Asia open: Middle East tensions drive oil higher as S&P 500 snaps winning streak

Key takeaways

- Renewed clashes between the U.S. and Iran involving Kuwait and Bahrain reignited geopolitical concerns, driving oil prices sharply higher and triggering a broad risk-off move across global equity markets.

- The AI-led technology rally faced its first meaningful challenge after Broadcom’s disappointing guidance raised concerns about the pace of AI infrastructure revenue growth, prompting investors to reassess near-term earnings expectations across the sector.

- Rising energy prices, resilient economic activity, and persistent inflation pressures have reinforced expectations for tighter monetary policy, with markets increasingly pricing a more hawkish Federal Reserve and a near-certain June rate hike from the European Central Bank.

- Chart of the day: WTI crude minor bullish trend remains intact above $95.10/bbl, key support with potential upside trigger at $100.00/bbl.

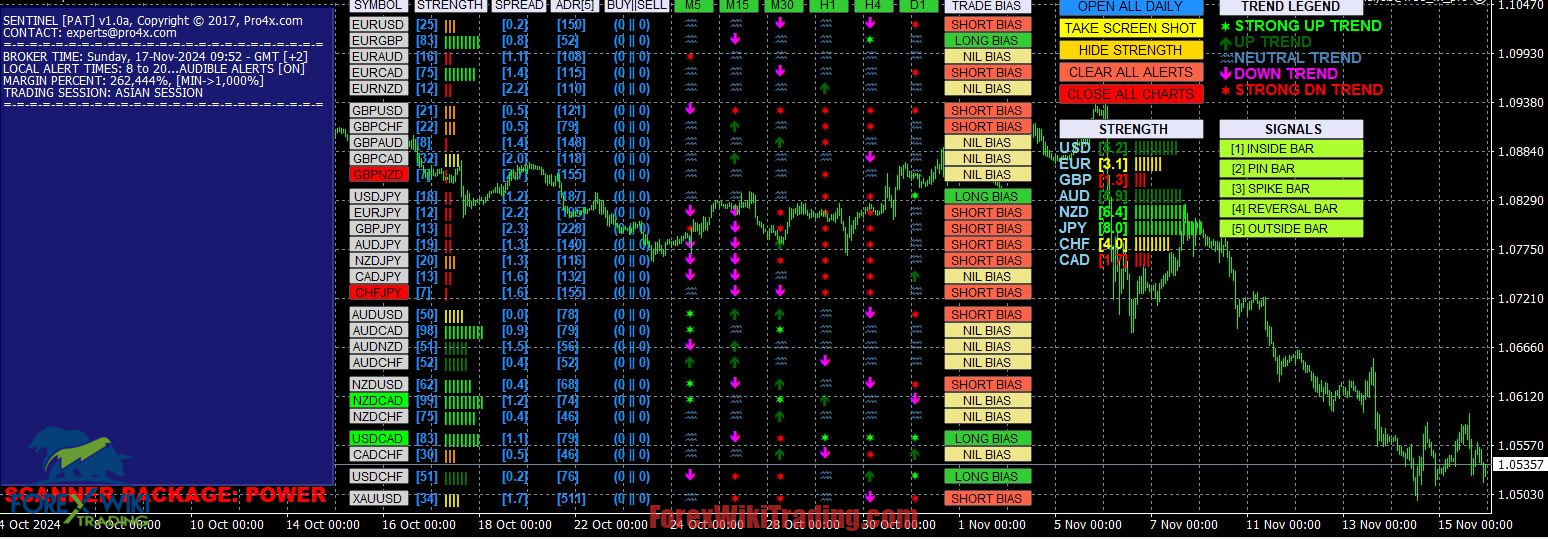

Chart of the day – WTI crude minor bullish trend remains intact

The minor bullish trend of the West Texas Oil CFD (a proxy for WTI crude oil futures) from the last Friday, 29 May 2026 low of $88.90/bbl remains intact (see Fig. 1).

Supported by an ascending trendline, watch the 95.10 key short-term pivotal support, and a clearance above the 100.00 near-term resistance (also the 20-day and 50-day moving averages) is likely to reinforce a further potential minor recovery towards the next intermediate resistances at 102.56 and 106.70.

On the flipside, failure to hold and an hourly close below 95.10 invalidates the bullish tone, setting up a choppy decline to retest the next intermediate supports at 91.40 and 89.00.

Top macro headlines

- US-Iran clashes disrupt peace: Overnight clashes between the US and Iran involving Kuwait and Bahrain resulted in one of the most serious flare-ups since the early April ceasefire, driving a sharp risk-off rotation across global markets.

- Tech AI rally falters: Broadcom Inc. issued a disappointing forecast signalling decelerating AI-fueled sales growth. This dragged down the broader tech sector, overshadowing early enthusiasm for Alphabet Inc.’s upsized $84.75 billion equity raise and SpaceX’s planned $75 billion IPO at $135 a share.

- Inflation risks trigger hawkish bets: Resilient consumer demand, corporate job additions, and a fresh surge in energy costs are fueling expectations of a hawkish Federal Reserve. Markets are increasingly betting the next Fed move will be a hike, while fully pricing in a 25-basis-point rate hike for the ECB’s June 11 meeting.

Key macro themes

- Geopolitical threat to energy supply: The renewed escalation in Middle East hostilities threatens to derail negotiations to extend the recent truce and reopen the Strait of Hormuz. This is directly pressuring global energy supply lines and pushing crude prices higher.

- AI growth meets reality check: The stark contrast between massive capital raises in the tech space and Broadcom’s weak forward guidance suggests the AI sector is facing resistance, prompting investors to re-evaluate the near-term revenue potential of AI infrastructure.

- Central banks cornered by inflation: The combination of a robust labour market and a sudden commodity shock leaves central bankers trapped. Policymakers are under immense pressure to raise or maintain borrowing costs to prevent inflation from reigniting, directly stalling the recent equity rally.

Global market impact

Equities: The S&P 500 fell 0.7%, snapping a nine-day winning streak. The Dow dropped 1.2%, and the Nasdaq 100 declined 0.3%. Software ETFs slid 4.3%. Globally, the MSCI World Index reversed early record highs, closing down 0.7%.

Fixed Income: The US 10-year Treasury yield advanced 5 bps to 4.49%. In Europe, Germany’s 10-year yield rose 6 bps to 3.04%, and Britain’s 10-year yield climbed 7 bps to 4.93%.

FX: The US Dollar Index rose 0.3% on safe-haven flows and hawkish rate bets. The Euro declined 0.3% to $1.1598, and the British Pound fell 0.3% to $1.3420.

Commodities: WTI crude surged 2.8% to $96.20/bbl, while Brent briefly topped $97/bbl amid geopolitical fears. Spot gold fell 1.2% to $4,435/oz, pressured by higher yields and a stronger USD to retest its key 200-day moving average.

Asia Pacific impact

- Stock markets are undergoing a setback: Moving in line with weak performances seen in the US stock market overnight, key Asia Pacific stock indices are on the defensive and in profit-taking mode in today’s Asia session, where intraday losses were seen across the board. Nikkei 225 (-1.4%), KOSPI (-1.5%), Hang Seng Index (-1.5%), China A50 (-1.5%), CSI 300 (-0.8%), ASX 200 (-1.2%), and STI (-1.2%).

- Trade & tariffs optimism: Sentiment was partially supported by expectations of potential US tariff reductions on non-critical Chinese goods. Based on 2025 figures, this could cover approximately 10% of US imports from China, potentially revitalising direct exports.

- Yen intervention watch: The Japanese yen remained under significant pressure, falling 0.1% to hover near a multi-decade low of 160.08 per US dollar in today’s Asia opening session, leaving markets highly alert to potential intervention by the Bank of Japan. Key near-term support for the USD/JPY rests at 159.45 (Wednesday, 3 June 2026, minor swing low).

Top 4 events to watch today

- ECB President Lagarde Speech – 4:00 pm SGT Impact: EUR/USD, EUR crosses, DAX

- US Initial & Continuing Jobless Claims – 8:30 pm SGT Impact: USD, US Treasuries, US stock indices

- Fed Speak (Barkin) – 8:30 pm SGT Impact: USD, US Treasuries, US stock indices

- BoE Governor Bailey Speech – 11.40 pm SGT Impact: GBP/USD, GBP crosses, FSTE UK 100

Opinions are the authors’; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. The provided publication is for informational and educational purposes only.

If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please refer to the MarketPulse Terms of Use.

Visit https://www.marketpulse.com/ to find out more about the beat of the global markets.

© 2026 OANDA Business Information & Services Inc.