Adventures in Private Investing–Cards on the Table Part II – Churning and Burning

The next 3 weeks will be huge for me. The NASDAQ IPO page even gave me the courtesy of lining up both tickers side by side.

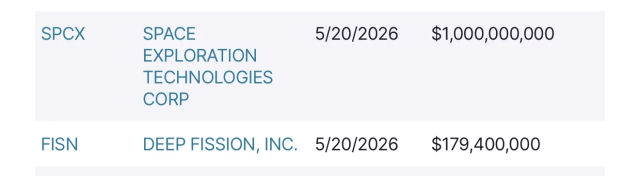

I’m in Deep Fission at $3 and it’s going to IPO around $25 this week, probably Thursday or Friday. That’s 8x.

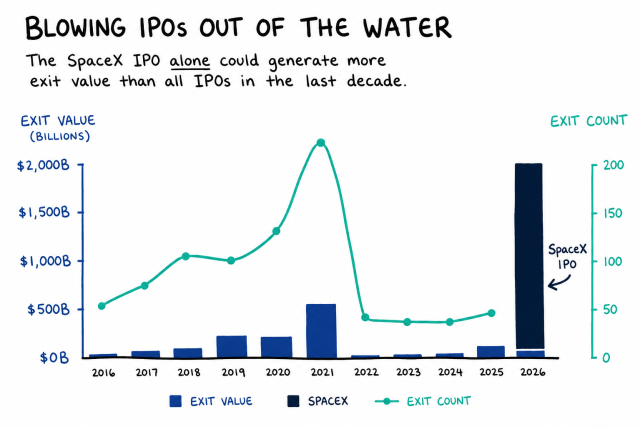

I’m in SpaceX at $22.40 and it’s going to IPO at $210, rumored to be June 12th. That’s almost 10x.

SPCX will be the largest IPO of all time. We are witnessing history.

Do you see my vision now? They will be taking about the IPO generation of 2026-2030 in financial history textbooks for years to come. Bubble this, bubble that, that’s just an old colloquialism that belongs in the 1990’s and it’s preventing you from getting rich.

Anyway. My next 10 companies.

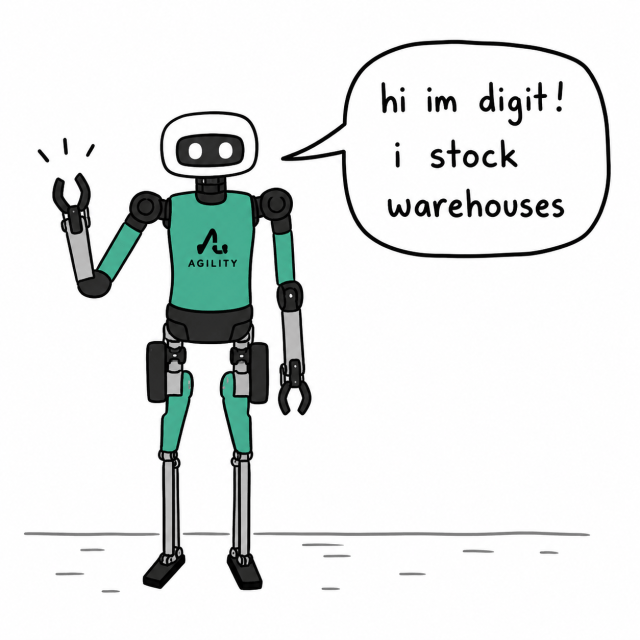

15. Agility

Date of investment: October 2025

Entry valuation: $2.15 billion on a 0/0 SPV

Bet size: 2 units

IPO status: given they’re on track to be first to market, 1-2 years?

Agility, founded in 2015, is building one of the first commercially deployed humanoid robots for real industrial work. Their robot, Digit, is designed specifically for warehouses and logistics centers: walking around human-built environments, carrying totes, and plugging into existing automation systems. They’re a vertically integrated company, having created their own intelligence system called “Arc” to operate Digit. They have partnerships with Amazon and GXO for industrial warehouse work. Because of their focus on safety (expecting OHSA certification in 2026), they expect to Digit to be one of the first to market robots to work outside of confined spaces.

Agility is one of the least talked about players in the humanoid game (along with the next company, Apptronik). They don’t market through social media the way Elon and Brett Adcock do. As a result of staying low-key, I think they have an extremely favorable valuation despite a profile that screams first to commercial-ready. This was a direct deal from “Aurelius Investments”, my Chicago firm that’s trying pivot away from layered secondary deals, so the economics are amazing.

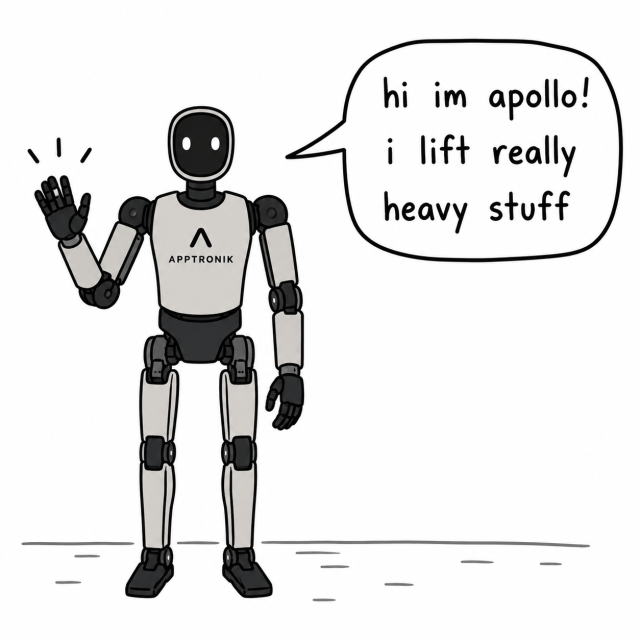

16. Apptronik

Date of investment: November 2025

Entry valuation: $5.7 billion on a 5/0 SPV

Bet size: 1 unit

IPO status: given they’re on series A, probably 2+ years

Much like Agility, Apptronik is building Apollo, a general-purpose humanoid robot aimed at becoming a labor platform for factories, warehouses, and eventually broader physical-world work. The only difference is that Apptronik will partner with Google Deepmind for their robotics brain while Agility develops their own. Started in 2016, Apptronik’s culture is steeped in NASA engineering discipline. Their original prototype was Valkyrie. Great low-key engineering team. They’re looking to deploy Apollo to work with Mercedes-Benz and Jabil in 2027.

At one point, I was thinking to myself “how do I position size into humanoid robotics? how can I possibly decide who will be the ultimate winner?” The thing is… I can’t. There will be multiple winners and the initial land grab will lead to skyrocketing valuations long before any narrative changes that involve commodization or margin compression. So I have taken a bit of a shotgun approach with robotics by investing in 3 different humanoid companies and 2 general intelligence companies.

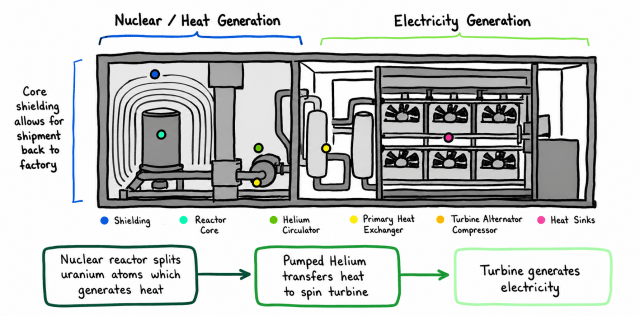

17. Radiant

Date of investment: November 2025

Entry valuation: $1.8 billion on a 0/20 SPV

Bet size: .5 units

IPO status: should assume nuclear is on a long timeline, so 3+ years

Radiant, founded in 2020 by former SpaceX engineers, is trying to shrink nuclear power into portable microreactors that can replace diesel generators in remote bases, industrial sites, physically-secluded communities, and disaster zones. The reactor is called Kaleidos. The vision for Kaleidos is basically compact reactors that can be trucked into the field and provide reliable off-grid power for years without refueling.

I did almost all my nuclear research starting with Deep Fission. At this time, nuclear was raging hot as you had Sam Altman’s OKLO trading north of $20 billion market cap. I first started with the history of nuclear energy in the U.S.–the tl;dr of it is that we basically stopped building plants because nobody wanted to take on the risk and build time. So then SMR’s became a potential solution except there still aren’t any functional power providing SMRs in the USA. There’s a lot of cynicism in the industry because of this supposed obsession with SMR that still hasn’t manifested into actual power. These reactors take much longer to build than what’s usually promised. They say 2028, expect 2030. There’s so much red tape. That said, I like the team here, like that nobody is competing in this micro/mobile niche of SMR, I like the VC firm underwriting their potential, I like the bi-partisan political tailwinds for the sector, and I just like nuclear as a citizen now–I think it will be good for the nation to have it make a comeback. I took a small 0.5 unit bet.

18. Modelyo

Date of investment: November 2025

Entry valuation: $50 million on a 1.5/20 mgmt fee (capped at 5 years)/carry structure

Bet size: .5 units

IPO status: true early investment so none

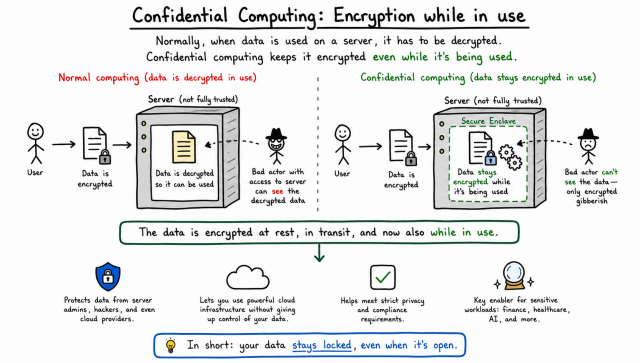

Modelyo is doing something called confidential computing, which is something I hadn’t even heard of yet until literally reading their pitch deck. You can see the explanation of the concept in the image below. Modelyo was born out of necessity during wartime. Its founders—officers from the IDF’s cybersecurity unit—were tasked with protecting sensitive systems from constant hostile intrusion attempts. In the process, they developed novel encryption and confidential computing technologies that ultimately became the foundation of the company.

Gartner identified confidential computing as one of the top future trends for 2026. I’m not going to pretend to be an expert here, I am simply trusting a venture firm–which I’ll refer to as Palm Tree Ventures to underwrite the potential behind this technology. I think there’s beyond 10x upside here.

19. Sygaldry

Date of investment: January 2026

Entry valuation: $400 million on a 1.5/20 mgmt fee (capped at 5 years)/carry structure

Bet size: .5 units

IPO status: true early investment so none

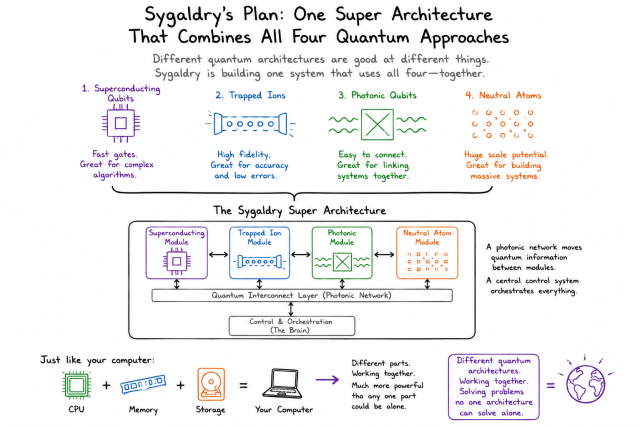

Sygaldry was founded just last year by Chad Rigetti, the founder and former CEO of Rigetti Computing. After stepping down from Rigetti in 2022 and briefly exploring venture investing, he’s now jumping back into the quantum computing race with a fresh approach. There’s basically four types of quantum computing–photonics, trapped ions, superconducting, and neutral atoms. Sygaldry’s novel idea is to combine all four types in a new unique architecture, analogous to how classic computing utilizes different parts like memory, CPU, storage, and motherboard. The first end-product will be quantum servers used for AI training and inference. This is another Palm Tree Ventures investment.

I’ve avoided investing in quantum computing for the most part because it’s too difficult for me to understand. I can’t help but anchor my thoughts to this skeptical post from Scott Locklin on quantum computing–is it possible this entire industry is just a scam? I don’t know. I like the fact that Sygaldry is led by a 2nd-time quantum founder who previously took RGTI public and it’s at a favorable valuation compared to public comparables. There’s still a possibility of a soft landing—even if I’m not fully convinced myself in the tech—as shown by names like RGTI, which went public via SPAC and generated massive returns last year largely on hype.

20. Phoenix Tailings

Date of investment: January 2026

Entry valuation: $360 million on a 1.5/20 mgmt fee (capped at 5 years)/carry structure

Bet size: .5 units

IPO status: true early investment so none

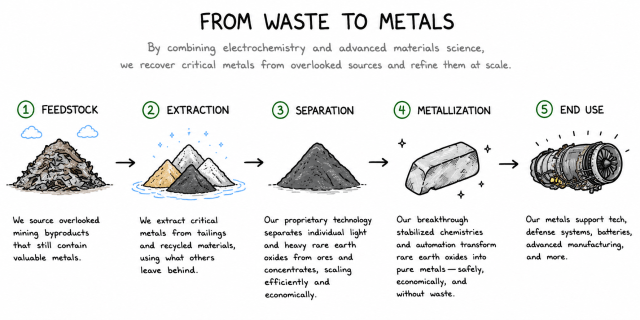

Phoenix Tailings is trying to rebuild America’s rare-earth supply chain from the ground up—without the toxic sludge, massive carbon footprint, and China dependence that define traditional refining today. Instead of conventional mining and chemical-heavy processing, the company extracts critical metals from mining waste (“tailings”) using a cleaner, low-temperature refining process designed to be waste-free, net-zero, and economically competitive. The construction of the modern world—from EVs and AI datacenters to missiles, drones, and robotics—depends on a steady supply of rare earth.

This is my third true venture play with Palm Tree where we’re investing in their Series B. It seems safer than the other two given it’s a resource play rather than a pure technological bet. Their valuation appears cheap compared to another rare earth company called Vulcan Elements, who are rumored to raise their next round at $2 billion.

21. Hark

Date of investment: February 2026

Entry valuation: $5.5 billion on a 2/20 mgmt fee/carry structure

Bet size: 1 unit

IPO status: true early investment so none

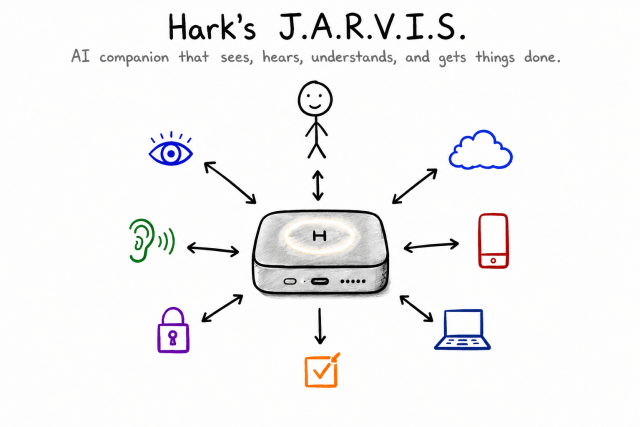

Hark is Brett Adcock’s newest AI company, and the core idea is building a deeply personalized “AI operating system” that lives across custom hardware, software, memory, speech, vision, and agents. Instead of just making another chatbot, Hark wants to create an always-on AI companion that understands your life, remembers context, proactively helps you, and eventually interacts with both the digital and physical world. Brett compares to their future product to J.A.R.V.I.S. from Marvel, the AI interface that Ironman uses for everything. They hired one of Jony Ives’ proteges at Apple to design it.

I think there’s going to be an iPhone moment for AI at some point—the breakthrough consumer product that changes everything—and this is my bet on who builds it.

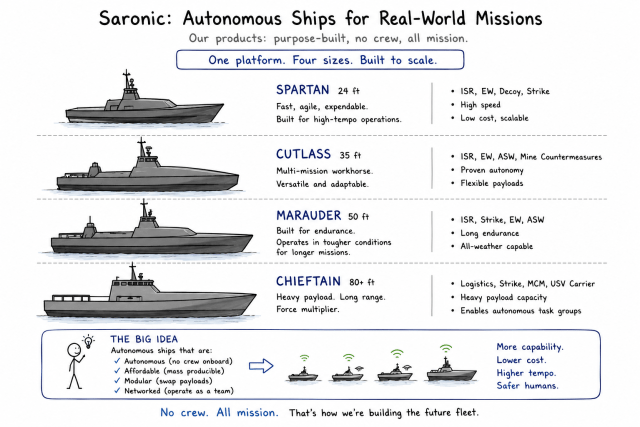

22. Saronic

Date of investment: March 2026

Entry valuation: $9.25 billion on a 5/0 SPV

Bet size: 1.5 units

IPO status: 2-3 years

Founded in 2022 by former Navy SEAL Dino Mavrookas, Saronic is building autonomous surface vessels — essentially AI-powered robotic boats for the military. The thesis is that future naval warfare shifts from a handful of ultra-expensive ships toward large fleets of cheap, autonomous, “hive-controlled” ships that can scout, surveil, and fight with far lower human risk and dramatically lower cost. They already operate a port in Franklin, Louisiana, and are now seeking to build a next-generation facility known as “Port Alpha.”

I think investing in Saronic now is like investing in Anduril 2 years ago. They’re a new defense prime that will directly address our shortcomings in naval shipbuilding. We are way behind China’s naval-industrial capabilities and we’re going to need naval power to defend Taiwan, if that day ever arises.

23. Advanced Machine Intelligence (AMI Labs)

Date of investment: April 2026

Entry valuation: 15-30% discount of series A via SAFE notes

Bet size: 1 unit

IPO status: true early investment so none

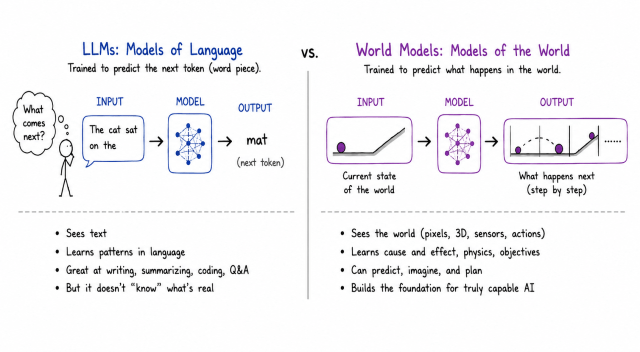

AMI Labs, backed by Yann LeCun, is focused on building next-generation AI systems that move beyond today’s prediction-heavy large language models toward machines that can actually understand, reason about, and interact with the physical world. The core thesis is that current AI is fundamentally limited because it mostly learns from text, while real intelligence comes from building internal world models — understanding cause and effect, physics, memory, planning, and common sense the way humans and animals do. AMI is essentially pursuing a longer-term vision of “human-level machine intelligence,” emphasizing autonomous learning and real-world understanding over simply scaling bigger chatbots. Their $1 billion dollar seed round was the largest ever seed round for a European company, valuing them at $3.5 billion.

This investment is my hedge that LLM’s eventually show an upper bound limit before the breakthrough the AGI and frontier labs have to then pivot to world models. LeCun is one of the godfathers of the AI movement and he has genuine and tremendous conviction that world models are the way to go.

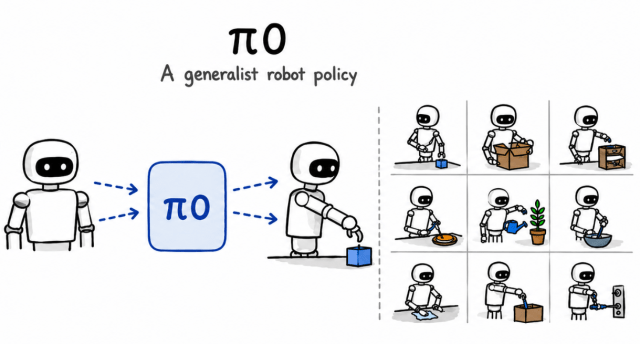

24. Physical Intelligence

Date of investment: May 2026

Entry valuation: $11 billion valuation at 1/10 mgmt fee/carry structure

Bet size: 3 units

IPO status: a few years

Physical Intelligence (Pi) is a startup developing large AI world models to power robots. Pi is building real world models that make robots “intelligent” the same way humans are intelligent. This remains an unsolved, open-ended research problem. Pi has released a general-purpose robot foundation model called π0 which has demonstrated capabilities to perform numerous dexterous tasks. They’re already in active partnerships with companies like Disney, Nike, Samsung, Intel and Toyota. The company’s philosophy is, “If you can solve physical intelligence, you can build one of the largest companies ever.”

They are a direct competitor to Skild, basically trying to build the future generalized brain of all robots. Skild does their training via simulation while Pi trains on real-world human data. I don’t want to pick between the two, I want both. I like that two of the top performing firms of the last decade (Founders Fund and Thrive) are backing Pi. That means I have to be in it too.

Okay, so that’s basically it. I did have a Stripe investment from a $91 billion valuation once, but that was involuntarily sold-off by an SPV manager in a double layer with Aurelius Investments. I received an 18% net return on 7 months of holding it. Could be worse I guess.

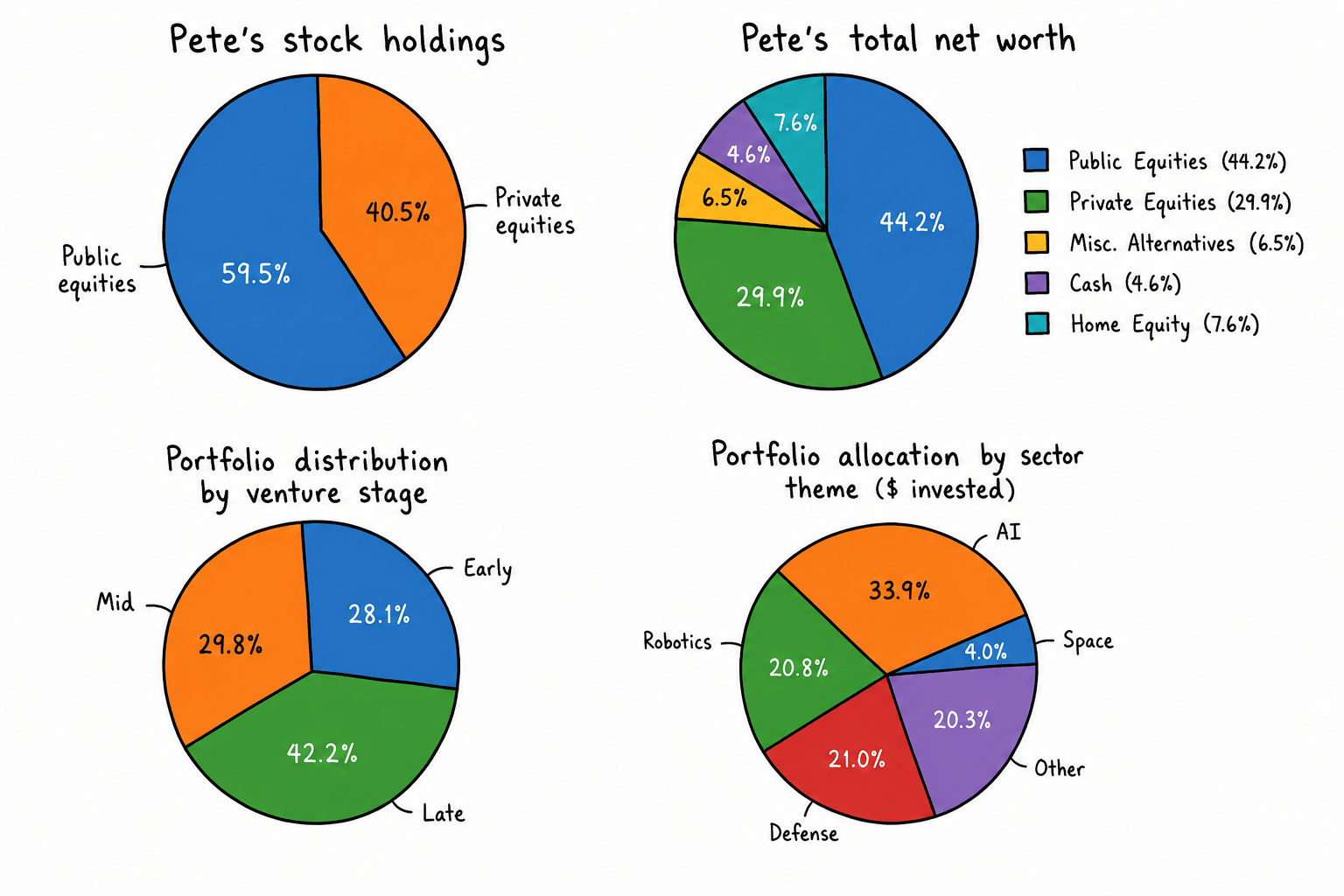

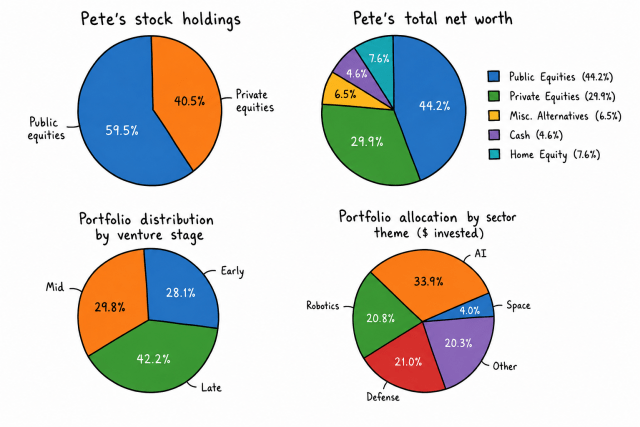

Now for some pie charts.

PETE’S INVESTMENTS IN PERSPECITVE

Note: all private investments are based on initial capital contribution–that means no markups and no fees yet. I only use the exact amount of money I wired in. Venture stage and sector themes were decided by ChatGPT to be semi-objective.

Just to give you an idea of how much my allocations have changed:

Before 2023, 40–50% of my net worth sat in cash and short-term equivalents. I was just too conservative. Getting 4–5% risk-free felt “good enough,” and I kept waiting for a bigger market pullback before increasing my equities allocation. We were just coming out of the frothy ZIRP era where too many bad ideas went parabolic.

Instead, the bull market came back earlier than I anticipated. My public portfolio—mostly index funds and Mag 7 names—became a larger and larger piece of the pie while the cash I didn’t deploy slowly started feeling like dead weight.

Then I decided to introduce venture and pre-IPO into the portfolio in 2024. It started slowly and then accelerated as I became more of a believer in future innovation themes like AI, space, defense, and robotics.

I started pulling money out of trading accounts to fund private deals. Last year I completely sold off all my crypto to fund venture. This year I sold my weaker-performing public equities to fund more venture.

At this point, close to 30% of my net worth is in private companies—far above the 5–10% most wealth advisors would ever recommend because of the risk and illiquidity. Honestly, if I didn’t have a family to support or large public-equity tax obligations hanging over me, that percentage would be even higher.

I don’t view it as reckless. I view it as the obvious opportunity right in front of my eyes.

And that allocation could climb materially higher soon. If just two positions—SpaceX and Deep Fission—were marked to their projected IPO pricing after June 12th, my private portfolio alone would increase by roughly 52%. That would push venture from ~30% of my net worth to roughly 39%. It’s still early and I haven’t executed an exit yet but I definitely feel validated so far.

You never thought you’d see Pete talking about allocations–like some old bogleheaded wealth manager, did you? Or talking about venture like some Silly-Con Valley douchebag. You thought it would always be about spamming buttons, spending an obscene amount on locates, and being on raging tilt as I lost $108,237.92 in 6 minutes trying to short some bullshit low float out of China.

Nope. Those days are done. This is the new Pete–more money, less stress.

Related

Source link