Frequently Asked Questions On Reverse Iron Condor Options Strategy

Contents

This options strategy is most commonly known as the Reverse Iron Condor, or, less commonly, as the RIC.

But don’t call it the Upside-down Condor.

Because that is an unwieldy name and I’ve never heard it called that way – even though its payoff graph looks as such:

The way a trader might have constructed this reverse iron condor structure is to buy an out-of-the-money put debit spread with the long option around the 30-delta on the option chain:

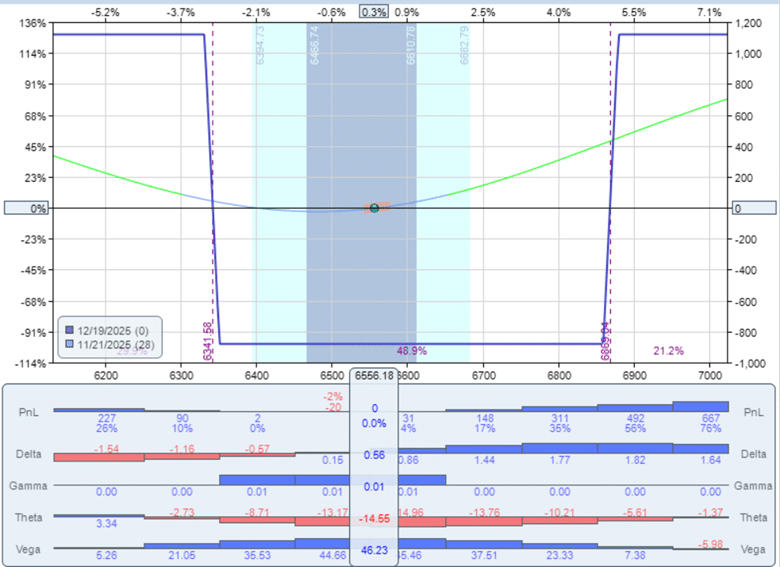

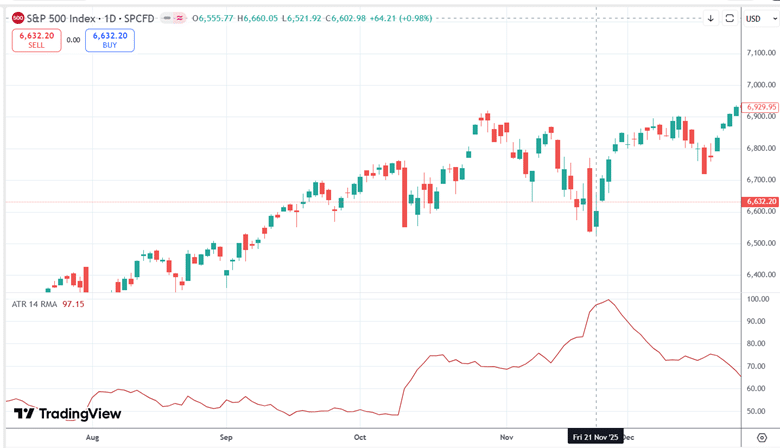

Date: Nov 21, 2025

Price: SPX @ 6556

Put Debit Spread:

Buy one contract Dec 19 SPX 6350 put @ $90.35

Sell one contract Dec 19 SPX 6330 put @ $86.05

Debit: -$430

Then the trader buys an out-of-the-money call debit spread that costs about the same as the put debit spread and maintains the same width.

Call Debit Spread:

Buy one contract Dec 19 SPX 6860 put @ $31.30

Sell one contract Dec 19 SPX 6880 put @ $26.80

Debit: -$450

So, the net debit for the Reverse Iron Condor is $880.

Answer: That is the trader’s choice.

The strikes and their pricing can be planned so that all four legs of the trade are entered as a single order, avoiding the risk that the market moves against the spread before the other opposing spread is still waiting to be filled.

On the other hand, a four-legged trade is more difficult to fill than two separate spread trades.

If doing two separate trades, try to get them filled close to about the same time.

Answer: The call debit spread was aligned to match the cost of the put debit spread.

Because of the volatility skew and the disparity in implied volatility across strikes, the call spread needed to be placed at a more distant strike level to achieve that equal pricing.

Answer: This makes the initial payoff graph at the current time (T+0 line) more symmetrical to achieve a near-zero delta at the start of the trade.

In our example, the position delta was 0.52.

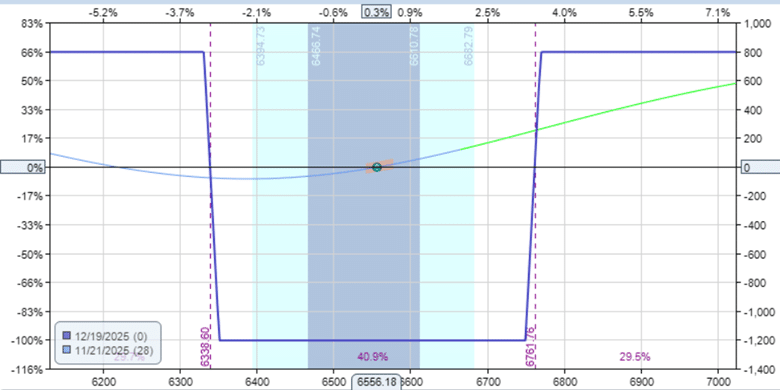

If we had made the expiration payoff graph symmetrical instead, as in the below…

Then the T+0 line is no longer symmetrical.

It has a directional bias of a positive delta of 0.92.

Answer: The maximum risk is the total debit paid to enter the position.

In this example, $880 is the max risk.

This occurs when the underlying price fails to move significantly, and the spreads have reached expiration.

In that situation, both debit spreads expire worthless, resulting in the loss of the entire premium paid for the position.

Answer: All the options expire on the same day.

In this example, they expire in 28 days.

Giving the trade more time to expiry (such as 60 days till expiration) will allow the trader more time for the market to make a big move.

Or if they expect the market to make a big move in the very near future, they may reduce the days-to-expiration.

Many traders will not hold the trade through to expiration to avoid the maximum loss.

Instead, the position is often managed earlier – frequently before the halfway point of the trade’s duration.

If the planned profit target had not been reached by that time, the trader may choose to close the position and accept whatever profit they have or accept a smaller loss rather than risk the spread continuing to decay in value all the way to expiration.

Answer: The maximum profit equals the width of one spread (either the call spread or the put spread) minus the total debit paid for the position.

This occurs if the underlying price moves beyond either long strike at expiration, allowing one side of the position to reach its full value.

This also assumes that the entire position is held until expiration as one combined trade.

In our example, the max profit is:

$2000 – $880 = $1120

It is possible, albeit quite rare, for a Reverse Iron Condor to make more than the theoretical maximum profit if the position is managed by legging out instead of holding the full structure to expiration.

For example, the market may move way up, and the trader takes nearly profit on the call spread.

And then the market moves way down, and the trader takes profit on the put spread as well.

Answer: The take-profit level depends on the individual trader’s preference.

Some traders may choose to take profits at around 25% to 50% of the maximum risk.

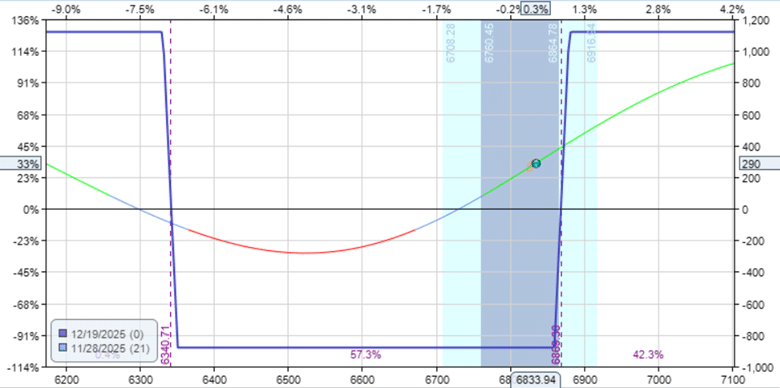

For example, some may choose to exit when they see a profit of $290 one week into the trade – that is more than 30% of the max risk…

Others may target 25% to 50% of the maximum potential profit.

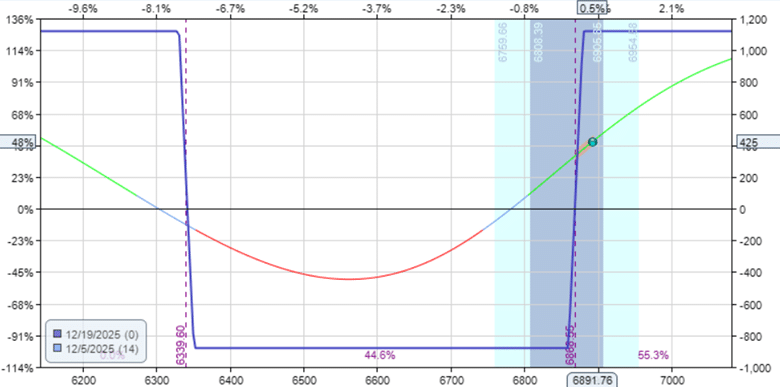

If the trade were held for another week, its profit would be $425, which would reach 35% of its maximum potential profit…

And yet others may use technical analysis to watch price action and determine when the price stops moving, at which point they take off the trade.

Answer: It depends on the trader’s risk tolerance and trade plan.

A common approach is to exit the trade if the loss reaches about 50% of the debit paid for the position.

In our example, if the position is down -$440, that is a signal to exit the trade.

Many traders also use a timed exit.

For example, they may close the position once more than half of the trade’s duration has passed.

This helps avoid the accelerated theta decay that occurs as expiration approaches.

Answer: When the price of the underlying is making big moves or is expected to make big moves.

Some indication of this can be…

- When the ATR is high. The Average True Range measures the size of price moves.

- When VIX is high, which indicates increased volatility and typically larger price moves.

- When the VIX Futures term structure is in backwardation.

- When right after a large price drop shock.

Our example trade started when ATR was quite high at 97 and VIX at 25 in the morning, right after that big red candle…

Answer: Of course not.

Under normal market conditions, the reverse iron condor is expected to lose money over the long run.

So don’t use the RIC all the time, like in campaign-style trades.

Use only in specific market conditions where you expect a large move.

Even then, it may not work.

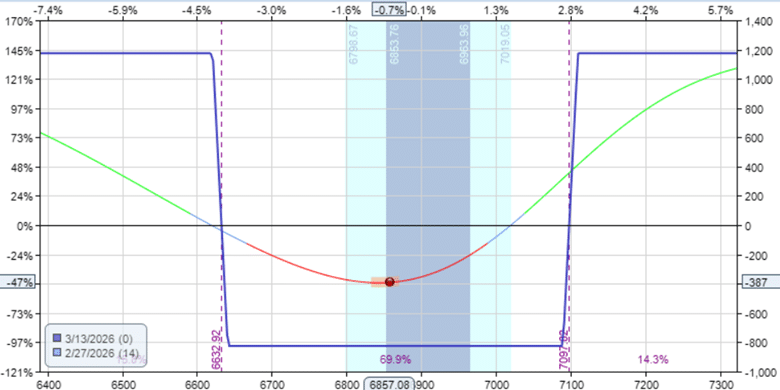

Here is an example of an RIC on SPX started on February 13, 2026, when ATR was 81 and VIX at 21, and VIX Futures term structure in slight backwardation.

And 14 days later, the trade had not hit its profit target.

With only 14 days left till expiration, this is the halfway point in the duration of the trade.

The P&L is -$387, or 47% of the debit paid.

The trade is at its stop loss and timed exit points.

So, the trader should exit the trade at a loss at this point.

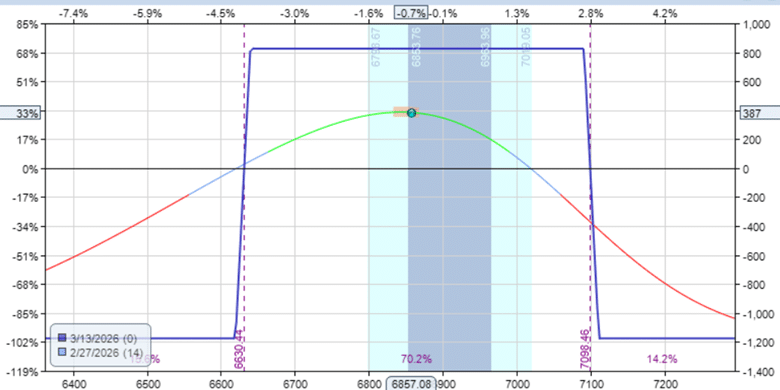

Question: Does that mean that if we did the reverse, then the trade would have won?

Answer: Yes, if we had done an iron condor instead – with the same strikes and expiration…

The iron condor would have made about 50% of its max profit.

Answer: The term “iron” means the option strategy contains both call and put options.

Answer: Yes.

It can be constructed using only puts or only calls.

However, it is no longer called a Reverse Iron Condor.

Instead, it would be called a Reverse Condor.

Also, one of the spreads would be an in-the-money spread, which would be more difficult to fill due to wider bid/ask spreads.

Hence, an iron reverse condor is preferred.

Question: What are the Greeks of the Reverse Iron Condor?

Answer: A reverse iron condor is a long volatility strategy that profits on large price moves.

Refer to the first screenshot at the top of the article to see the Greeks histogram of the example SPX trade.

Delta: This is the primary driver of the RIC.

While the delta is low or neutral to start, once the price moves, the trade becomes directional, and we want the price to continue moving in that direction.

If the price rises, the call spread gains value, and the delta becomes positive.

If the price falls, the put spread gains value, and the delta becomes negative.

This is a positive gamma trade. It means…

If the price moves up, delta quickly becomes more positive.

If the price moves down, delta quickly becomes more negative.

The effect is that the more the price moves in one direction, the more the position benefits, and those gains accelerate as the price continues in that direction.

A large positive gamma indicates that the trade is sensitive to price movements.

It is most sensitive to price movement when the price is at the bottom of the T+0 curve.

A positive gamma trade will have negative theta.

So the RIC will lose value each day, with time working against the trade because of its negative theta.

It has positive vega, which benefits the trade if implied volatility increases.

Although it usually doesn’t have a huge impact since the long and short options partially offset each other in terms of vega.

A reverse iron condor is a long-volatility strategy to be applied tactically when a large, near-term price move is expected.

Think of it as a situational tool, reserved for moments when a significant price move is likely.

Like an umbrella ready for use in the rain, we don’t want to carry it around all the time.

We hope you enjoyed this article on the reverse iron condor strategy.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Source link