BlackRock, JP Morgan & More Test Tokenized Collateral on Hedera, Stellar, Canton

For years, crypto investors have been told that institutions were coming.

Now we are starting to see what that may actually look like.

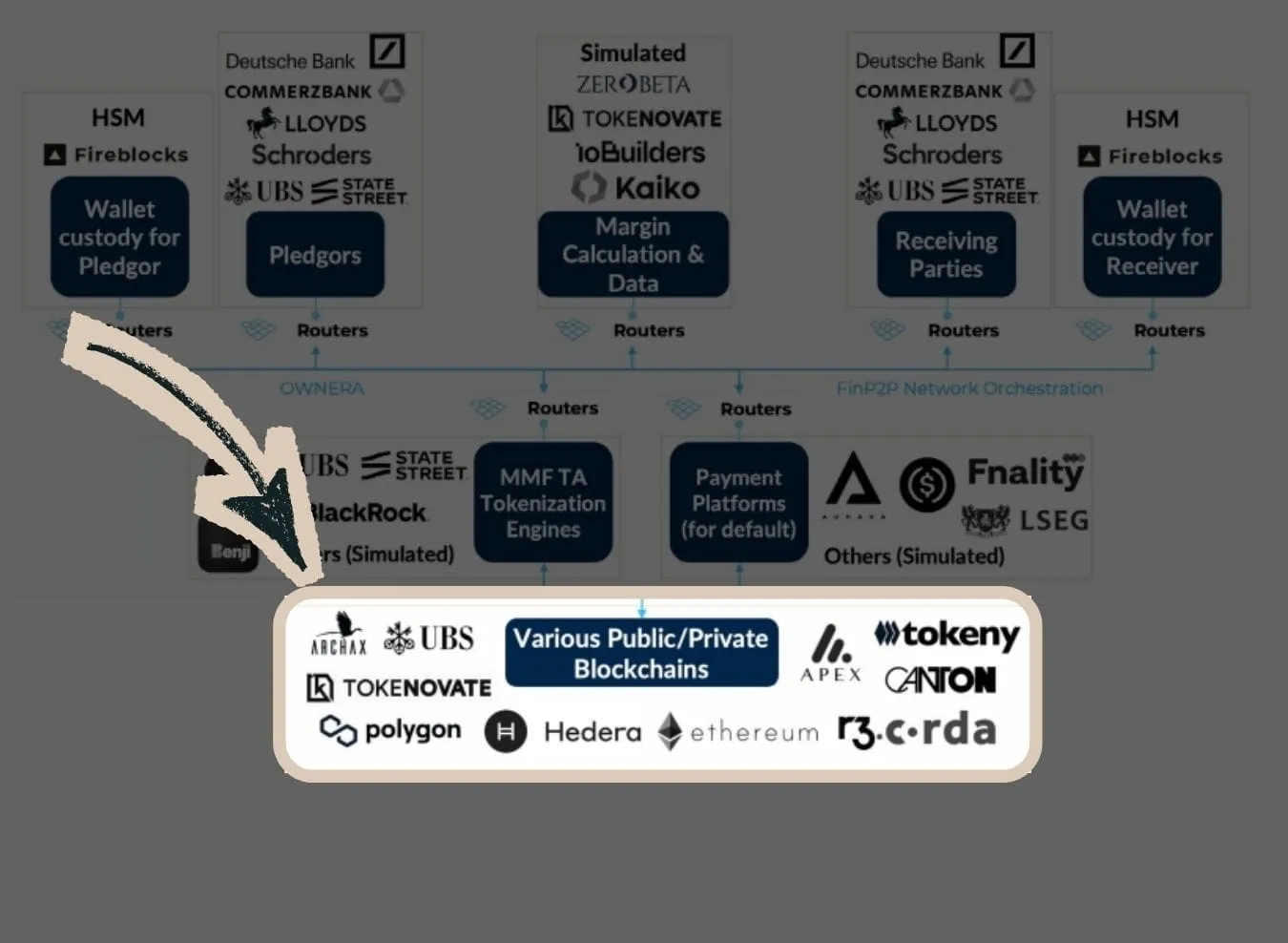

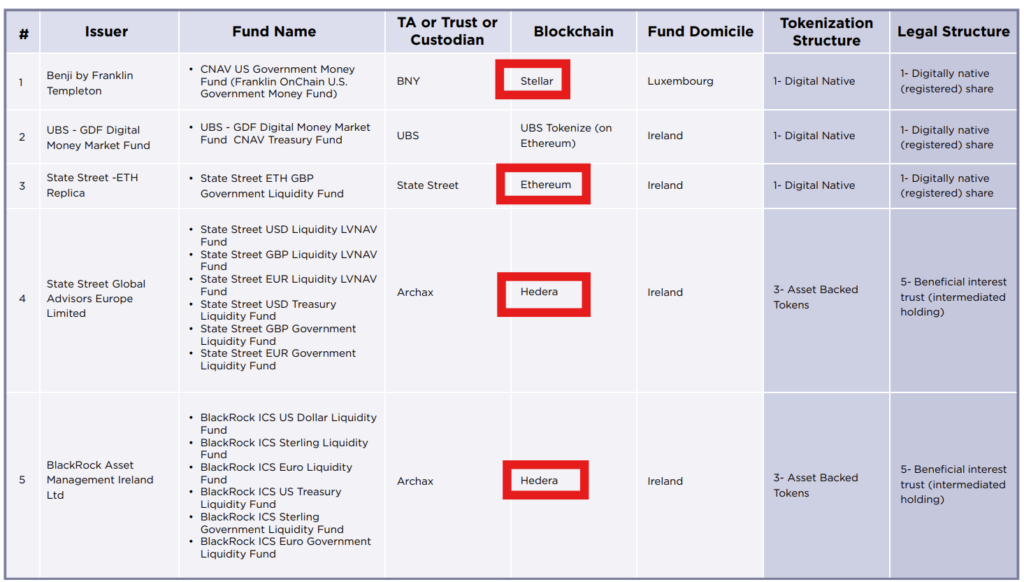

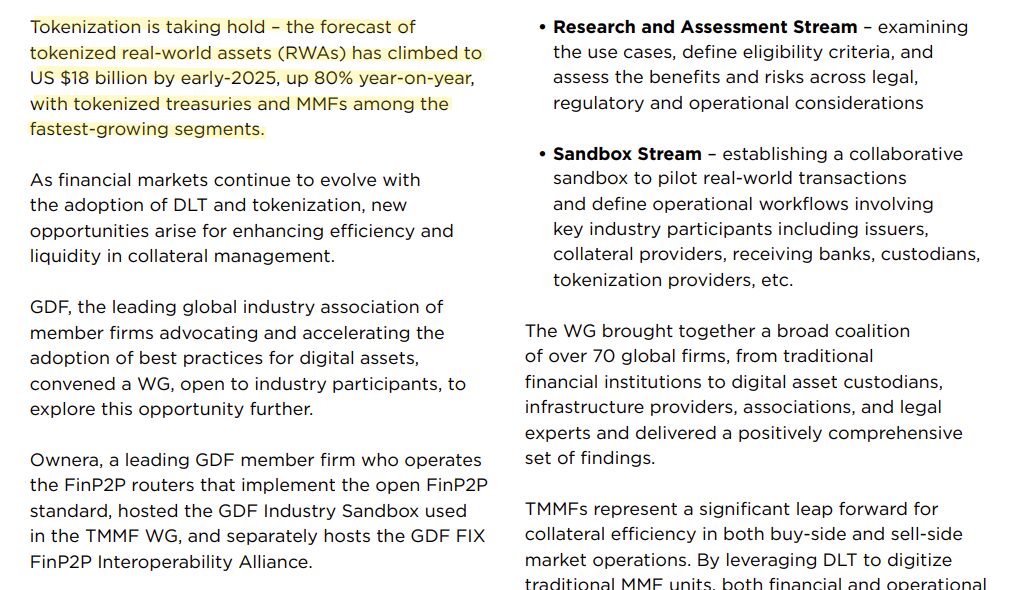

A new report titled The Case for Collateral Mobility in Europe & the UK Using Tokenized Money Market Funds lays out one of the clearest institutional blockchain use cases we have seen in a long time: using tokenized money market funds, or TMMFs, as collateral in real market workflows. This was not a niche experiment. The report lists more than 70 organizations involved across banks, asset managers, custodians, legal experts, infrastructure providers and market operators, including BlackRock, Citi, Deutsche Bank, Fidelity, Franklin Templeton, Goldman Sachs, JP Morgan, Moody’s, State Street, UBS, the London Stock Exchange Group and many more. It also lists Layer 1 environments including Besu, Canton Network, Corda, Ethereum, Hedera, Polygon and Stellar.

That is why this story matters.

This is not another vague “blockchain could help finance one day” narrative. It is a serious, detailed attempt to test whether tokenized collateral can improve one of the most important functions in modern markets: moving collateral quickly, legally and efficiently across institutional systems. The report says the working group combined legal and market analysis with a sandbox stream designed to pilot real-world transactions and define operational workflows involving issuers, collateral providers, receiving banks, custodians and tokenization providers.

And the implications are bigger than many investors probably realize.

Why tokenized collateral matters so much

Collateral is the backbone of huge parts of global finance. It supports derivatives, repo markets and other funding arrangements, and when collateral gets stuck, delayed or operationally cumbersome, stress can spread fast.

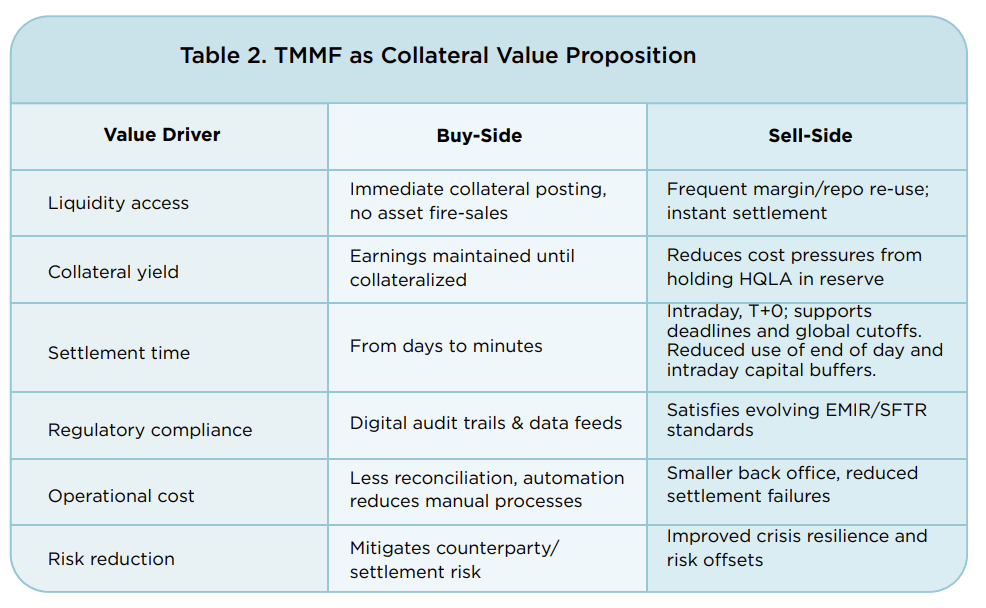

The report directly points to the 2022 UK LDI crisis as a reminder that reliance on cash collateral and cumbersome redemption-subscription workflows can worsen liquidity pressure during market stress. It argues that tokenized money market funds could help reduce some of those frictions by preserving yield, avoiding unnecessary redemption into cash and making collateral easier to move. The foreword says TMMFs combine the familiarity and liquidity profile of traditional MMFs with the settlement speed, programmability and transparency enabled by distributed ledger technology.

That is what makes this so important for crypto.

The real breakthrough for blockchain may not come first from retail payments or meme speculation. It may come from improving the hidden plumbing of financial markets.

What the report actually found

One of the strongest parts of this report is that it goes beyond theory.

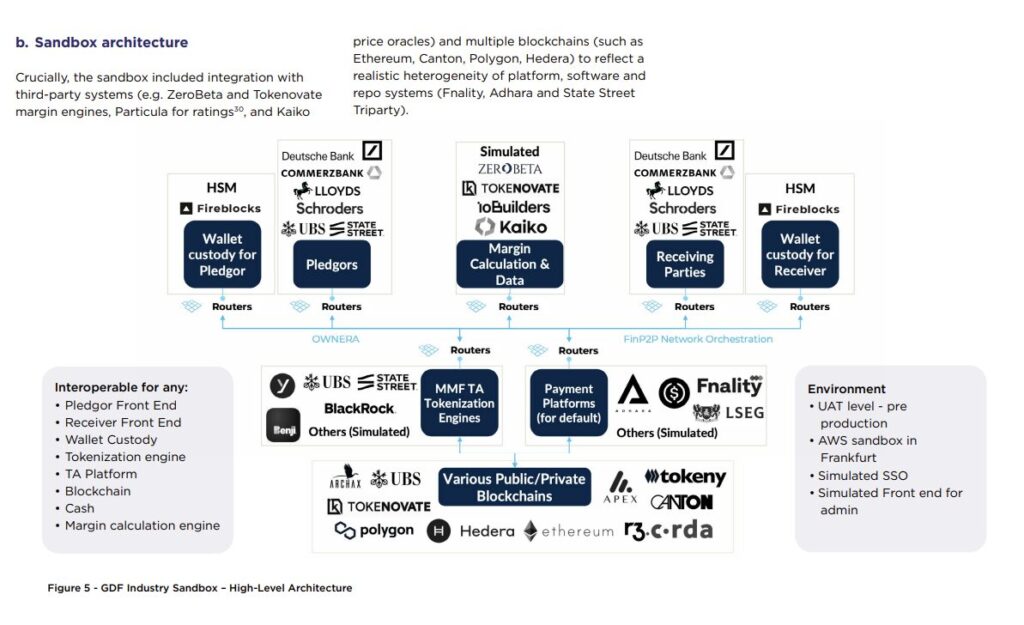

The sandbox was set up as a production simulation environment and ran six progressively more complex simulations, including simple bilateral transfer, integrated margin calls, a depeg event and substitution scenario, an insolvency default scenario, triparty funding, and a workflow described as moving “from SWIFT to collateral settlement in seconds.” The report says the sandbox demonstrated that TMMFs can operate as enforceable collateral today and unlock efficiencies, resilience and interoperability that traditional systems struggle to match. It also says the sandbox validated TMMFs as a production-ready collateral instrument.

That is a very different message from saying institutions are merely “interested” in blockchain.

According to the report, the simulations showed operational feasibility, real-time risk management, legal enforceability under stress, interoperability across markets and ledgers, liquidity and yield advantages, and a degree of market readiness that makes the future of collateral mobility “not hypothetical but achievable today.”

That line is powerful, because it tells you the report is not pitching a distant dream. It is arguing that the model is already workable.

The biggest efficiency gap: days versus seconds

If you want the simplest reason why this is important, it is this: speed.

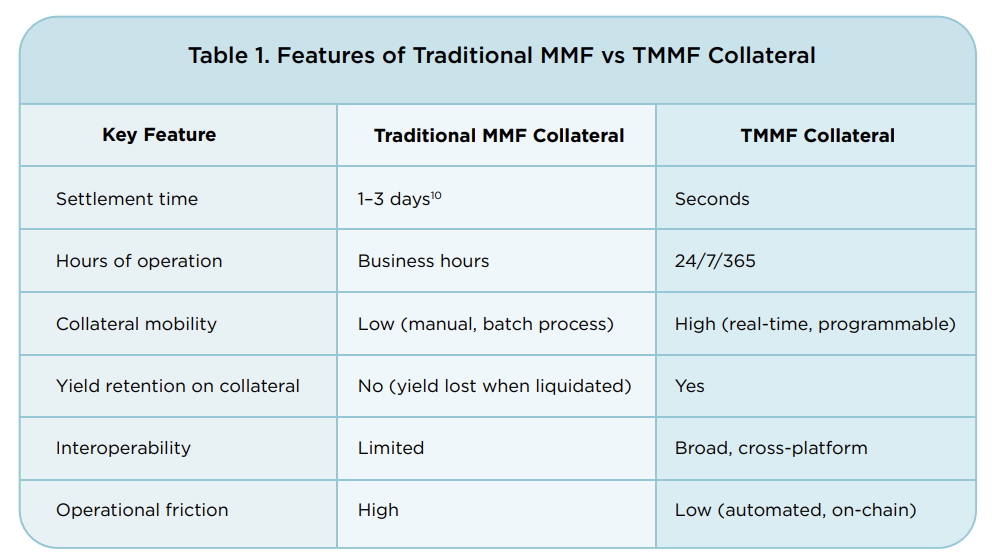

The report’s comparison between traditional MMF collateral and tokenized MMF collateral is striking. It says traditional MMF collateral typically takes 1–3 days to settle, operates during business hours, offers low collateral mobility and high operational friction. By contrast, the tokenized version is described as settling in seconds, operating 24/7/365, offering high real-time programmability and preserving yield on collateral.

That is not a minor upgrade.

That is the difference between finance running on cut-off times, intermediaries and batch processing, and finance operating on real-time rails.

The report goes even further in its later sections, saying TMMF transfers can settle in seconds instead of the 1–3 day cycles typical of traditional MMF transactions, while supporting always-on liquidity and more seamless collateral posting.

For investors, that is the real alpha in this story.

Not the usual “coin X to the moon” narrative.

Not empty institutional buzzwords.

But a clear demonstration that blockchain-based infrastructure may be able to solve real bottlenecks in capital markets.

This was not a one-chain future

Another major takeaway is that the institutional future described in the report is multi-ledger, not single-ledger.

The architecture and participant list make it clear that this sandbox was built around interoperability, routing and orchestration across different systems. Ownera’s FinP2P routers are specifically mentioned in connection with the sandbox, and the simulations include cross-system workflows, third-party integrations, and links between legacy messaging and tokenized settlement. The report’s sixth simulation explicitly extended the infrastructure to connect legacy SWIFT-based margin messaging to on-chain collateral settlement.

That matters because many retail investors still think in simplistic terms: one chain wins, everyone else loses.

That is not what this report suggests.

Instead, it points toward a future where multiple ledgers, different legal structures, interoperable standards and institution-friendly middleware all work together. In that world, the likely winners are not necessarily the loudest projects, but the networks and infrastructures that can integrate with legal, regulatory and operational requirements.

Why Hedera, Stellar and Canton are getting attention

For crypto audiences, three names will stand out immediately: Hedera, Stellar and Canton Network.

These are not random mentions. They appear in the Layer 1 list inside a report centered on collateral mobility, tokenized money market funds and institutional operational testing. That does not mean the report is declaring a single winner. But it does mean these networks are associated with a far more serious and commercially relevant conversation than retail speculation alone.

For Hedera, this supports the long-running thesis that enterprise-grade infrastructure and tokenization could become a major part of its story.

For Stellar, it reinforces the idea that the network’s role in asset issuance and regulated financial products may still be underappreciated by the wider market.

For Canton, it strengthens the argument that permissioned or institution-oriented environments could play a central role in the tokenization stack, especially where regulated market structure is involved.

In other words, this report is bullish not because it “picks a winner,” but because it makes the institutional tokenization thesis look far more tangible.

The legal side may be even more important than the technology

Crypto investors often focus on throughput, speed and settlement.

Institutions care about something else just as much: enforceability.

That is why one of the most important parts of the report is the legal and insolvency analysis. The sandbox included a default scenario designed to test enforcement and recovery. The report says the six simulations showed that posting TMMFs as margin can work end-to-end under current legal and operational structures, and it repeatedly emphasizes legal certainty and enforceability as central to the model.

This is critical.

A faster system means very little if it breaks in a dispute, a default or a stressed market event. The fact that this report spent so much effort on legal form, insolvency access and cross-jurisdictional treatment tells you this was built for serious institutional consideration, not just innovation theater.

Why this could become one of blockchain’s biggest real-world use cases

There is already a lot of excitement around tokenized treasuries and RWAs.

But tokenized money market funds may prove just as important, or even more important, because they are not just passive wrappers for traditional assets. They can potentially become active collateral instruments inside capital markets.

The report says tokenized RWAs had climbed to $18 billion by early 2025, up 80% year on year, with tokenized treasuries and money market funds among the fastest-growing segments. It frames TMMFs as a way to enhance efficiency and liquidity in collateral management, and as a practical bridge between traditional fund structures and blockchain-based settlement.

That is the key point.

This is not only about putting assets on-chain.

It is about making them usable in the live mechanics of finance.

And once that starts to happen, tokenization stops being a branding exercise and starts becoming infrastructure.

Our take

The biggest takeaway here is not that traditional finance has suddenly “gone full crypto.”

It is that major institutions are getting increasingly specific about where blockchain can actually add value.

And based on this report, one of the clearest answers is collateral mobility.

When you see BlackRock, Citi, Deutsche Bank, Goldman Sachs, JP Morgan, Moody’s, State Street and UBS in the same conversation as Hedera, Stellar, Canton, Ethereum and Polygon, that should tell you something important. The market is slowly moving past generic blockchain experimentation and toward live testing of real use cases with operational, legal and settlement implications.

That does not guarantee instant adoption.

It does not guarantee one network wins.

And it does not automatically mean token prices should explode tomorrow.

But it does suggest something much more meaningful:

The infrastructure phase of tokenization is becoming real.

If tokenized money market funds can settle in seconds, move across interoperable environments, preserve yield and remain legally enforceable under stress, then this could become one of the most important real-world blockchain use cases yet. The report’s own conclusion is that the future of collateral mobility is not hypothetical, but achievable today.

That is why investors should be paying attention.

Because this is not just a story about crypto narratives.

It is a story about the future plumbing of finance.

Source link