HDFC Bank Q4 FY26 Results Analysis – Bramesh’s Technical Analysis

HDFC Bank, India’s largest private sector lender, released its Q4 FY26 (Jan–Mar 2026) and full-year results today. The numbers came in in-line to marginally better than street estimates, showing operational resilience despite ongoing margin pressure.

Key Standalone Figures (Q4 FY26)

|

Metric |

Q4 FY26 |

YoY Change |

QoQ/Notes |

|---|---|---|---|

|

Net Profit |

₹19,221 cr |

+9% (from ₹17,616 cr) |

In-line with ~₹19,000–19,200 cr consensus |

|

Net Interest Income (NII) |

₹33,082 cr |

+3.2% |

Muted growth |

|

Interest Income |

₹76,610 cr |

-1.1% |

Slight decline |

|

Total Income |

₹89,809 cr |

Marginal + |

– |

|

Deposits |

₹31.05 lakh cr |

+14.4% |

Strong growth |

|

Advances (Loans) |

₹29.60 lakh cr |

+12% |

Healthy but deposits outpacing |

|

GNPA Ratio |

1.15% |

Improved (1.33% YoY, 1.24% QoQ) |

Asset quality strengthening |

|

NNPA Ratio |

0.38% |

Improved (0.43% YoY) |

– |

|

NIM |

3.38% (total assets) 3.53% (interest-earning) |

Under pressure |

Typical post-merger trend |

|

Provisions |

₹2,609 cr |

-18% |

Lower credit costs |

|

Operating Profit |

₹27,802 cr |

+4.8% |

– |

Full Year FY26:

- Net Profit: ~₹74,671 cr (+11% YoY)

- RoA: 1.94% (up from 1.91%)

Dividend:

- Final dividend of ₹13 per share (face value ₹1)

- Total dividend for FY26: ₹15.50 per share (including ₹2.50 interim)

- Record date: June 19, 2026

What Stands Out (Positives)

- Deposit momentum (+14.4% YoY) outpacing loan growth is excellent — improves LDR and reduces reliance on expensive borrowings.

- Asset quality surprise: GNPA and NNPA ratios improved both YoY and QoQ; provisions fell sharply. This is a big relief after merger-related integration noise.

- Bottom-line delivery: 9% profit growth with lower credit costs shows cost discipline and steady core operations.

- Shareholder-friendly: Healthy dividend payout continues HDFC Bank’s tradition.

- Capital Adequacy Ratio (CAR) remains strong at ~19.7%.

Areas of Caution

- NIM compression is visible — NII grew only 3.2% despite 12% loan growth. Higher cost of deposits and rate transmission to borrowers are still biting.

- Interest income actually dipped slightly YoY, highlighting the margin challenge in a high-rate environment.

- Growth is steady but not explosive (loans at 12%, deposits 14.4%) — typical of HDFC Bank’s post-HDFC Ltd merger normalization phase.

Overall Verdict

Steady, resilient quarter with improving asset quality — exactly what the street wanted to see amid recent governance overhang (chairman resignation). The results are not spectacular but clean and reassuring, beating muted expectations on profitability and credit costs while maintaining strong balance-sheet growth.

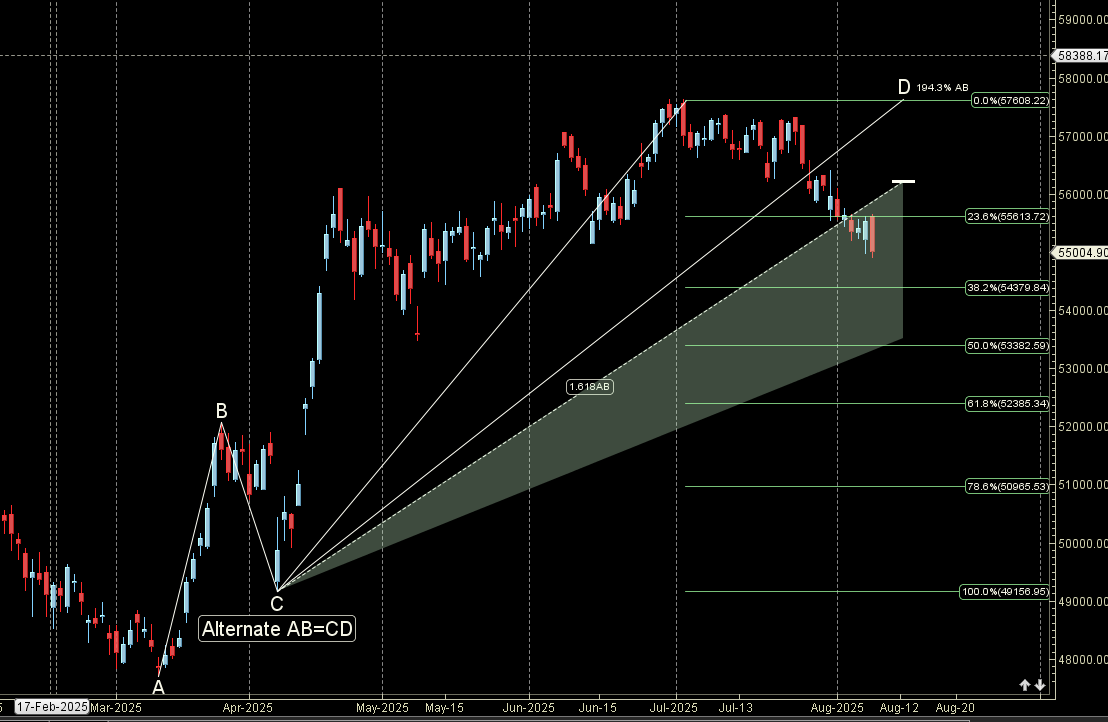

Technicals :

Above 820 can see rise till 850-864

Related

Source link