s compute center, which has been leased to Anthropic for an eye-popping $1.25 billion a month, which should kickstart revenues next year, with the potential of tension in future years if xAI plans to go head-to-head against Anthropic in the AI products market.

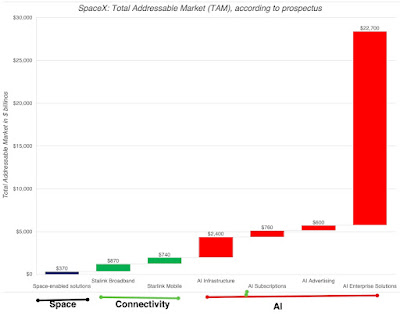

The other relevant section of the prospectus contained estimates of total addressable market (TAM) for the company, broken down by business:

Story takeaway: I will stick with my estimates for target markets for the space launch and connectivity businesses, since the TAMs in the prospectus are, in my view, over reaches, and I will slow growth in the near years, to reflect that these businesses will take time to mature. In the AI business, I disagree with the magnitude of the TAM in the prospectus, but the acquisition of Cursor and the indications in the prospectus suggest that xAI very much wants to be part of the enterprise solutions space, notwithstanding its immense capitalization needs, and I will double my target revenues for AI from $80 billion to $160 billion, reflecting my estimate of a TAM of about $3 trillion to $4 trillion for AI products and services from businesses.

- The space business has the best unit economics of the three business, with a gross margin of about 67%, reflecting the cost advantages of its reusable rocket technology. While the space business reported an operating loss, that was entirely because of its weighty R&D expenses, and capitalizing those expenses results in a healthy operating margin for the business.

- The connectivity business does not have gross margins as high as the space business, but those gross margins are improving, with gross margins jumping from 37% in 2024 to 48% in 2025. This business had positive operating income in 2025, even before capitalizing R&D, and improves substantially with capitalization.

- The AI business not only has the lowest gross margins of the three businesses, but saw deterioration of those margins in 2025, reflecting intense competition from other LLMs as well as the rising costs of delivering AI products and services.

There are other parts of the prospectus that come into play in the profitability discussion, with each of the businesses:

- On the space launch business, the cost of launching payloads at SpaceX have been trending down, making its already large cost advantages in the business even larger.

- On the connectivity businesses, there is bad news and good news on the per user front. The bad news is that the revenues, per month, per subscriber, declined from $99 in monthly revenues in 2024 to $66 in monthly revenues in the first quarter of 2026. The good news is that the number of subscribers has doubled from 5 million in the first quarter of 2025 to 10.3 million in the first quarter of 2026, with the bonus that the company has been able to improve its profitability (see gross margins in the table above) over time.

- On the AI business, there is not much to go on, on the profitability front, since the focus in the prospectus is more on the increase in compute capacity (see nameplate compute draw on Page 90 of the prospectus) than it is on revenues, especially on the enterprise front. Here again, though, the Colossus lease with Anthropic should help with profitability in the near term.

Story takeaway: The unit economics for the space businesses, in conjunction with the recognition that there are no other substantial operating expenses (outside of the misclassified R&D expense) in either business, lead me to increase my estimate of the target margin for the business to 45%, from 40%. I will leave intact the target margin of 60% for the connectivity business, because once the satellites that service this business are in space, this is the business that will benefit the most from scale. My biggest shift is in my estimated target margin is for the AI business, where the dynamics that are pushing gross margins down, i.e., increased competition and high costs of delivering AI services, will persist; my estimated operating margin drops from 45% to 25%.

3. Reinvestment

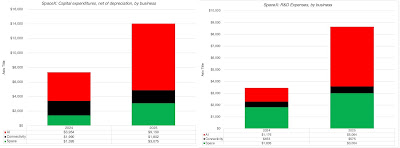

In my post prior to accessing the prospectus, I did describe SpaceX as a capital intensive business, but the actual spending on capital expenditures and R&D in the prospectus is breathtaking in its magnitude:

In 2025, the company spent almost $14 billion in capital expenditures and almost $9 billion in R&D, a doubling of its reinvestment from 2024. In particular, it is AI that is driving the bulk of this surge, accounting for more than $14 billion in total reinvestment in 2025, with $9.1 billion in capital expenditures and $5.1 billion in R&D. The positive twist that a SpaceX optimist would put on these numbers is that the spending on AI in particular is a positive, indicating that the company is not planning to settle on a niche market strategy, but instead will will go head-to-head with Anthropic, Google and OpenAI for the enterprise solutions markets. The negative spin is that this ambitious agenda will translate into tens of billions more in capital expenditures in the near years, creating a drag on the cash flows and value destruction if they lose the AI market competition.

Story takeaway: Given that SpaceX is continuing to invest substantial amounts in its space launch and connectivity businesses, I will increase reinvestment in the near term (years 1-5) by lowering how much they will generate as additional revenues for every additional dollar of capital invested (lower sales to capital ratios). With AI, where I was already assuming that reinvestment would be large (with a low sales to capital ratio), the tripling of target revenues will result in a surge in reinvestment to generate the higher sales.

Updating Story and Value

While the core story of SpaceX being a company with growth potential and strong competitive advantages that I framed prior to reading the prospectus remains intact, there are changes to that story that come from the information in the prospectus. The prospectus reinforces the notions that the company is best positioned in the connectivity business to generate both revenue growth and profits in the near term, that its cost advantages in the space launch business will persist and deliver profits, but that target market will be slower to develop, and that the AI business has both the largest target market and poses the biggest challenges, in terms of profitability and capital intensity, for SpaceX.

Bringing together my changes in target revenues, operating margins and reinvestment inputs allows for an update of the input table that I started this section with:

The enterprise value for SpaceX edges up from $1.21 trillion, in my pre-prospectus valuation, to $1.22 trillion with the post-prospectus numbers, and the overall equity value increases to $1.3 trillion, with almost all of the increase coming from the influx of $75 billion in cash from the IPO, albeit with a higher share count. The value per share of about $100 will need some revisiting as the IPO numbers firm up and more information is forthcoming on restricted stock units owned by employees, but just as I was finishing this post, a news story hit the wires that the offering price would be set at $135/share.

If I were to summarize the impact of the prospectus on my SpaceX story, it would be that it has made the story bigger, but also more volatile. There are a multitude of risks that SpaceX faces in each of its businesses, but the one that I would be concerned about the most is that it will overreach in the AI business, beginning with an overestimate of the target market for AI products and services and the strength of its own competitive position in that market, and following through with investments that reflect those misplaced assessments. Those concerns are heightened by a voting share structure that locks in Elon Musk’s control of the company, since there is little that shareholders can do to restrain the company, if SpaceX doubles down on capital expenditures and acquisitions in the AI space, even after it becomes clear that the AI market is much smaller than anticipated and/or that xAI’s offerings are not as good as the competition. If you add to this mix the antipathy that exists between Musk and Sam Altman, you have the potential for a UFC match between two monstrous egos, funded by tens of billions of dollars shareholder money.

Financial Statements and Value: The Life Cycle Effect

Financial analysis and valuation, going back to Ben Graham’s Security Analysis, has always been centered on financial statements, and that focus has become more intense over the last few decades as access to data and analysis tools has expanded. In fact, much of what passes for valuation has become financial modeling, where line items in financial statements are forecast based upon the historical time series, with the proverbial bottom lines being earnings and cash flows. Along the way, ratios computed from financial statement numbers are used to screen companies for investment quality. Some of these ratios, such as accounting returns on capital and equity, have become the basis for assessing company quality and competitive moats in the hands of consultants and investors. The SpaceX prospectus is a case study in why this approach to investing is often myopic and misleading, and why the informational value of financial statements will change as companies grow and mature.

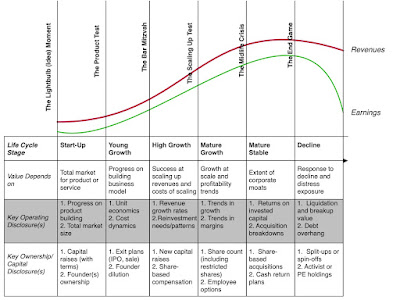

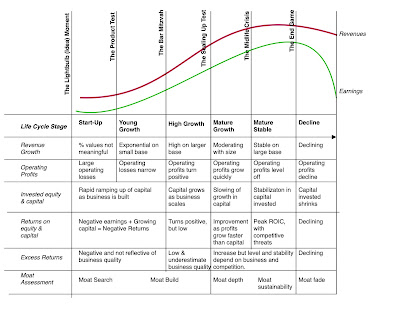

In valuing companies, you are always trying to forecast revenues, profits and cash flows in future, but they key questions you want answered and the drivers of value shift as you move through the life cycle:

As you can see, for young companies, the key determinants of value include sizing the total market and assessing unit economics, and not the proverbial bottom lines in accounting statements including the magnitude of revenues and profitability. As companies move through the life cycle from start-up to mature to decline, you should expect to see financial statements evolve as well. Young and high growth companies will generally report small revenues (though they expect those revenues to ramp up over time) and losing money and having negative cash flows is a feature, not a bug. As companies mature, revenues will get larger (albeit with lower growth) and profits turn positive, as will free cash flows available to return to shareholders in dividends and buybacks.

If you allow for the fact that all three of SpaceX’s businesses are young, falling in the young to high growth categories, the big questions driving value are about market size and unit economics, since the former provides the basis for revenue growth and the latter determines profitability. That is why, when looking at the prospectus for SpaceX it was the data on total addressable markets, unit economics and capital intensity that had a bigger impact on value, and this information, for the most part, was in the footnotes to the financials, rather than in the financial statements themselves.

For those who are focused on value metrics/constraints (consistently money making, high profit margins and accounting returns) and pricing multiples (low EV to EBITDA or low PE), the SpaceX prospectus is full of red flags. SpaceX is a company with small revenues and large losses, and paying a hundred times revenues for it (which is where a $1.8 trillion pricing would put it) seems foolhardy. I have no quarrels with this point of view, which animates old-time value investing, but this perspective comes with a cost in terms of investment choices. Investors who are wedded to never buying money losing companies or never paying more than twenty times earnings for a stock will end up with portfolios of mature (and declining) businesses. If that is their comfort zone, the strategy is perfectly defensible, but they should dispense with complaints about never being able to find high growth stocks to invest in or critiques of others who find these stocks attractive, notwithstanding the weak numbers.

There are many good arguments that can be made about why you should not invest in SpaceX, but basing that conclusion on the fact that they are money-losing or have negative cash flows or trade at a high multiple of revenues is both lazy and unconvincing. In contrast, making a case against investing in SpaceX because you believe that the target markets for its businesses will be far smaller than the company thinks they will be, or that cost and competitive pressures will drive margins down or even that you find its corporate governance structure and dependence on a personality (Elon Musk) off-putting is perfectly reasonable. If you do make that case, though, it is worth remembering that this is your point of view, and that disagreements about market size and profitability across investors, especially in young companies, are natural and healthy. In short, based on my inputs and story, I think that SpaceX is worth about $1.25-$1.3 trillion, but if you contend that it is worth $3 trillion or only half a trillion, it is neither my job nor my place to convince you that I am right and that you are wrong.

The IPO Pricing Game

In the coming weeks, you will undoubtedly be exposed to multiple perspectives on SpaceX, and that is healthy. That said, you will be better equipped to make sense of these perspectives, and perhaps incorporate some of the views into your own, and reject those that do not make sense, if you have an understanding of what an IPO process involves. In particular, understanding the motivations of the different players in the game (the investment bankers setting the offering price and managing the offering, the issuing company, the investors and traders jockeying for shares at that offering price and the traders positioning themselves for the first day of trading) will help determine whether you should be playing this game or sitting it out, at least for the moment.

The Bankers

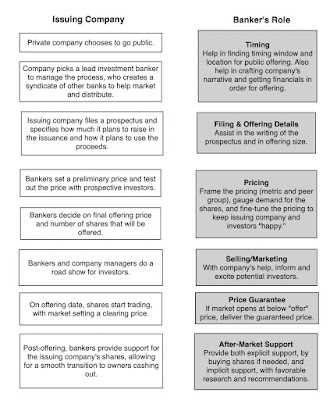

Let’s start with the sequencing that goes into a conventional initial public offering, though alternatives have emerged to it in recent years:

As you look at the role played by bankers to the IPO process, allowing them to keep a slice of the IPO proceeds, the SpaceX IPO is a testimonial to the dwindling value added by bankers on every dimension:

- Timing: It is urban (or market) legend that investment banks can time markets, and that this market timing can help determine the best time to go public. Just one look at the track record of market strategists at investment banks should dispense with this delusion, since banks (and most institutional investors) are (and have never been) good at gauging market momentum and shifts in mood.

- Filing and Offering details: It is true that there are technical details and logistical steps to filing a prospectus and setting offering details, but they are almost all mechanical. With SpaceX, I am not sure whether the prospectus, as filed, was the work of a team of bankers, but if it was, I wonder what an entirely Grok-written prospectus would have looked like, and whether we would have noticed the difference.

- Pricing: In an IPO, the bankers’ mission is to price companies for their offering, not value them, and while they usually draw on pricing multiples and peer groups to make that pricing judgment, they are guided by the pricing in the most recent private transactions, usually in the form on venture capital rounds. With SpaceX, that task is simplified by the reality that this company, while private, has had active trading in its private shares, and that it was priced at roughly $1.2 trillion prior to the IPO process commencing. Adding the $75 billion in offering proceeds, and incorporating the advantages of increased liquidity from being a public company and becoming part of the S&P 500, it is not surprising that there is a sense that the offering will be priced at between $1.5 trillion to $2 trillion, with or without the investment banking input. My guess is that we will end up somewhere in the middle, with some handwaving about revenue multiples and other AI companies used to justify that pricing. (After I finished this post, a news story popped up that the offer price would be set at $135/share, translating into about a $1.8 trillion pricing for the company.)

- Selling/Marketing: In an age where investment banks have lost credibility and social media is where marketing happens, SpaceX can generate its own marketing spin, and has an army of influencers behind it. In addition, almost every institutional investor has a point of view on whether to own SpaceX or not, it is unclear what exactly a roadyshow can do to augment the sales pitch.

- Price guarantee: The pricing guarantee that investment bankers offer in initial public offerings is a mostly empty promise, since they systematically set offering prices at below (by 15-20%) what they believe the market will pay. That is the reason that the offer price for SpaceX will be set below the upper end of the range, and while the discount may seem like a significant loss to funders and current owners, the fact that the offering is for less than a tenth of the shares in the company will soften the blow.

- Post-market support: As a follow-up to the price guarantee, investment banks often offer after-market support for companies in the days after they go public, buying shares if the stock comes under selling pressure. With SpaceX, that option is off the table, since no investment bank has the capital to support the pricing of a two-trillion company, if investors turn negative on it.

In fact, given that banks are perhaps getting more from the initial public offering, in terms of publicity and allotments for their preferred clientele, than SpaceX is getting from their services, you could argue that the bankers should be paying the company for reflected glory, rather than charging them fees. The only good reason that I can think of for SpaceX not going the direct listing route, where you dispense with the kabuki dance of offerings and let the market set the offering price, is that the company needs the cash from the offering, and that route is much more difficult to take in a direct listing.

Issuer (Company, Founder and Investors)

Looking at the IPO from the SpaceX perspective, the public offering will provide benefits. For the investors in the company in its private form, including venture capitalists from early in its life to public investors in more recent years, the IPO will allow them to cash out, albeit after the lock-out period expires in a few months. For the company, the increased access to capital from being a public company will allow it to fund the capital expenditures and investment needs that emanate from the company’s ambitions in the AI business. For Elon Musk, the public offering has the potential to make him the first trillionaire in history, in addition to unlocking new pathways to further enrichment for meeting specified targets (including getting a million people on Mars).

Since some of these benefits have been in existence for many years, the fact that company stayed private for that period is an indication that there are costs to going public that have held it back. The first is that, notwithstanding Musk’s voting control of the company, become a public company will open SpaceX to market scrutiny, in the form of earnings reports every quarter and insider trading reports. The second is that the market is fickle, and while it is rewarding companies that invest in AI with high market prices today, it can change its mind and punish them for the same reason. The third is that while there is little that investors can do to trade and make money on overpriced private businesses, they can sell short on public companies.

Investors and Traders

SpaceX is a company that has been in the public eye for a decade or more, even as a privately owned enterprise, partly because of its social media boosters and partly because its space launches make it a magnet for attention. There are many who are drawn to the company, but unable to invest in it as a private business, will now have a chance to do so, if it goes public. But should they try to partake in the initial offering? The answer to that question depends on whether you are an investor, where you buy (sell) companies that you believe are trading under (over) their assessment of value and hope the gap closes or a trader, where you buy (sell) companies where you expect prices to go up (down) in the future, for a multitude of reasons, only some of which may relate to company fundamentals.

I am more investor than trader, and I say that without judgment, since the end game in markets is to make money, not score intellectual points. The truth is that I am not a very good trader, and I am better off staying in my preferred domain, which is valuation, albeit with no guarantees of a payoff. My valuation of SpaceX was driven by my interest in the company and belief that it is in unique, cutting-edge businesses, and my decision on whether to buy into the offering is therefore driven by my assessment of its value. At the rumored pricing of $1.8 trillion for the company, it is too richly priced for my tastes, given my valuation of $1.25-$1.35 trillion for the equity in the company. That does not mean that I will never buy the stock, since the market does change its mind, and if the price does drop by enough, my decision would change accordingly. It is worth remembering that Facebook was selling at half its offering price a few months after its IPO, and that Uber lost more than 50% of its market cap in the year after its public offering, moving both companies from over to under valued.

If you are a trader, though, the game changes. Specifically, the intrinsic value of the company is not central to your decision, perhaps even irrelevant, and your judgment on whether you seek to partake in the SpaceX offering will depend on your reading of market mood and momentum. I would not be surprised in the least to see the offering priced at $1.8 trillion, and see a jump in the price on the day of or in the weeks after the offering, and if that is your most likely scenario, being able to get into the offering at the offer price or even in the first few hours or days of trading will be a winning strategy. The risk, of course, is that momentum can shift quickly, causing a significant price drop, effectively making timing your trades right key to your trading strategy. The shifting and often unpredictable forces of mood and momentum are also the reason that as an investor, I would not sell short, notwithstanding my value assessment, even if the pricing for the company pushes from $1.8 trillion to $2 trillion or more.

A Loaded Bet on AI!

As the IPO process for SpaceX heats up in the coming weeks, you should prepare yourself for a flood of selling from the company and its bankers, with talk of possibilities and potential dominating the discussion, as well as arguments from the other side, where it will be framed as a vehicle for AI hype, destined to fail. If you are on the receiving end of these sales pitches, you should listen but check the numbers for plausibility and make your own judgments. For the bankers involved and the issuing company, the biggest danger to a successful offering is not that there will be near-term reality checks on their hype, but that the market mood will shift, either in the aggregate or specifically related to AI, in the weeks leading up to the offering. No matter what your views are about the SpaceX IPO, positive or negative, there is no denying that this company is a loaded bet on the AI and Elon Musk, and while that may concern some, there are others who will look at Musk’s track record with Tesla and feel the odds are in their favor.

YouTube

Attachments

Blog posts on SpaceX

Source link